Post-Mortem: What We Learned In H1 2026 – And What That Implies For Our Outlook

Good forecasting requires honest – and often harsh – self-appraisals of past performance. We subject our 2026 calls to critique, update our outlook for the next 12 months to incorporate what we’ve learned, and speculate on the remaining pitfalls to watch for in the second half of the year and beyond.

“To err is human. To blame someone else is politics.” - Hubert Humphrey

In our economic outlook published at the end of 2025, we detailed our expectations for 2026 of continued economic growth led by tech-related investment, moderating inflation, a slight rise in the unemployment rate, and multiple rate cuts from the Fed. As a consequence, we expected lower interest rates across the yield curve, with credit and equities outperforming government bonds.

So far in 2026, though, we’ve experienced a sharp rise in interest rates, driven by solid economic growth, sticky core inflation, a flat unemployment rate, and a Fed that is seemingly on hold for the foreseeable future, with the bond market pricing in nearly two hikes over the next 12 months.

So what did our call get wrong?

While we’d love to adopt the standard TV pundit ploy and blame it all on “how-could-we-have-known” geopolitical events, it turns out the Iran War was not a critical factor in our forecast misses.

In fact, we downplayed the invasion as a game-changer for asset prices (see our Iran note), and we stand by our view that geopolitical events tend to have short-lived economic and financial market impacts.

We also stand by our view that higher oil prices represent a price-level shift, not an enduring inflation story.

So if not geopolitics, where did we go wrong?

We learned a few new things about the labor market, inflation, growth, and rates over the first half of 2026.

