Crude Concerns

Week Ending: March 13, 2026

Crude Concerns

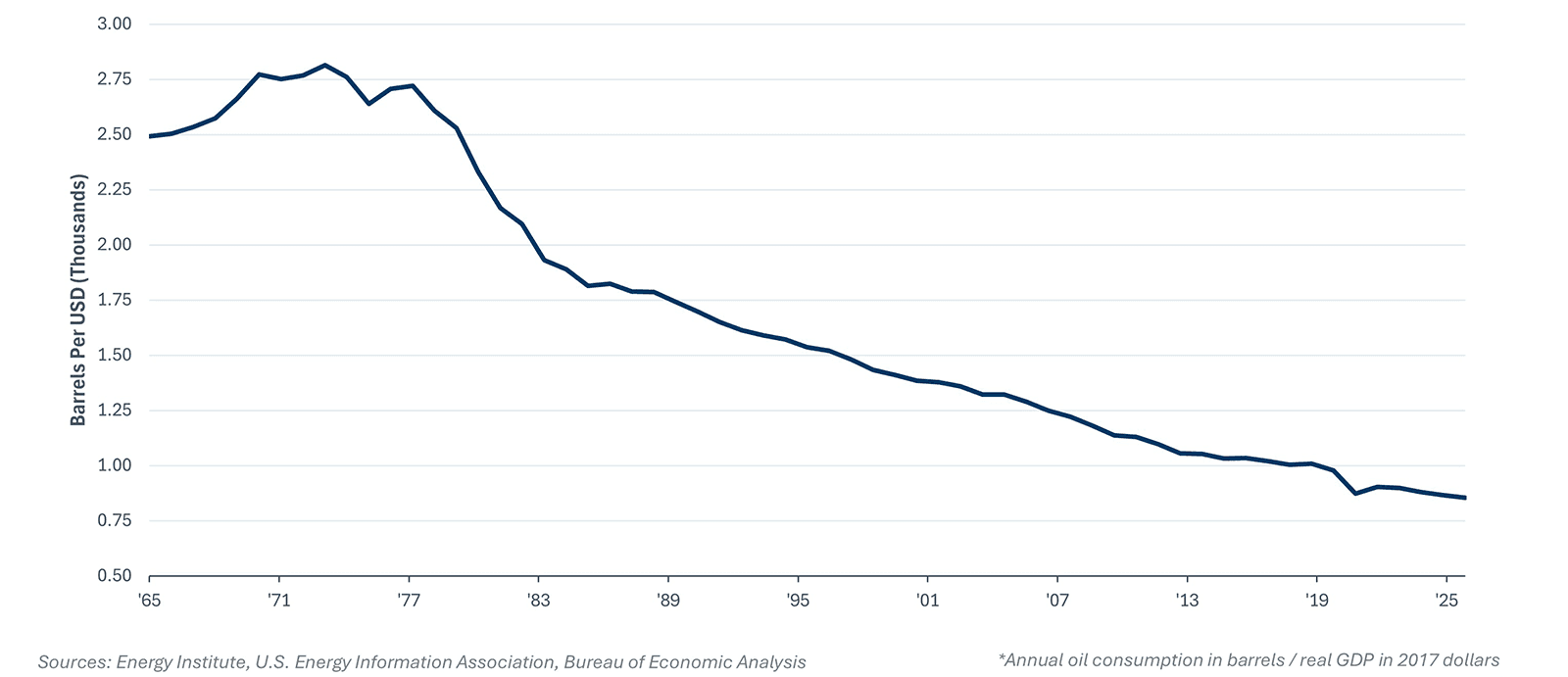

U.S. Oil Consumption Per Unit Of Real Output*

The conflict in the Middle East reignited fears of a recession, a pickup in inflation, or both, driven by an “oil price shock.” However, we would caution against being overly pessimistic on growth or too worried about an inflation pickup. First, the pass-through of higher oil prices to core inflation has been limited in recent decades. Second, while higher energy prices will eat into consumer income, it will take sustained elevated energy prices to further erode income growth (e.g., more than a quarter). Third, the U.S. economy’s oil intensity has fallen by 66% since 1965, driven by diversification into other energy sources and a shift from manufacturing to services. Fourth, the U.S. recently transformed from a net petroleum importer to a net petroleum exporter, further insulating the country against oil price shocks. Perhaps the transmission from oil price shocks to growth and inflation is weaker today than ever, at least for the U.S.

