“Made in China (中国制造)” became popular in the 1990s as China became the world's manufacturing hub for lower-value and lower-tech consumer products. The affordability of “Made in China” goods has also made the phrase a stereotype for lousy quality.

But in 2024, China redefined “Made In China” by rapidly overtaking competing countries in the electric vehicle (EV) industry. China surpassed Germany as the world’s largest automobile manufacturer through EVs, with Chinese EVs representing 60% of total EV production worldwide.1

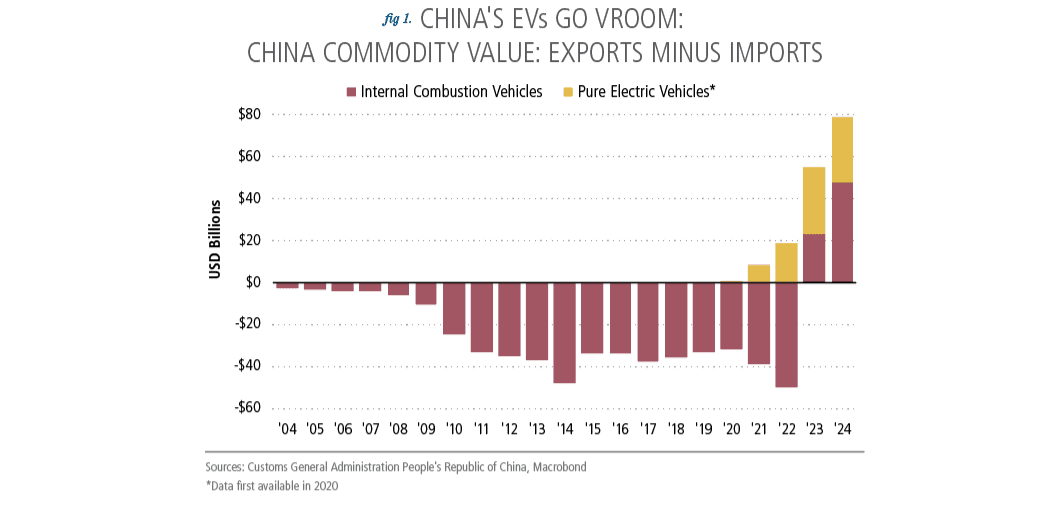

More shockingly, 2024 marks only the second year since China first transitioned from a net automobile importer to an exporter (see Figure 1).

Is China’s EV success a one-off? Or can its automotive strategy be replicated in other sectors?

EVs represent just one success story within China's broader high-tech ecosystem. By uncovering China’s EV roadmap, we explore how a government-influenced tech ecosystem can rival America's tech giants.

Three Steps Of China’s EV Roadmap

Chinese EV ascendancy did not happen by accident, however. EVs are one successful product resulting from China’s three-step industrial strategy.2

The first step is technology transfer, more formally known as market share in exchange for technology (市场换技术). In particular, technology transfer has been key for China’s traditional auto sector. Nearly 70 joint ventures with foreign car companies were formed in the 1980s, allowing foreign companies to access the Chinese consumer base in exchange for training Chinese engineers.3 Fast forward to 2018, and Tesla's establishment of its first overseas factory in Shanghai allowed Chinese EV production know-how to leapfrog ahead. Tesla received generous government subsidies in exchange for knowledge of Tesla’s EV manufacturing model and technology, such as the “Giga press,” a special casting machine for EV parts.

The second step is adaptation or a top-down-driven strategy for devoting resources to the newly acquired technology. Led by China’s Minister of Technology and Science, Wan Gang (万钢), China invested around 100 billion renminbi (or 14 billion U.S. dollars) in EV and EV battery companies from 2007 to 2019, accounting for one-third of overall sales during the same period. Subsidies ranged from sales tax exemptions to public transportation projects (Did You Know? Box: Buy EVs Or Wave Bye-Bye). The Chinese government also heavily incentivized extensive research in battery technology, which became the key to Chinese EV success (more on this later).

Did You Know?

Buy EVs Or Wave Bye-Bye

Electric Vehicle (EV) subsidies in China are not limited to producers. China began influencing consumers using consumer rebates long before the U.S. government first granted tax credits for Teslas. The current Chinese tax rebate of 12,800 yuan per vehicle is equivalent to an average 10% discount. Moreover, in large Chinese cities, purchasers of internal combustion cars have to enter a lottery to get a license plate. While the lottery process will prioritize households with more children, internal combustion vehicles could still be subjected to road space rationing. In contrast, “green” license plates for EV users are ready upon purchase. On top of being legally able to drive the car on the road, artificially depressed electricity prices at charging ports are a bonus. Sounds like a case of buy EVs or wave Bye-Bye!