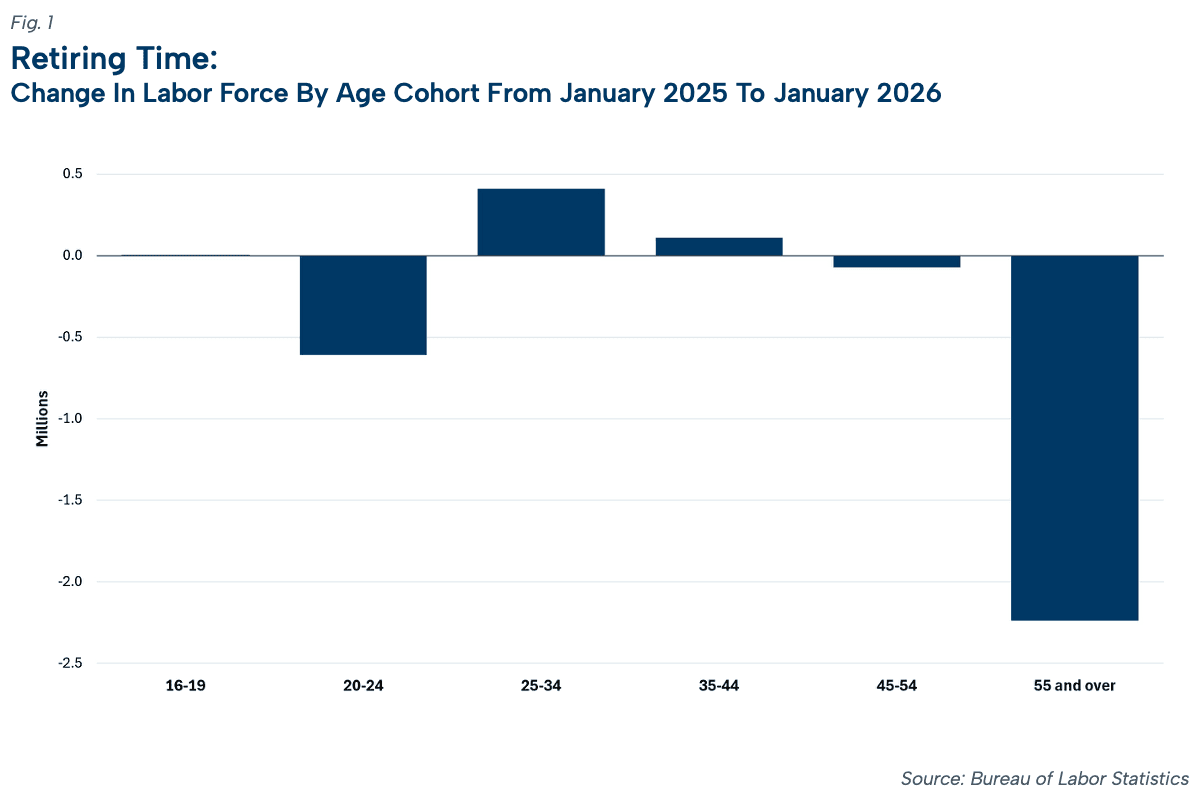

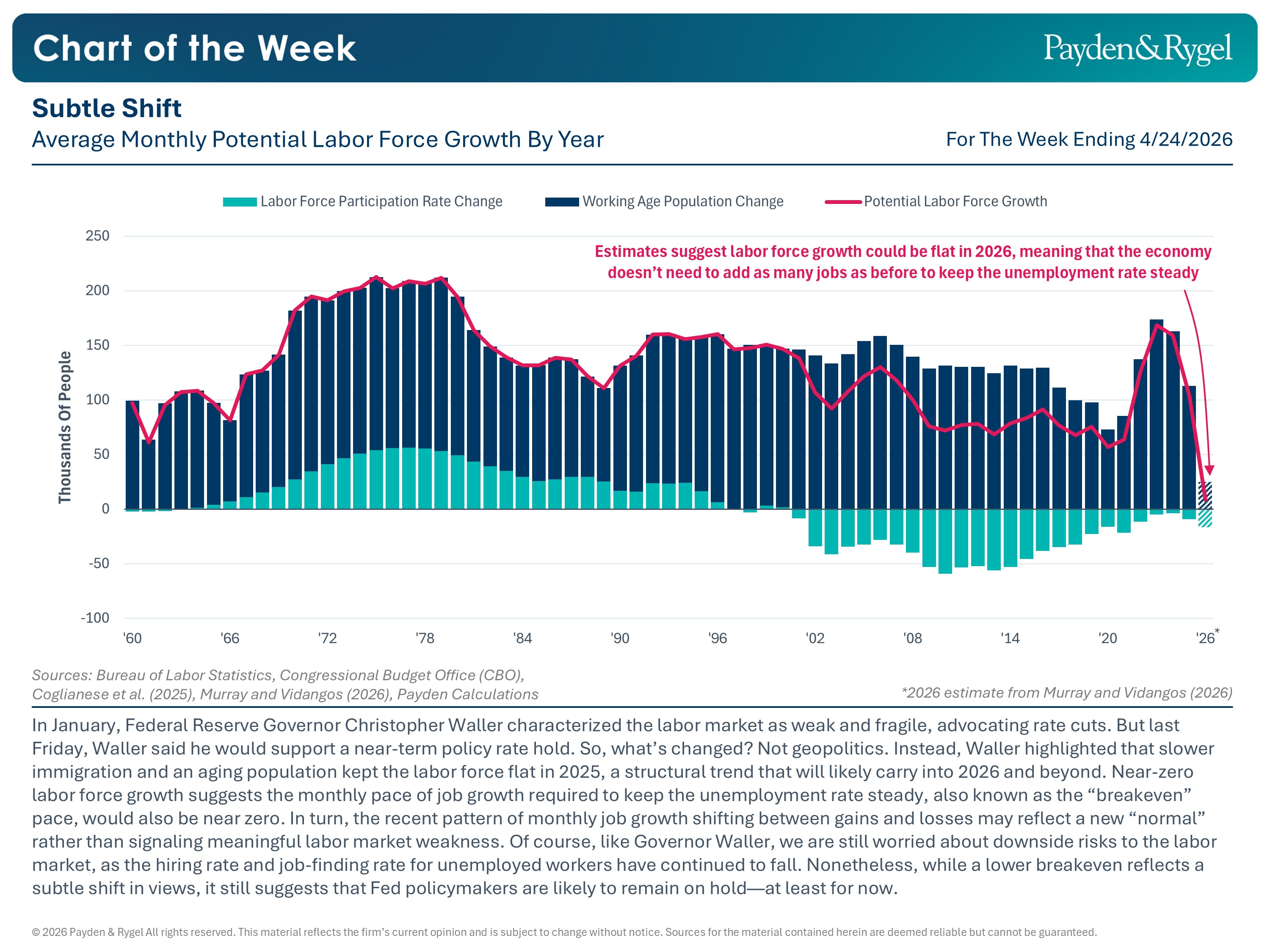

First, on the labor market, after 18 months of very weak job growth, the unemployment rate has barely budged.

With the benefit of data revisions, we know why: more people have left the labor force (mostly retiring) than have entered it (due to slower population growth and migration restrictions; see Figure 1). So, fewer jobs are needed each month to keep the unemployment rate steady. As a result, weak job growth in 2025 presented less of a risk than we had anticipated.

Figure 1 - Retiring Time:

