There’s a running joke in the U.S. that may offend our European readers (if you’re among the easily offended, avert your gaze now): America innovates, Europe regulates (see Did You Know? Box: Strangled By Red Tape).

Did You Know?

Strangled By Red Tape

Corporate governance is a slogan for European companies, but it comes at the significant cost of overregulation. As a simple comparison, over the last five years, about 3,500 pieces of legislation were enacted in the U.S., while around 13,000 acts were passed in the EU.11 There are a few reasons why overregulation is not good for economic growth. First, regulation naturally leads to more reporting and compliance costs, redirecting valuable company resources from actual productive activities, particularly for start-ups. Second, strict labor laws prevent the efficient redistribution of labor across firms, as laying off or firing unproductive workers might create more cost for a company than keeping them on. As the headline goes, Europe might be regulating itself into last place.12

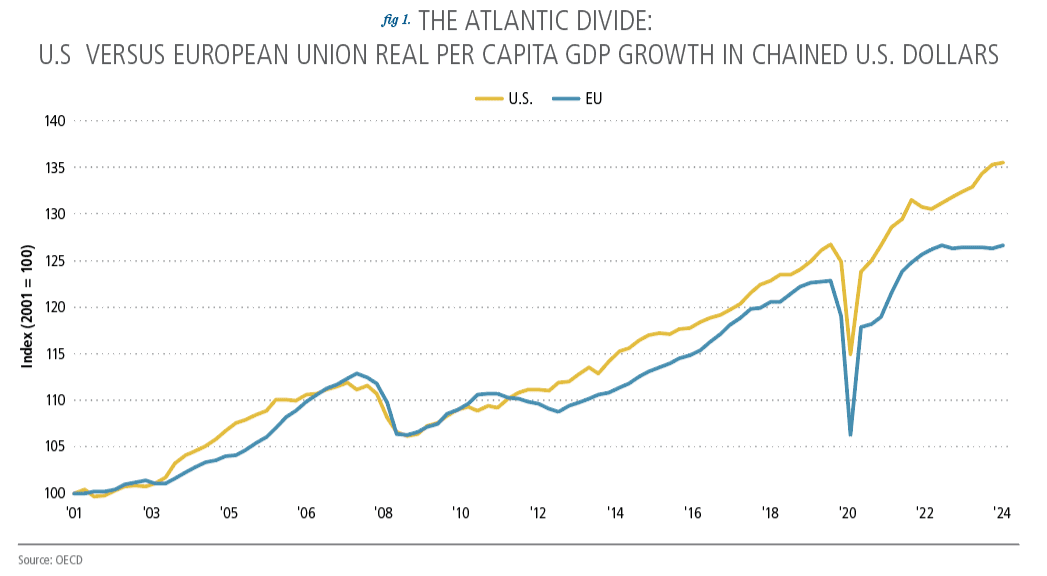

Quips aside, Europe trails the U.S. economically and has fallen further behind in recent decades. Since 2000, the U.S. economy has grown by 68%, while the EU economy has grown by just 40%.

Since the turn of the century, America's per capita GDP—the all-important measure of economic well-being—has increased by 36%, compared to just 27% for Europe (see Figure 1).

Full disclosure: Many of these worrisome data points are not our own; we borrowed liberally from a recent report by Mario Draghi, the famous former European Central Bank (ECB) President, temporary Italian Prime Minister, and former Goldman Sachs banker.

What explains the widening economic gulf between the U.S. and the EU, and what can be done? The purpose and intent of the following essay are to answer such questions.

What Explains The Gap?

Draghi doesn’t sugarcoat the story when detailing why Europe languishes, and it can all be summed up in one word—innovation (or the lack thereof).

Innovation (mostly technological advancement) leads to higher productivity, which boosts potential output growth. Transformative innovations in modern history have been key drivers of long-run growth: railroads in the 1860s, assembly lines and automation in the 1920s, the internet in the 1990s, and possibly artificial intelligence (AI) today.