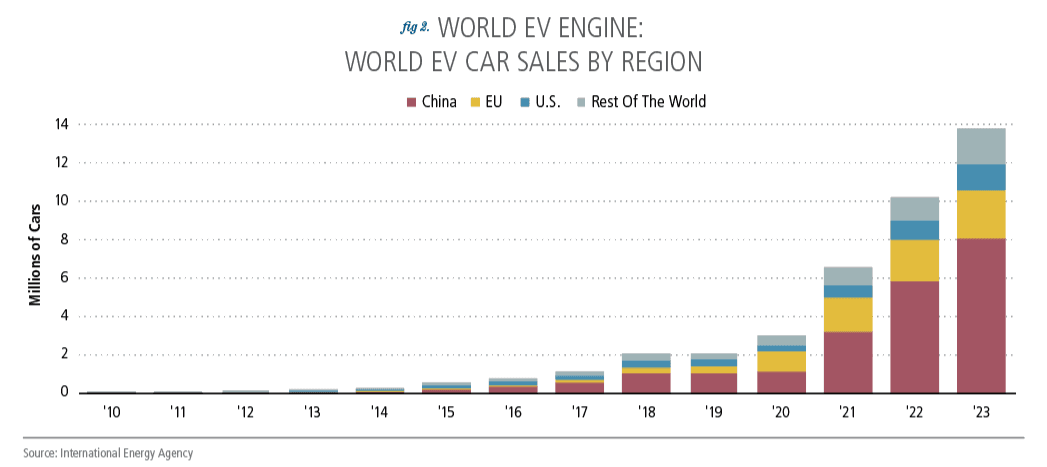

The third and final step is “going global” (走出去). After Chinese companies had mastered foreign technologies and improved upon them to exercise their cost advantage, they first replaced foreign firms domestically, then advanced to penetrating foreign markets. Evidently, from 2017 to 2024, the share of foreign automaker sales in China dwindled from 70% to 40%, whereas domestic EV car sales in China grew at an average annual rate of 60% during the same period.4 Chinese EVs now comprise over 60% of total world EV sales (see Figure 2).5

The Formula Behind The Price Tag

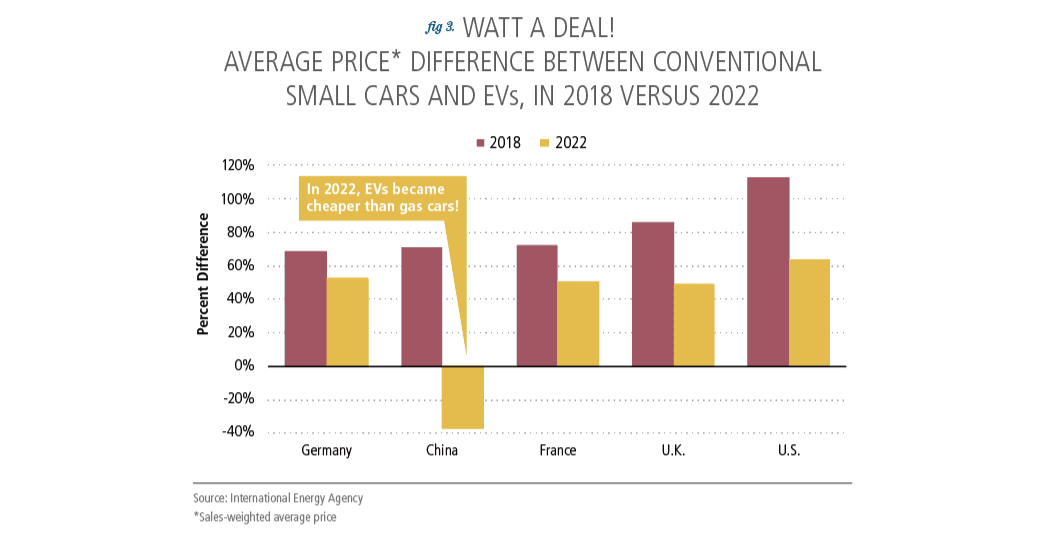

A key characteristic that has allowed Chinese EVs to “go global” is their low price.