Change In Labor Force By Age Cohort From January 2025 To January 2026

Source: Bureau of Labor Statistics

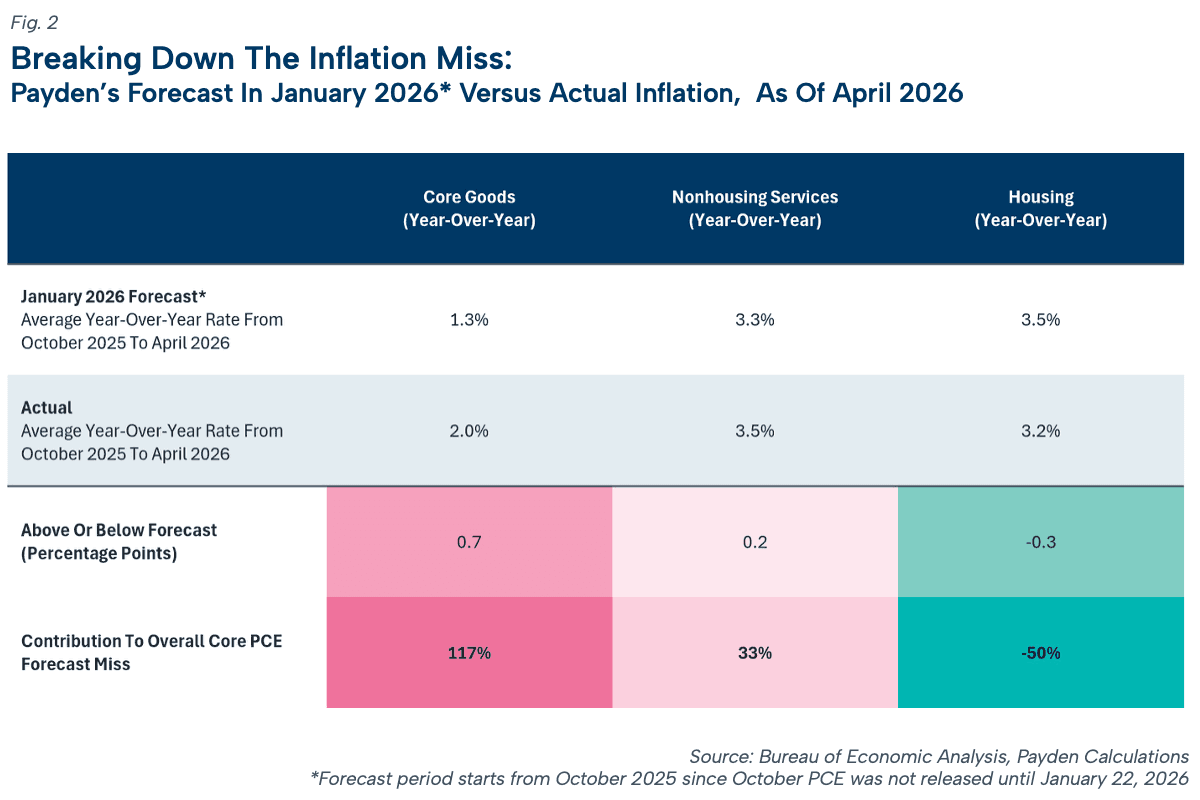

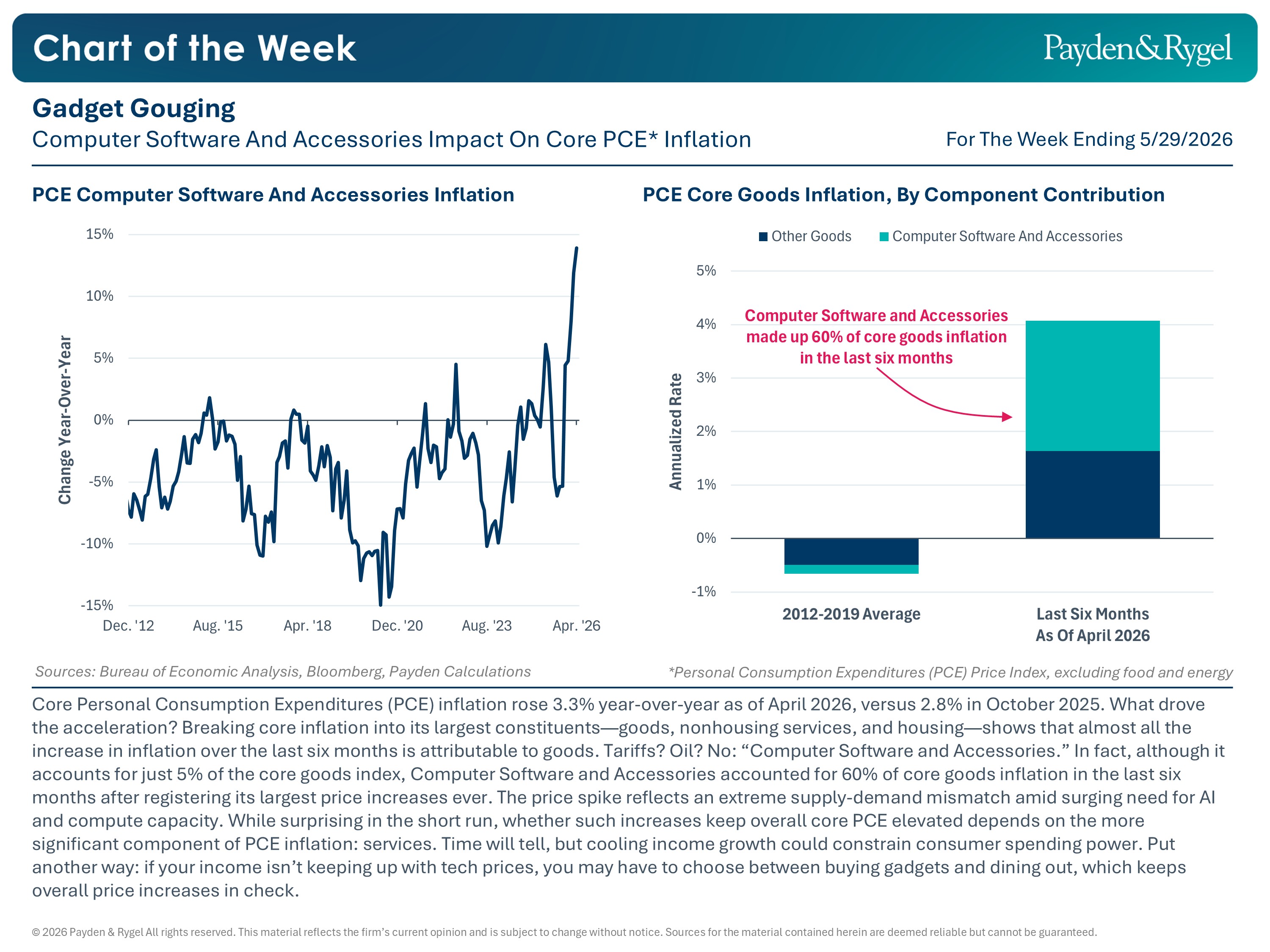

Second, core inflation remains sticky, with year-over-year core PCE inflation at 3.3% as of April, up from 2.8% six months ago. Dissecting changes in the three major constituents of core inflation shows that, since October 2025, the culprit has been core goods prices, which accounted for over 70% of the rise (see Figure 2).

Figure 2 – Breaking Down The Inflation Miss:

Payden’s Forecast In January 2026* Versus Actual Inflation, As Of April 2026

Sources: Bureau of Economic Analysis, Payden Calculations

*Forecast period starts from October 2025 since October PCE was not released until January 22, 2026

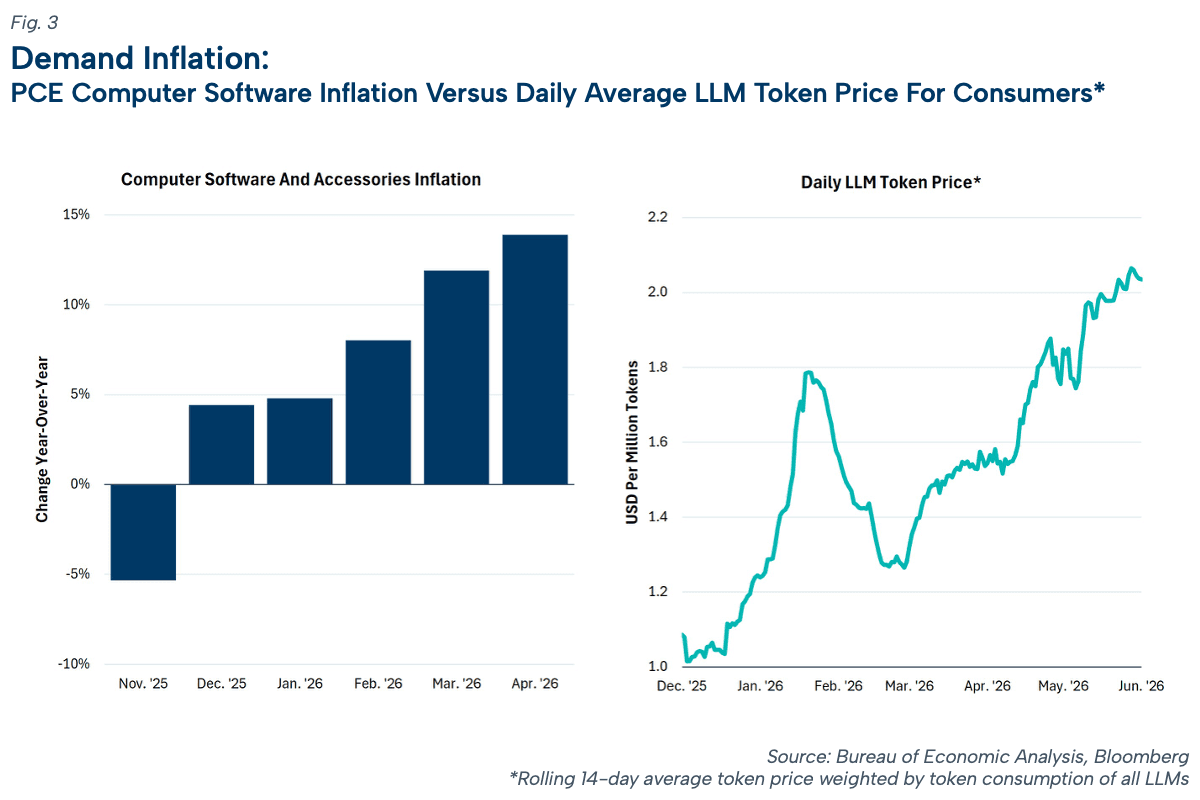

Tariffs? Oil? Neither.

Instead, it turns out that information-processing equipment – specifically, computer software and accessories – accounts for the majority of the rise in goods prices amid the AI boom. After all, it makes sense that surging demand for compute capacity driven by increased AI use will push up AI prices for consumers while supply is still catching up (see Figure 3).

Figure 3 - Demand Inflation:

PCE Computer Software Inflation Versus Daily Average LLM Token Price For Consumers*

Sources: Bureau of Economic Analysis, Bloomberg

*Rolling 14-day average token price weighted by token consumption of all LLMs

Ironically, we’ve belabored the fact that hyperscalers' current data center buildout is nowhere near sufficient to meet AI demand (here, here, here, here, and here). Still, we’ve failed to account for how an extreme demand-supply mismatch, also related to the tech boom, would, in the short run, drive prices on AI-related software and accessories.