Europe has lagged behind the U.S. on various measures of innovation. Since 2019, new business registrations in the U.S. have increased by 35%, compared to the euro area’s 7% over the same five-year span.1

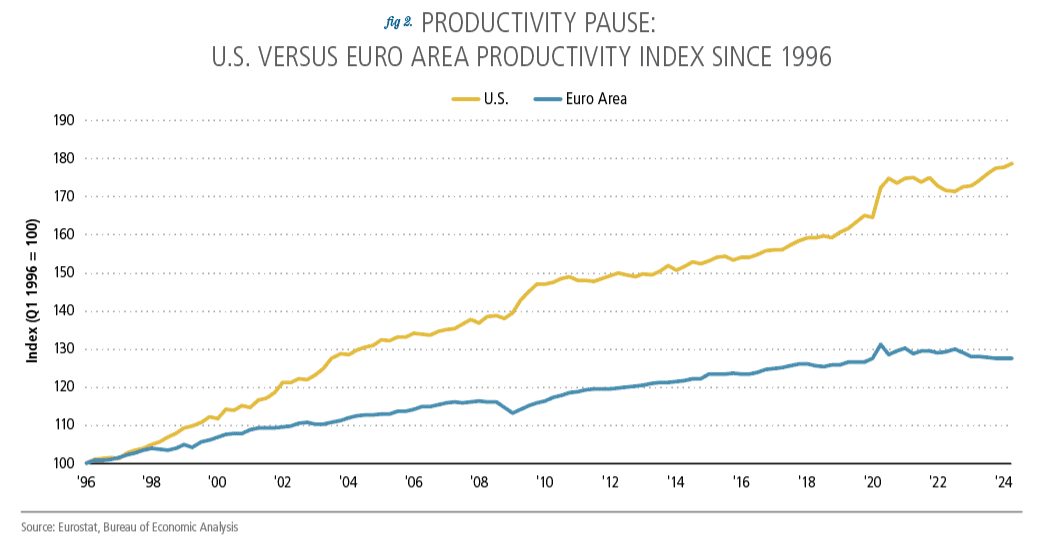

Europe has also been far less productive than the U.S. in recent decades. Although productivity growth in Europe was on par with the U.S. until 1995, U.S. cumulative productivity has outpaced the growth in Europe by almost threefold as of the second quarter of 2024 (See Figure 2).2

Where exactly has Europe lagged? The productivity of the euro area fell short of its pre-pandemic trend in almost all sectors except for public administration and finance.3 Compared to the U.S., according to Draghi, the EU tech sector is the lagger, as “EU productivity growth over the past twenty years would be broadly at par with the US” if the tech sector’s contribution to total productivity were excluded.4

And, the future of the EU tech sector's productivity is not looking so bright. The U.S. already accounts for nearly 70% of all AI models developed since 2017 and more than 70% of the world’s computing capacity.5

Innovations Require Inputs

Innovations don’t magically happen—they require inputs, including the energy used to power production, the capital needed to equip research labs, and the resources that would foster the next generation of innovative leaders. Unsurprisingly, Europe struggles with all three building blocks of the innovative process.

First, energy costs are prohibitive to growth. Europe's position as a net energy importer makes it vulnerable to price fluctuations. According to Draghi, European companies face energy costs that are 30 percentage points higher than U.S. companies face on average, which has caused energy-intensive industry production to fall nearly 15% since 2021.6

Unfortunately, energy requirements for growth will only increase. In addition to the already energy-intensive industrial sectors, data center power demand will experience exponential growth, with AI computing at the forefront of every novel service sector business.

Second, European research and development (R&D) spending remains stale and stagnant. American R&D has transitioned from spending on automobiles in the early 2000s to software companies in the 2010s and now to digital and AI sectors. However, over the same time, automobile industries have dominated Europe’s R&D investment.

Lastly, Europe faces an education gap. The American education system is more market-oriented than Europe’s. For example, Silicon Valley's location near top research universities (e.g., Stanford and UC Berkeley) has resulted in an innovation cluster where firms take advantage of the network to recruit top talent. According to Draghi, “Europe has no innovation ‘clusters’ in the top 10 globally, while the U.S. has four and China has three.”