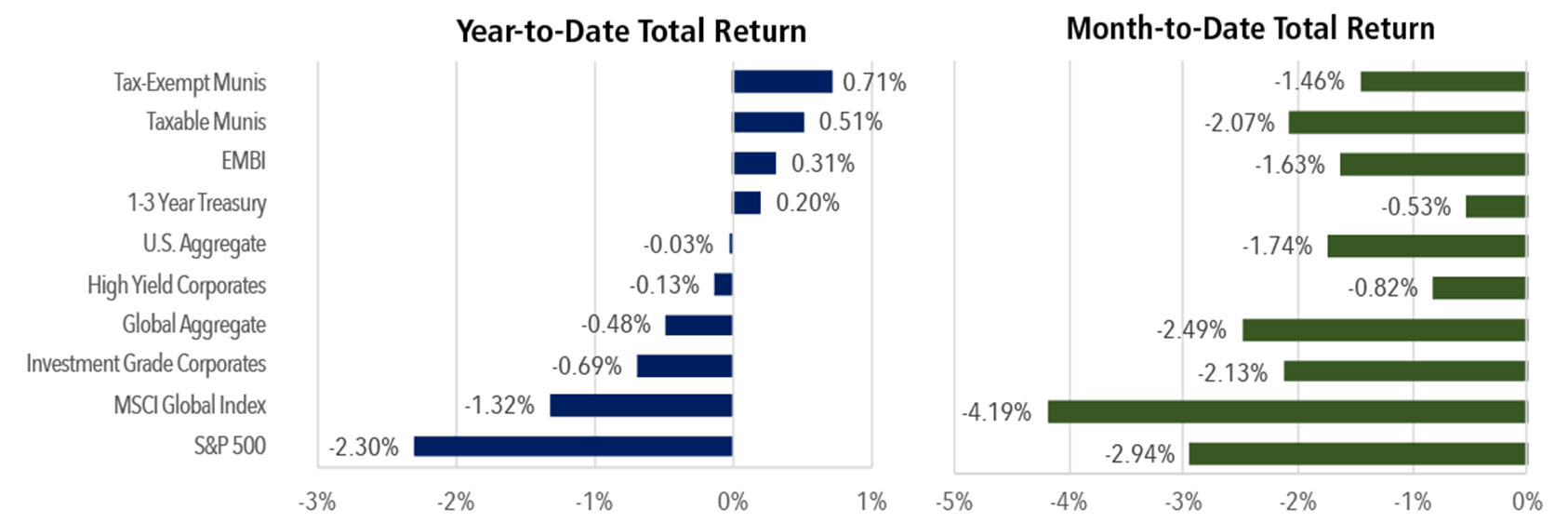

Total Returns by Asset Class

Highlights of the Week:

High Yield: High yield bond investors navigating the impact of the U.S. war with Iran need to consider the long-term effects of higher oil prices on energy issuer fundamentals. While the short-term consequence might be improved cash flows, the long-term impact could be demand destruction and, ultimately, lower revenues. Active management is crucial in the current environment.

Corporates: This week’s $113 billion new issue supply marked the second busiest issuance week ever in IG, including two of the top ten largest deals ever, with Amazon and Salesforce pricing at $37 billion and $25 billion, respectively. The heavy supply and elevated market volatility pushed spreads wider by 7 basis points this week to an option-adjusted spread of 90 basis points as of Thursday’s close.

Municipals: Despite recent volatility, municipal bond inflows have stayed positive for 16 consecutive weeks. For the latest week, LSEG Lipper reported $612 million in inflows, pushing year-to-date inflows to $22.8 billion—the third-fastest on record.

Equities: The U.S. equity market experienced negative returns for a third straight week as rising geopolitical tensions continued to weigh on investor confidence. Most sectors declined, with industrials, financials, and consumer discretionary facing the steepest losses, while utilities, energy, and consumer staples were the top performers.

Securitized Products: The asset-backed security (ABS) market remained resilient despite macro volatility, with spreads widening by only a few basis points due to increased secondary supply. A variety of new issue supply was easily absorbed this week, with typical subscription levels in equipment, auto, and data center ABS, while a fiber ABS deal was multiple times oversubscribed. Although fiber ABS tightened in the secondary market due to strong demand, some weaknesses appeared in non-investment grade subprime ABS, possibly influenced by higher gas prices.