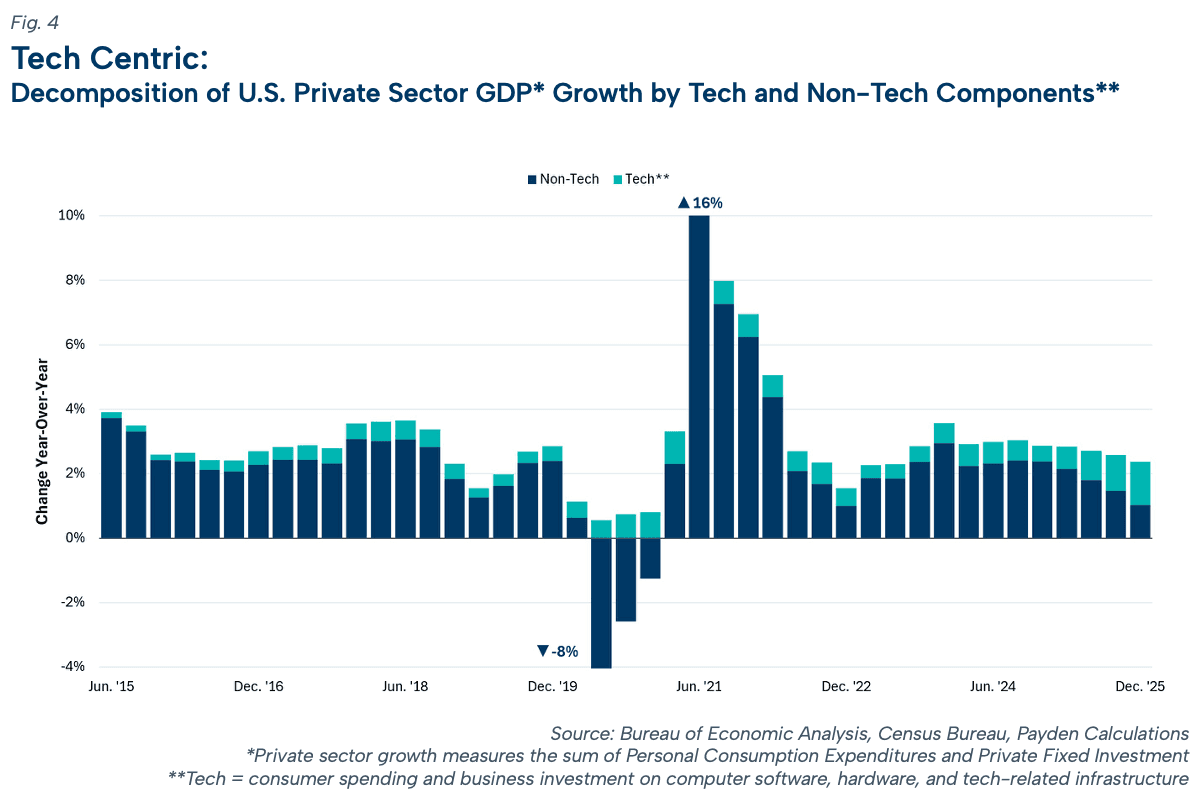

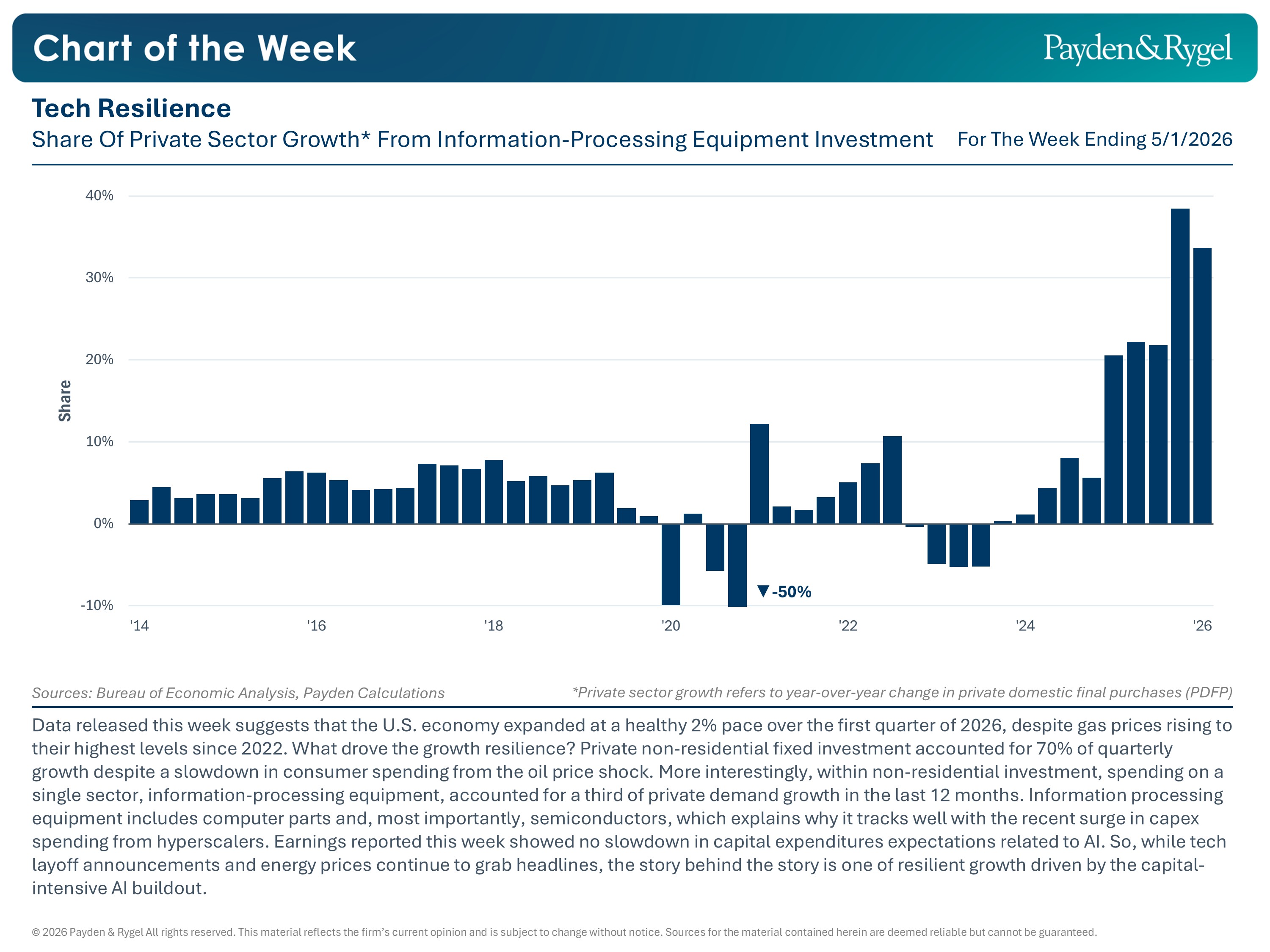

Third, economic growth has held up even better than expected despite consumer spending slowing in the first quarter of 2026. Investment activity, namely, private-sector investment in AI-related hardware and software, drove nearly 60% of net private-sector growth in the last four quarters (see Figure 4).