The Scaling Issue

High energy costs and a lack of R&D spending restrict the growth of mature companies and prevent new ones from forming. But even the few successful startups face difficulty “scaling up.” Draghi places the blame squarely on Europe’s fragmented financial system and industrial environment.

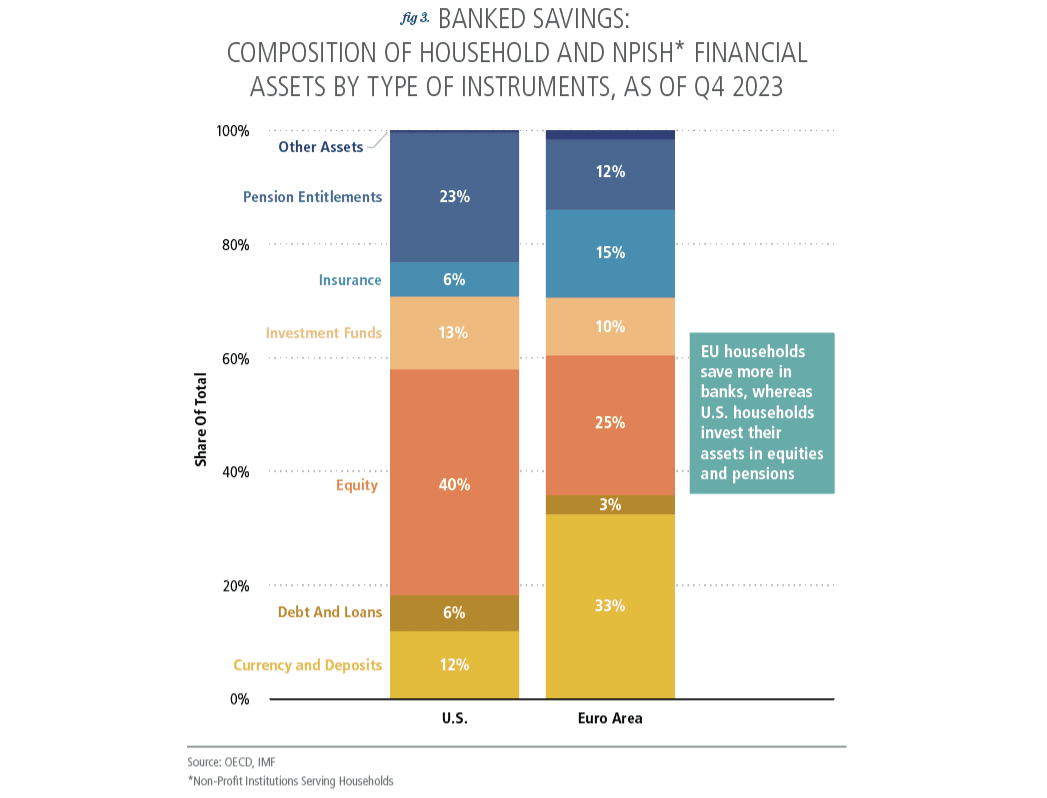

Europe’s capital resources are heavily concentrated in banks (62% in Europe compared to 29% in the U.S.).7 Risk-averse banks have higher liquidity needs and lend primarily to mature companies. Meanwhile, other non-bank capital resources, such as private pensions, serve as the primary funding source for start-ups through the venture capital and private equity markets.

However, there is a lack of private funds in Europe, and, as a result, from 2013 to 2023, only $150 billion of venture capital funds were raised in Europe, compared to $924 billion raised in the U.S.8

So, why aren’t EU households investing in private funds? Well, public or government-managed pensions are a more prevalent form of retirement savings in Europe than private pension plans. Further, European residents prefer to leave a larger majority of their assets in banks than their U.S. counterparts, partly due to lower return expectations from other forms of investment (see Figure 3).

In addition, pensions that invest across borders (the majority of pensions) get penalized by taxes and capital restrictions. For example, out of the 27 EU member states, 18 have direct foreign investment restrictions, and 12 actually tax foreign pension funds.