On average, EVs are 33% cheaper than conventional cars in China, whereas EVs are at least 40% more expensive than traditional cars in the U.S. and Europe (see Figure 3). Further, even at a 100% premium, an imported Chinese BYD EV is still 10% cheaper in Germany than a domestically produced Volkswagen EV with similar features.6 No wonder the EU has already slapped tariffs on Chinese EVs!7

So, how exactly did Chinese EVs get so cheap? Not through lower labor costs—average labor costs have increased by 60% in China in the past seven years, but the average price of EVs has decreased by 50% over the same period.

The abovementioned technology transfers are just part of the reason, but the key behind the EV price tag is cheaper batteries and China’s domination of the entire EV manufacturing supply chain.

First, China is a leading producer of cost-effective lithium iron phosphate (LFP) batteries, which have lower energy capacities than the more widely used lithium nickel manganese cobalt (NMC) batteries.

However, after a decade of research, Chinese producers began using a cell-to-pack technology to improve the energy density of LFPs while maintaining lower costs. Over the past decade, LFP battery costs have decreased by 82%, and in 2023, LFP batteries accounted for more than 40% of the global battery demand.8

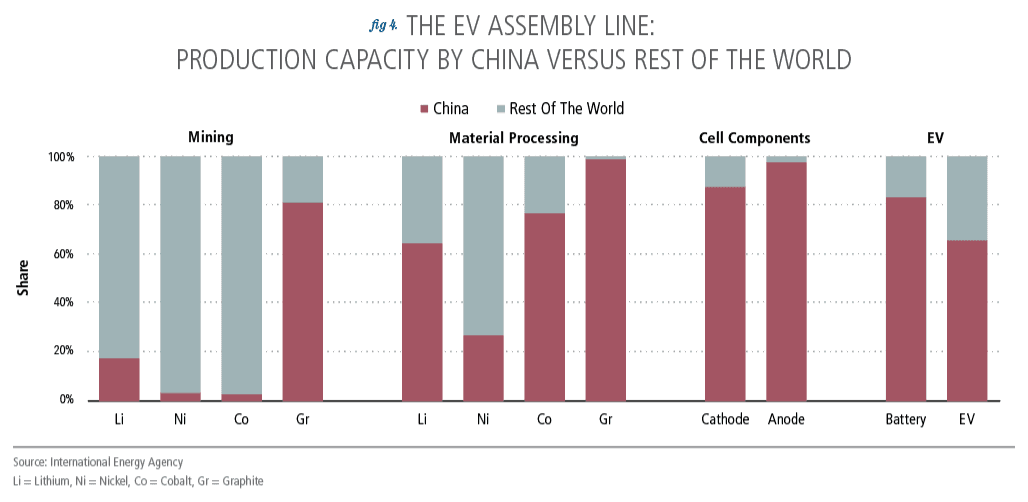

Second, China became a dominant player in all manufacturing stages of EVs, amplifying cost synergies. Aside from supplying over 90% of battery production, China dominates the market in graphite mining and has hefty investments in African lithium mines and Indonesian nickel producers. China also has the largest global market share in raw material processing for critical metals used in EV battery production, including lithium, nickel, cobalt, and graphite (see Figure 4).9

“Multi-Tech”-ing With EVs

Lest you think EVs are China’s one-off breakthrough, it’s just one of many within China’s constellation of tech firms forming an entire ecosystem.