Fourth, regarding the Fed, we maintained that it would resume cutting in 2026, not because of Warsh at the helm, but contingent on inflation moderating and/or unemployment ticking up. Neither has occurred so far.

Even Fed Board Governor Chris Waller, perhaps the most dovish member of the Federal Open Market Committee (FOMC) who’s been advocating for rate cuts since July 2024, admitted recently in a speech that “inflation is not headed in the right direction” and that his “current policy position is to hold rates steady for the near term” unless there’s “improvement on inflation or a significant deterioration in the labor market.”

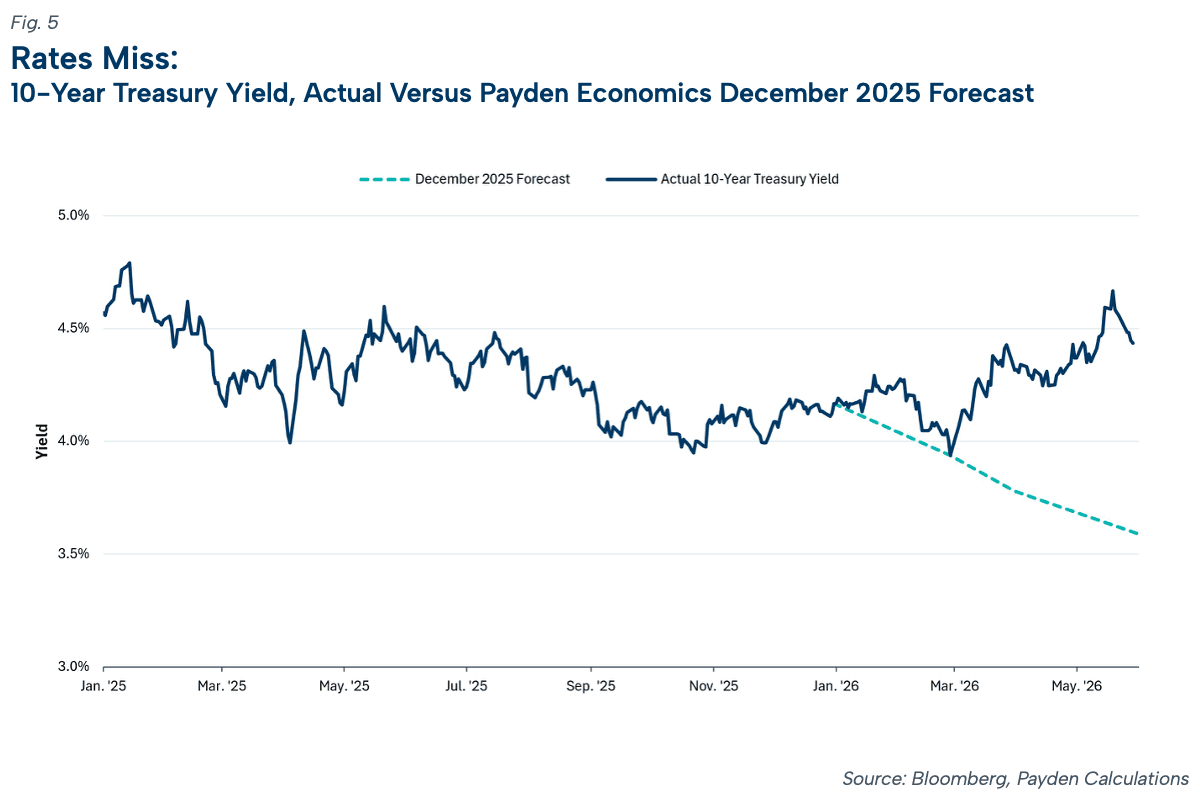

And the above errors compounded: being wrong on the Fed call and inflation path also means we were too bullish on rates. At the beginning of the year, we expected the 10-year Treasury yield to dip toward 3.5% by the end of 2026. In contrast, yields have risen over 30 basis points year-to-date, with inflation the largest driver of our forecast miss (see Figure 5).

On a positive note, we reduced our probability of a recession over the course of H1, even amid higher energy prices, by tracking labor market and tech spending signals, which kept us upbeat on credit and equity exposure despite the war. Where we fell short was in tracing the tech boom’s impact on consumer prices.

So, how has our outlook evolved based on the above postmortem?

First, hiring activity bottomed out in Q2 2025 following the tariff shock and picked up again in recent months, while layoffs remain low. Meanwhile, labor force growth will likely remain sluggish in 2026 as a structurally aging population persists over the next decade. In turn, better job growth will keep downward pressure on the unemployment rate, which we expect to end the year at 4.1%.