The result from the lack of venture capital funding is clear: “There is no EU company with a market capitalization over EUR 100 billion that has been set up from scratch in the last fifty years, while in the U.S., all six companies with a valuation above EUR 1 trillion have been created over this period.”9

What’s more, firms founded in Europe often relocate to the U.S. to access cheaper and more varied forms of funding. According to Draghi, out of the 147 “unicorns” started in Europe, 40 relocated abroad, primarily to the U.S. Losing local startups leads to productivity contraction, job losses, and reduced local industry competitiveness.

Industry fragmentation across Europe is also rampant. European lawmakers tend to dislike mergers and acquisitions between firms. Nearly 70% of workers are employed in small or mid-sized firms (fewer than 250 employees), whereas in the U.S., the share shrinks to 40%.10 The fragmentation prevents intercorporate investments and blocks the efficient transfer and capitalization of new technologies (see Did You Know? Box: Aspire To Acquire).

Did You Know?

Aspire To Acquire

Contrary to the common perception, mergers and acquisitions (and spinoffs, too) have proven to be necessary steps for corporate growth. For example, many large tech firms in the U.S. today (e.g., Amazon, Apple, and Google) have reached their current size through numerous acquisitions. Google (or Alphabet), the youngest of the three, has acquired 258 firms since its birth, enabling products ranging from Google Maps to Gemini AI. EU regulators have fined Google at least $10 billion in antitrust cases since 2010—which hasn’t stopped it and other hyperscalers from accounting for 70% of global internet traffic.13 So, why do acquisitions accelerate business growth? Acquiring competitors (horizontal integration) allows for increased revenue, cost synergies, and more innovative resources within the industry. Acquiring your suppliers (vertical integration) lowers costs significantly. Acquiring outside of your sector allows you to integrate and diversify business operations. Who wouldn’t be up for that?

Practical Steps Forward

While clearly addressing the problems plaguing Europe, Draghi also proposes some ways forward. As students of financial markets and financial institutions, we’ll focus on one area near and dear to our hearts: the financial fragmentation across the EU.

Financial market unification is a key step to allowing more cross-border capital movement and ensuring efficiency in capital allocation. However, the EU lacks a single securities market regulator and a single rulebook for all aspects of trading. Current organizations, such as ESMA, coordinate only among national security market regulators rather than issuing a single set of regulations like those issued by the U.S. Securities and Exchange Commission. Consequently, supervisory practices and interpretations of regulations in the EU are greatly varied.

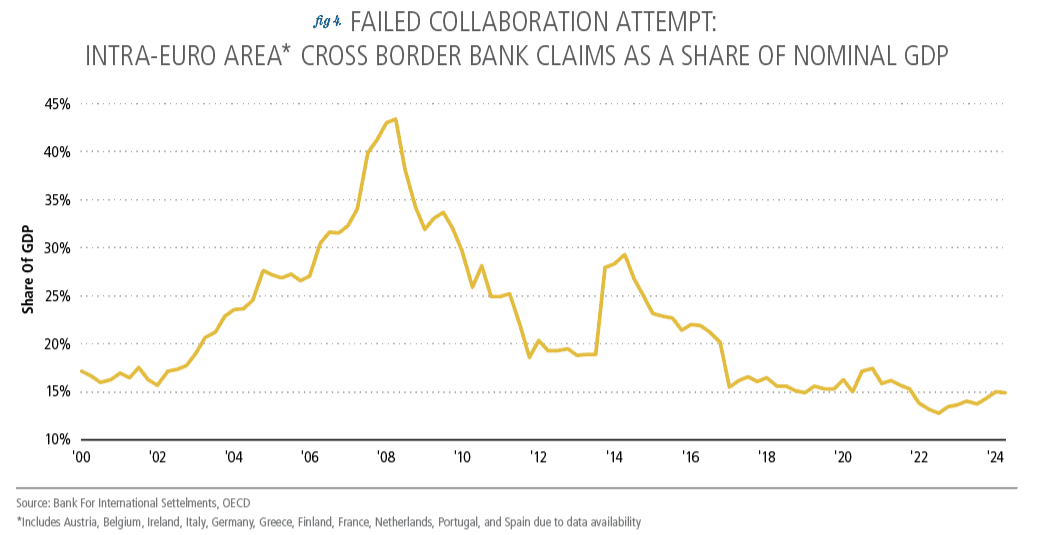

In addition, tax and foreign investment restrictions across member states should be unified, as substantially unaligned policies will limit cross-border capital flows. Cross-border bank claims within the major 11 euro area countries fell from 43% of GDP before the global financial crisis (GFC) to only 15% in Q2 2024 (see Figure 4).