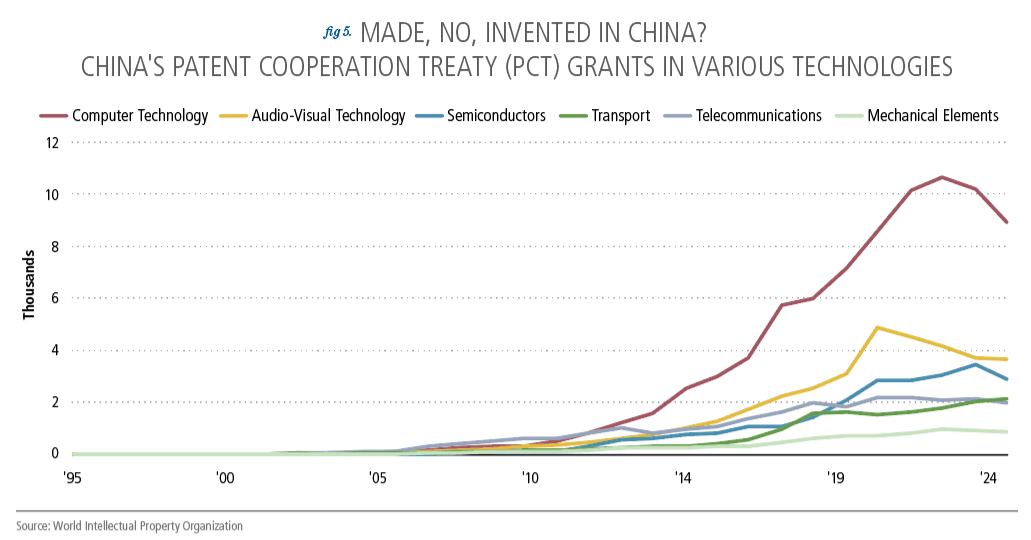

Most of China's tech giants have embraced multiple frontier technologies simultaneously to exploit their underlying similarities. Perhaps as a result, Chinese companies have rapidly accelerated innovations in various traditional and front-end technologies in recent years (see Figure 5).

Large phone manufacturers in China, such as Xiaomi (小米) and Huawei (华为), also produce EVs. Phone makers have a natural advantage when it comes to developing the user interface hardware (such as touch screens) used in EVs and integrating them with the internet and, eventually, with other cars.10

Manufacturing EVs also unleashed autonomous driving technology. Baidu (百度), the “Google” of China, released its first robotaxi, Apollo Go, in 2022 (Does it remind you of Waymo, the self-driving car owned by Alphabet? See our Waymo article in Vol 4, 2024 PoV). The latest Apollo Go model, released in May 2024, is five times cheaper than producing a Waymo in the U.S., and Baidu has already deployed hundreds of them in China.11

Navigating The Future

EV technology is also paving the way for new technological frontiers.

For example, EV manufacturing companies like Li Auto (理想汽车) and XPeng (小鹏汽车) have invested heavily in robotics. Perception and interaction sensors, algorithms, and lidar cameras are all key inputs to industrial (and humanoid) robotics. The same supply chain domination used for EVs thus gave China a headstart in robotics, as China also controls 63% of the key companies in the global supply chain for humanoid-robot components.12

Moreover, Huawei, China’s primary information and communication infrastructure provider, is also developing drones. Huawei was already producing the key inputs to drone manufacturing: batteries and drone parts. With its advantage in network-providing infrastructure, Huawei has now begun low-altitude commercial drone deliveries, a feat Amazon has also started to employ, but only in a few localities (partly due to safety regulations in the U.S.).

We can go down the list, but you get the gist. “Multi-teching” is not only a U.S. tech giant phenomenon!

Can History Repeat Itself?

As China expands its manufacturing scope to frontier technologies beyond EVs, artificial intelligence (AI) and semiconductors are at the center of investors’ focus. But, with the U.S. currently leading the way, the common perception is that China won’t be able to catch up as it did with EVs.

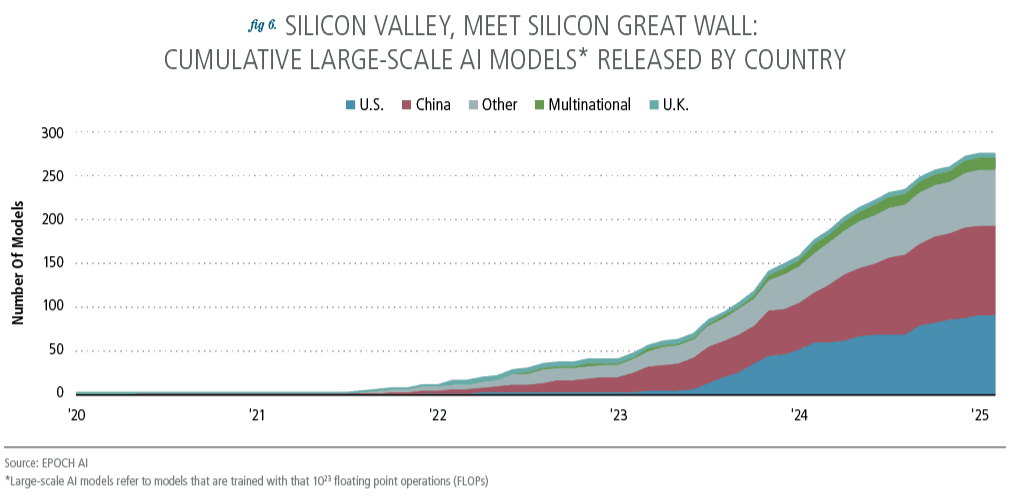

All might not be lost, though. As with the story of EVs, despite its limited ability to manufacture cutting-edge chips, China has published as many notable large language models (LLMs) as the U.S. (see Figure 6).