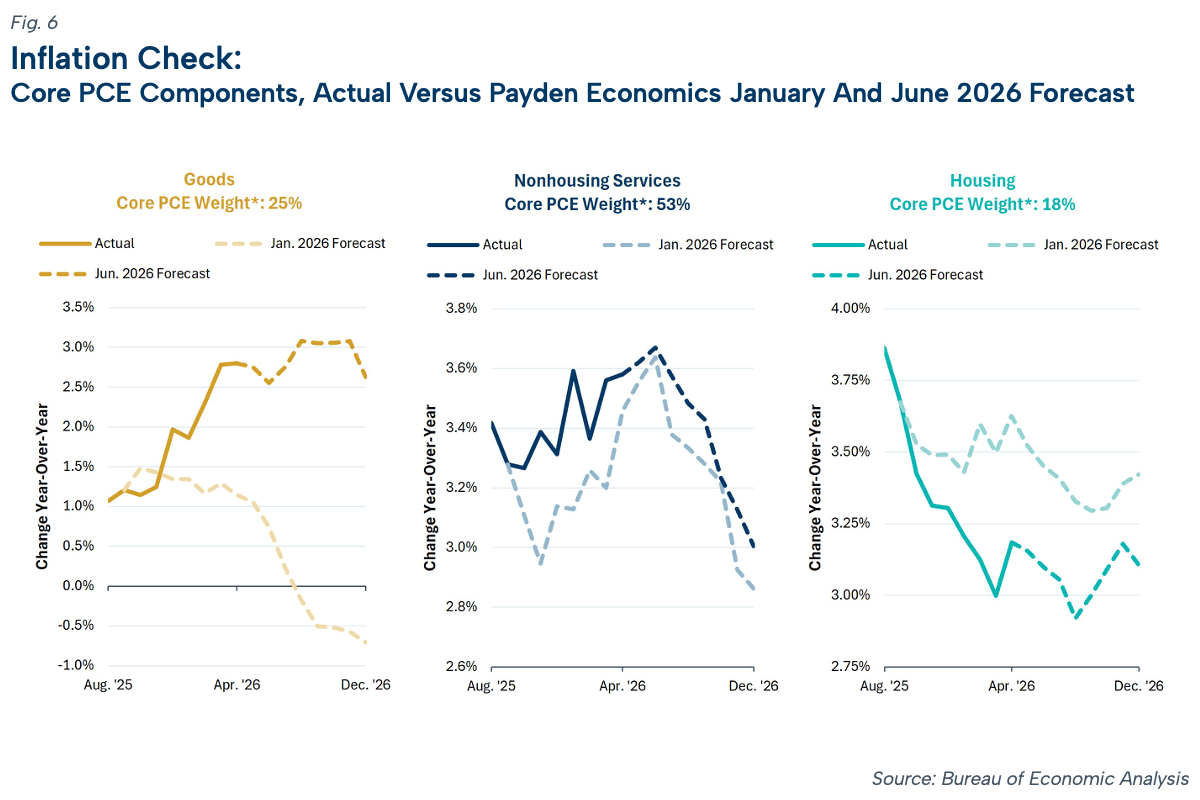

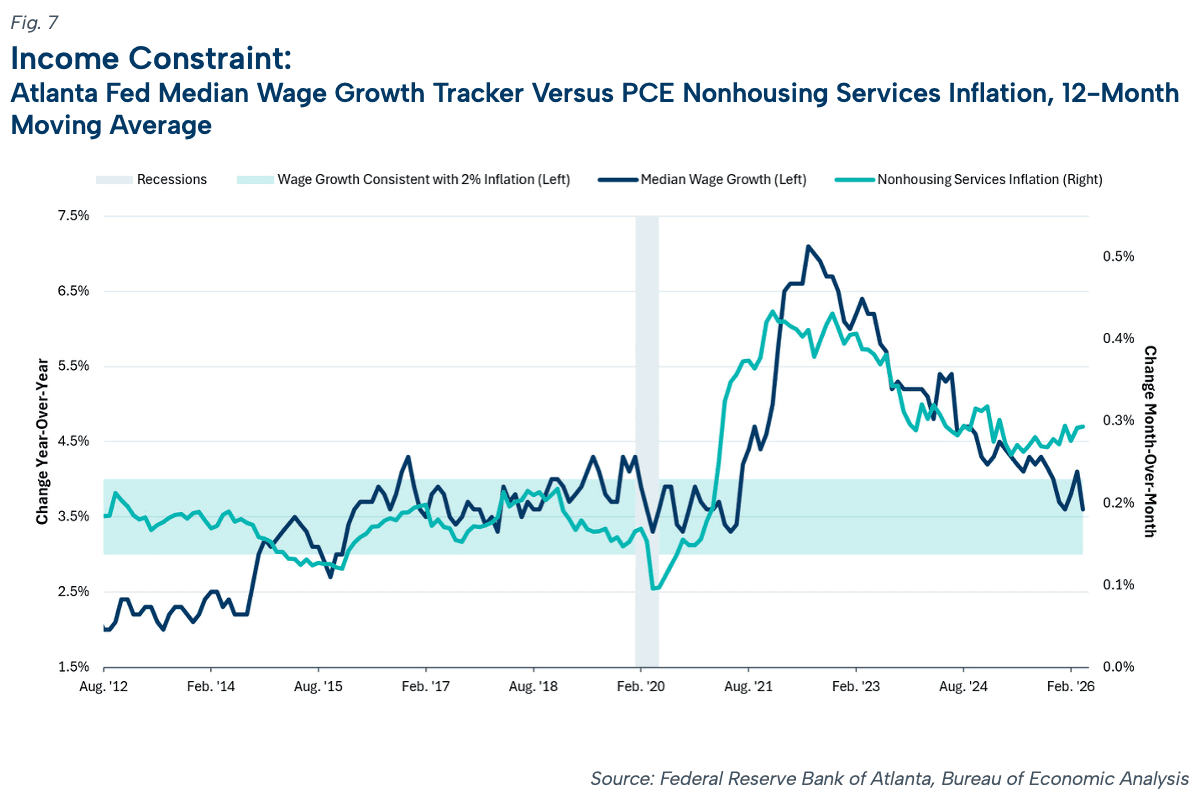

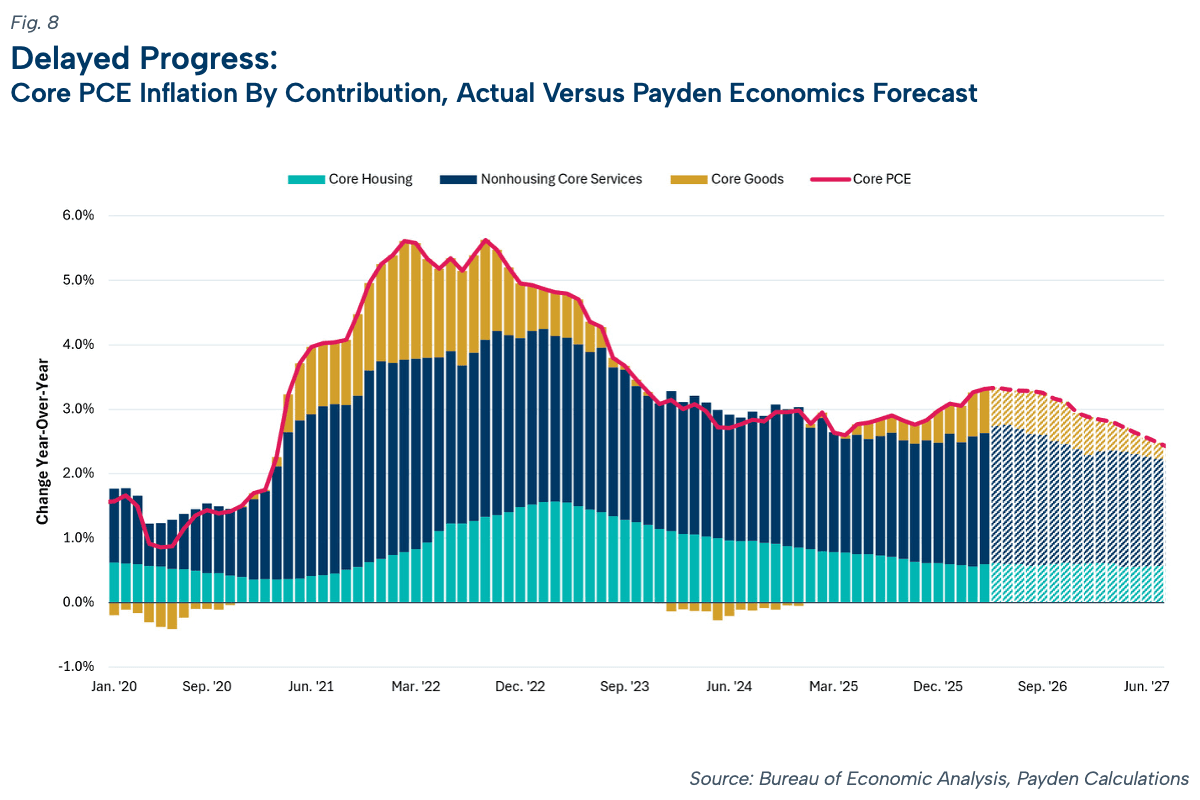

Second, we expect core inflation to remain sticky around 3% through December 2026, driven largely by core goods prices, particularly for computer software and accessories (see Figure 6). We still expect disinflation despite stronger job growth; we are far from an overheating labor market, which should keep wage growth tame and drive continued disinflation in nonhousing services and in housing inflation (see Figure 7). But progress on year-over-year core PCE inflation will have to wait until the second half of 2027 (see Figure 8).

Third, we expect the U.S. economy to grow at around 2% through the second half of the year, powered by tech investments that should continue into 2027, based on hyperscalers' capital expenditure expectations and demand for AI hardware and services.

Fourth, elevated inflation near 3% and a remarkably stable unemployment rate will keep policymakers on hold at least through the next 12 months. The next rate move is still more likely a cut than a hike, but the timing will depend heavily on progress on inflation, which we don’t expect until the latter half of 2027.

As we look ahead to the summer and the second half of 2026, we also wonder: what risks threaten the revised outlook?

We’d highlight two alternative paths to the updated outlook above.

First, what would prompt the Fed to hike?

We are watching two things: wage growth and inflation expectations.

A reacceleration in wage growth will allow businesses to continue passing higher prices for goods and services on to consumers, driving inflation. And wage growth could accelerate if the labor market heats up, whether it’s job growth continuing to pick up or tech investment fueling pull-forward