A freer flow of capital across borders would improve capital allocation, as larger pools of private capital allow investors to take on more risks for potentially higher returns, creating funding opportunities for start-ups.

Hopeful Notes For Tomorrow

Draghi has identified some key reasons for Europe’s underperformance: higher energy costs, low R&D spending, and the lack of a market-oriented education system. Further, heavy antitrust regulations have prevented innovative start-ups from scaling up, while financial market fragmentation prevents start-ups from receiving sufficient funding.

Consequently, further financial integration and removing cross-border investment restrictions might be the most practical steps forward.

Of course, we understand that financial integration is easier said than done, as revising regulations may take years.

However, comparisons with the U.S. only serve as a benchmark. The goal of the EU financial market is not to replicate America’s innovation success but to take away and employ its advantages.

For example, the EU is already a leading player in sustainable and digital finance. Further, Europe is home to ASML Holding, the sole supplier of extreme ultraviolet (EUV) lithography machines required to manufacture the most advanced chips.

As a firm recently expanding its presence in Europe with an office in Milan, we have significant investments in Europe's future. While it may take time for Europe to turn things around, we are rooting for its success.

Endnotes

Eurostat, U.S. Census Bureau. The euro area refers to the 20 countries out of the 27 members of the European Union (EU) that have adopted the euro and the ECB as their central bank.

Draghi, M., The Future of European Competitiveness.(2024). Brussels, Belgium; European Commission. Retrieved from: https://commission.europa.eu/topics/strengthening-european-competitiveness/eu-competitiveness-looking-ahead_en?prefLang=fr#paragraph_47059

Bergeaud, A. (2024). The Past, Present, And Future of European Productivity. European Central Bank. https://www.ecb.europa.eu/pub/pdf/sintra/ecb.forumcentbankpub2024_Bergeaud_paper.en.pdf

Draghi. (2024). Part A, Chapter 2. “Closing the innovation gap.” Page 20.

Microsoft, Google, Amazon, Meta, Apple

Draghi. (2024). Part A, Chapter 3. “A joint decarbonisation and competitiveness plan.”Page 35.

Arnold, N. (2024). Stepping Up Venture Capital to Finance Innovation in Europe. IMF Working Papers, 2024(146), 20. https://doi.org/10.5089/9798400280771.001

ibid

Draghi. (2024). Part A, Forward. Page 2.

Ibid

Draghi. (2024). Part A, Chapter 6. “Strengthening Governance.” Page 65.

Ip, G. (2024, January 31). Europe Regulates Its Way to Last Place. Wall Street Journal. https://www.wsj.com/economy/europe-regulates-its-way-to-last-place-2a03c21d

Alcantara, C., Schaul, K., De Vynck, G., & Albergotti, R. (2023, September 26). How Big Tech Got So Big. Washington Post. https://www.washingtonpost.com/technology/interactive/2021/amazon-apple-facebook-google-acquisitios/

This material reflects the firm’s current opinion and is subject to change without notice. Sources for the material contained herein are deemed reliable but cannot be guaranteed. This material is for illustrative purposes only and does not constitute investment advice or an offer to sell or buy any security. Past performance is no guarantee of future results. Point of View articles may not be reprinted without permission. We welcome your comments and feedback at editor@payden.com.

This material has been approved by Payden & Rygel Global Limited which is authorised and regulated by the Financial Conduct Authority. This material has been approved by Payden Global SIM S.p.A.. which is authorised and regulated by CONSOB.