Further, semiconductors are already an integral part of China’s technological infrastructure. China dominates over 80% of rare earth element processing, including key semiconductor inputs such as low-grade gallium, tungsten, and magnesium.13 With the Chinese government pumping money into the semiconductor sector at a rate equivalent to a CHIPS Act every year since 2014, the number of semiconductor design companies increased sixfold between 2010 and 2022.14

Although other challenges remain, the frontier technology business model of EVs provides a blueprint for other emerging technologies, including semiconductors and machine learning.

Just as no one thought China could dominate the global EV market 20 years ago, the global manufacturing powerhouse may soon expand into other technological frontiers.

Endnotes

International Energy Agency (IEA). (April 2024). Global EV Outlook 2024. Paris. https://www.iea.org/reports/global-ev-outlook-2024, Licence: CC BY 4.0

Chan, Kyle. (February 2025). Testimony before the U.S.-China Economic and Security Review Commission: Hearing on “Made in China 2025—Who Is Winning?”. www.uscc.gov/sites/default/files/2025-02/Kyle_Chan_Testimony.pdf

Ibid.

Ibid.

IEA. Global EV Outlook 2024.

Sebastian, G., Barkin, N., Kratz, A. (April 2025). “Ain’t No Duty High Enough.” Rhodium Group. https://rhg.com/research/aint-no-duty-high-enough/

In October 2024, EU members voted to impose a five-year duty of 17% on BYD, 18.9% on Geely, and 35.3% on SAIC. BYD, Geely, and SAIC are among the largest Chinese EV producers. Other cooperative companies will be subject to a 20.7% countervailing duty.

Catsaros, O. (November 2023). “Lithium-Ion Battery Pack Prices Hit Record Low of $139/kWh.” Bloomberg NEF. https://about.bnef.com/blog/lithium-ion-battery-pack-prices-hit-record-low-of-139-kwh/

Sedgman, P., Hong, J., Lew, L. (September 2023). “China’s Stranglehold on EV Supply Chain Will Be Tough to Break.” Bloomberg. www.bloomberg.com/graphics/2023-breaking-china-ev-supply-chain-dominance/?embedded-checkout=true.

Chan, Kyle. (January 2025). “China's Overlapping Tech Industrial Ecosystems.” High Capacity. www.high-capacity.com/p/chinas-overlapping-tech-industrial.

Hawkins, A. J. (November 2024). “Baidu’s Supercheap Robotaxis Should Scare The Hell Out of the US.” The Verge. www.theverge.com/2024/11/22/24303299/baidu-apollo-go-rt6-robotaxi-unit-economics-waymo.

Chen, C. (February 2025). “China’s EV Giants Are Betting Big on Humanoid Robots.” MIT Technology Review. www.technologyreview.com/2025/02/14/

1111920/chinas-electric-vehicle-giants-pivot-humanoid-robots/.

Caines, Colin, Sharon Jeon, and Cheyenne Quijano (January 2025). "Developments in Chinese Chipmaking," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, January 17, 2025, https://doi.org/10.17016/2380-7172.3647.

Ezell, S. (August 2024). “How Innovative Is China in Semiconductors?” Hamilton Center on Industrial Strategy. Information Technology and Innovation Foundation. https://itif.org/publications/2024/08/19/how-innovative-is-china-in-semiconductors/.

This material reflects the firm’s current opinion and is subject to change without notice. Sources for the material contained herein are deemed reliable but cannot be guaranteed. This material is for illustrative purposes only and does not constitute investment advice or an offer to sell or buy any security. Past performance is no guarantee of future results. Point of View articles may not be reprinted without permission. We welcome your comments and feedback at editor@payden.com.

This material has been approved by Payden & Rygel Global Limited which is authorised and regulated by the Financial Conduct Authority. This material has been approved by Payden Global SIM S.p.A.. which is authorised and regulated by CONSOB.