hiring demand. Recent job openings data showed that small firms in the West, particularly in professional and business services, have experienced a surge in hiring demand (AI-related?). We will be watching for a sustained dip in the unemployment rate below 4.1% and an acceleration in wage growth to move to the “reacceleration” camp.

There is a caveat, though: wage growth accompanied by productivity growth may still not pose an inflation threat.

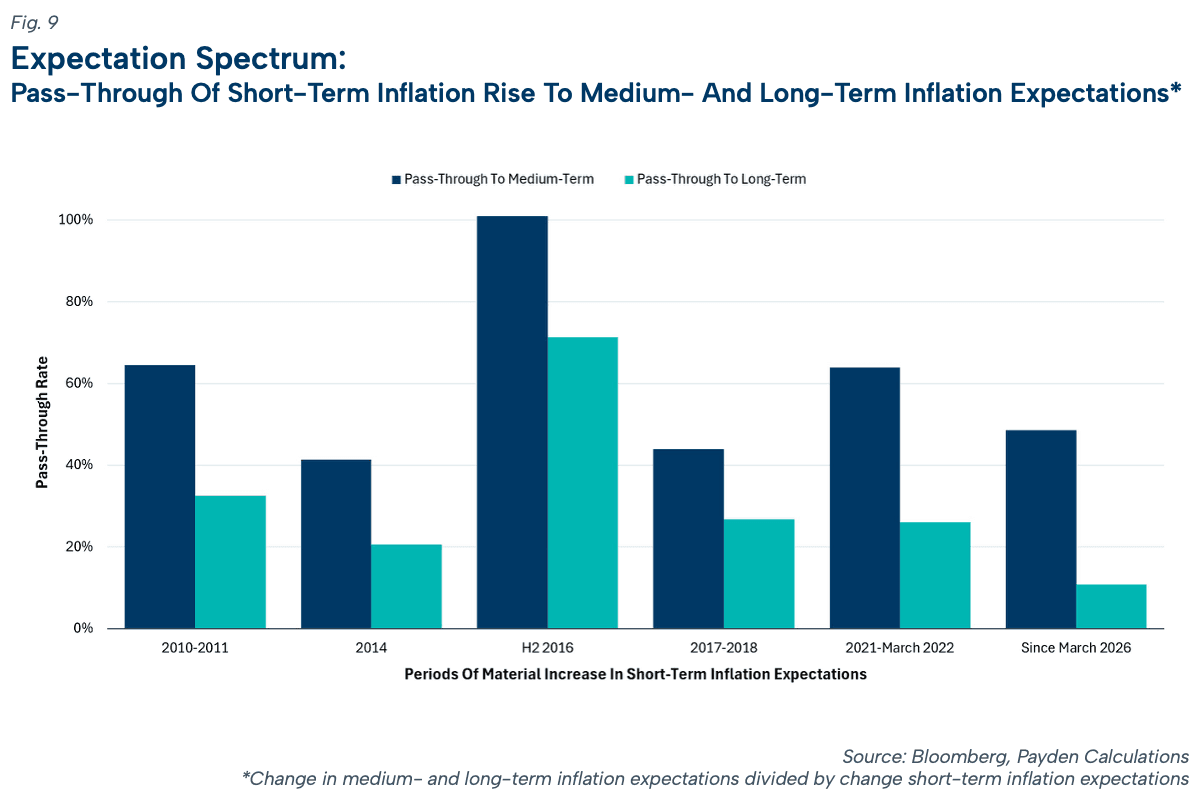

The second catalyst for hikes would be a modest rise in market-derived inflation expectations, as reflected in the 2-year (medium term) and 5-year (long term) forward inflation swap rates. Policymakers who are increasingly disappointed with having missed their inflation target for now 5+ years may cite de-anchoring inflation breakevens as a reason to act now (by hiking) rather than merely sit on their hands and hope our disinflation scenario plays out.

So far, the increase in market inflation expectations has been more muted compared to past episodes (see Figure 9). A further rise in inflation expectations, like the 2021 episode, would put multiple rate hikes on policymakers' radar.

Are there other potential drivers of higher rates? Well, AI investment could also boost productivity growth and, all else equal, imply a higher real neutral rate. However, so far, AI-driven productivity remains an early promise rather than a guaranteed outcome.

Second, what could prompt rate cuts?

Since U.S. domestic growth is being driven primarily by tech, any pullback in hyperscaler investments due to financing constraints could take growth below trend.

It’s also possible that inflation moderates faster in the next 12 months if the tech-driven goods inflation burst is more short-lived or offset by faster disinflation in services.

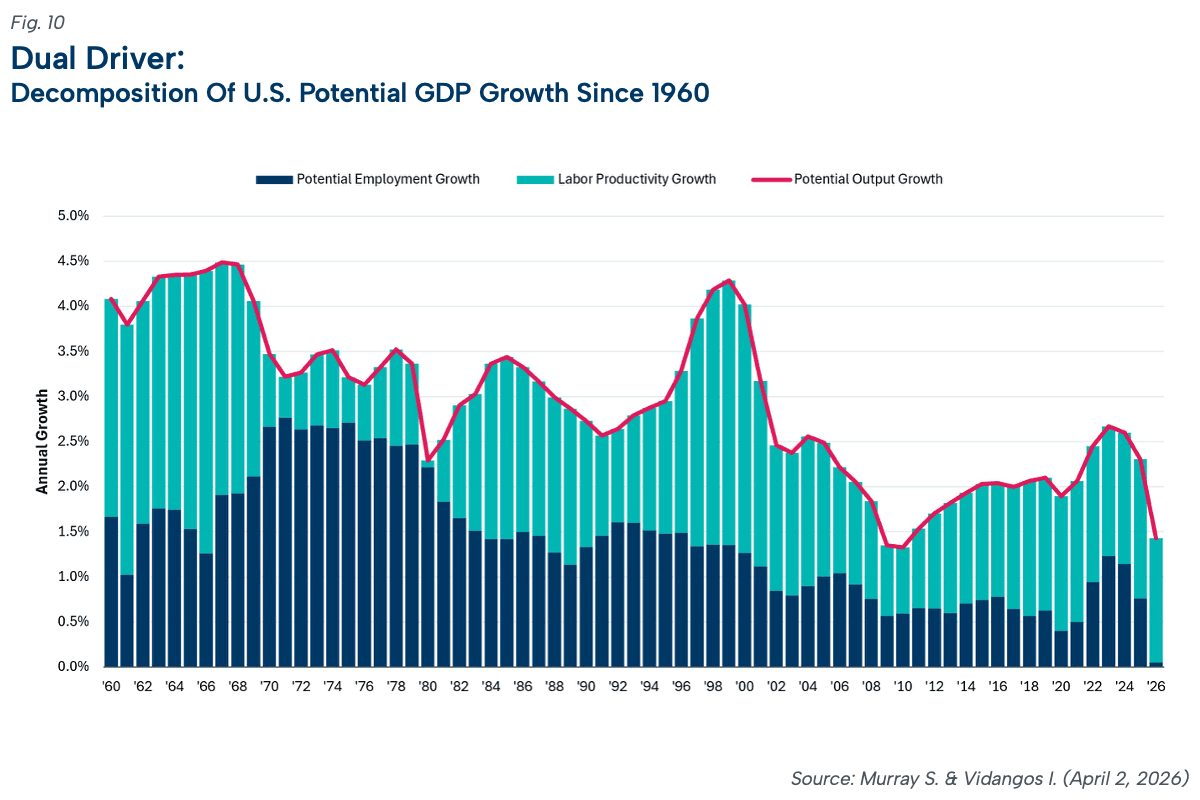

And stagnant labor force growth implies that potential growth will depend almost entirely on productivity growth (less help from more people working; see Figure 10). In turn, lower potential growth could mean lower interest rates.

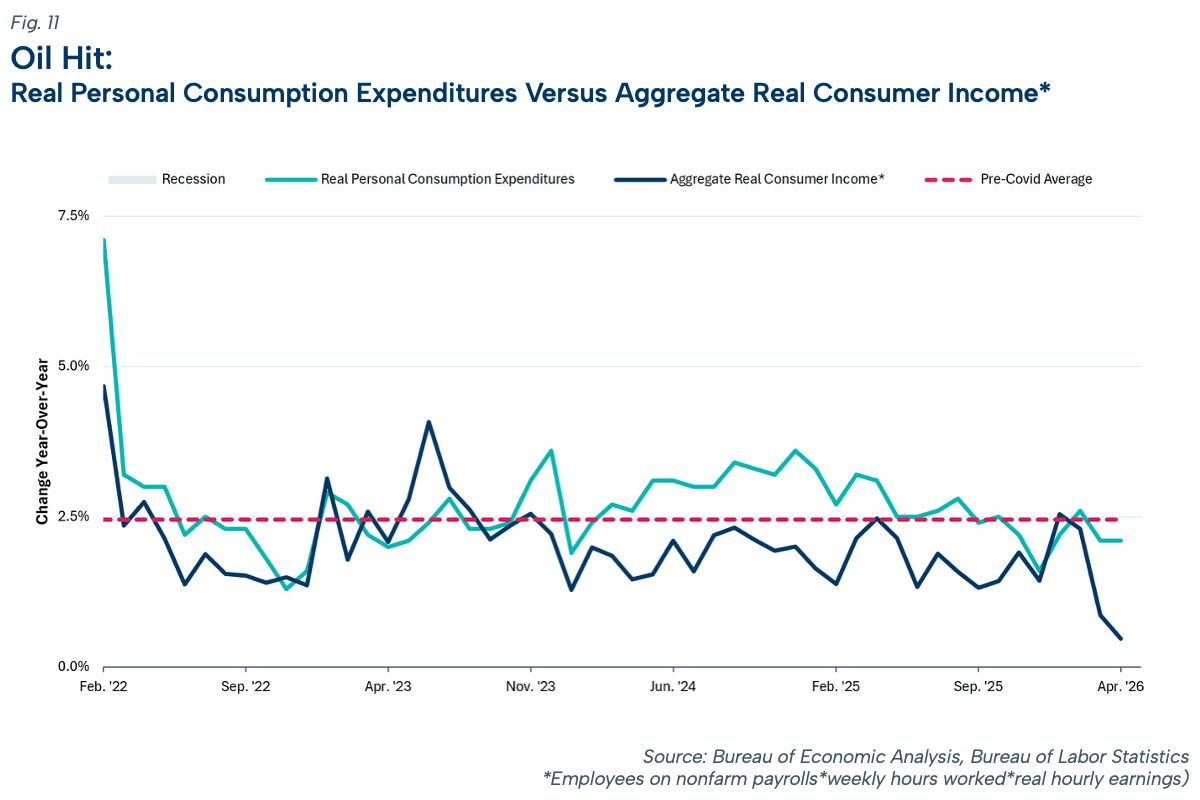

Finally, the sharp slowdown in aggregate real (inflation-adjusted) consumer income growth over the last two months could slow spending (see Figure 11).

All told, we think the Fed is on hold for the foreseeable future, and the risk tilt is toward stronger growth and stickier inflation over the next 12 months. Rate hikes remain a possibility but not a foregone conclusion.

As the path ahead remains highly uncertain, be wary of strong opinions that remain unchanged in the face of new data.

Enjoy your summer,

The Payden Economics Team

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}