It’s been more than half a century since U.S. President Richard Nixon shocked the world, de-linking the U.S. dollar from gold and slapping 10% across-the-board tariffs on the whole world, in a hastily prepared Sunday night televised address on August 15, 1971.1

Did the announcement mark the end of the U.S. dollar as the global reserve currency?

Far from it. Instead, the dollar became more popular in the ensuing decades.

The best-laid plans of Presidents and policymakers often amount to little in the face of global economic forces.

A similar story may be playing out today. Stablecoins are cryptocurrencies that aim to maintain a fixed par value (usually 1 USD), but with the same innovative features as Bitcoin and other cryptocurrencies, operating 24 hours a day, seven days a week, and using decentralized, real-time settlement.

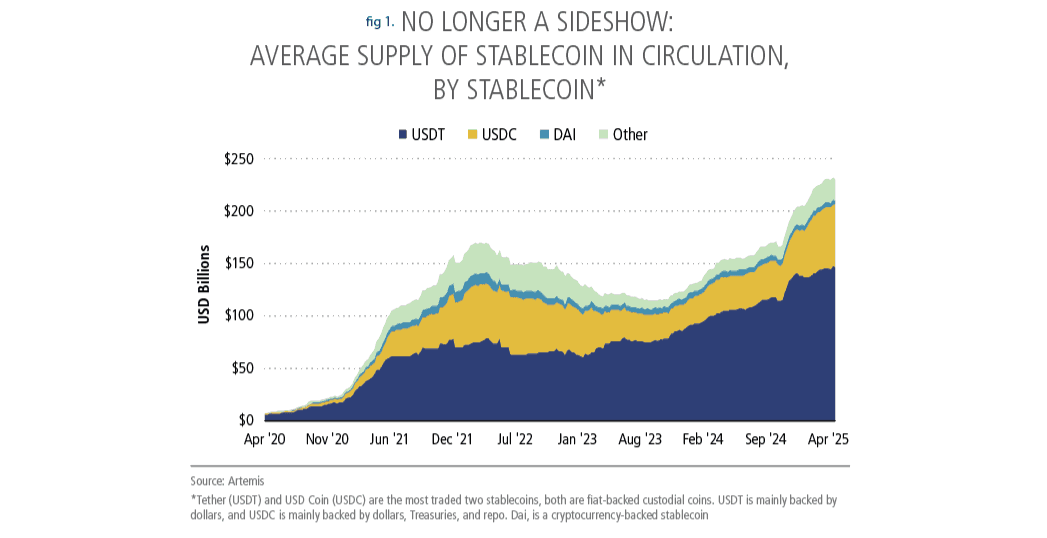

Sideshow, you say? The stablecoin market value is rapidly approaching $250 billion (see Figure 1). Further, daily trading volumes of major stablecoins total $24 billion, approaching Bitcoin’s $34 billion and already more than Ether’s $17 billion.

What should investors think about these new-fangled coins? To answer, we evaluate stablecoins by examining an interesting historical precedent: eurodollars. Eurodollars enable people to hold dollars outside the U.S. While eurodollars are predominantly the province of a wealthy elite who can maintain accounts at Midland Bank in London or have a numbered account in Zurich, this time around, it’s different. Stablecoins are already onboarding the entire world to the U.S. dollar system.

Let’s take a brief tour through financial history to put stablecoins into context.

Eurodollars: A Brief History

A eurodollar is a U.S. dollar deposit in a non-U.S. bank or a U.S. bank's overseas (foreign) branch.

There are two key differences between a eurodollar and a dollar deposited in the U.S.: first, foreign banks holding the deposits aren’t subject to the same banking regulations as U.S. banks; and second, the FDIC does not insure the offshore dollar deposits.

After World War II, several factors fueled the rise of the eurodollar market. Initially, U.S. Regulation Q, or Reg Q, capped the maximum interest paid on domestically held deposits, which sent deposits overseas in search of yield. Later, as the Cold War raged on, the Soviets needed U.S. dollars to purchase global commodities, but keeping a bank account in the U.S. did not seem like the best option. Consequently, they deposited dollars in the Soviet-owned Banque Commerciale pour l’Europe du Nord in Paris. The bank was known as BCEN-Eurobank, hence its dollar deposits became known as “Eurobank dollars” and later just “eurodollars.”2

Further, U.K. banks also began taking dollar deposits in the 1950s to make money. One example was the Midland Bank in London, which took in dollar deposits and invested the proceeds in UK money markets, as U.K. interest rates were above comparable U.S. interest rates throughout the 1950s. At one point, the U.K. bank deposit rate was almost 200 basis points higher than the fed funds rate.3

A widening U.S. trade deficit also funneled dollars into global circulation. At the same time, post-war rebuilding programs, like the Marshall Plan, meant additional dollars flowed into Europe.

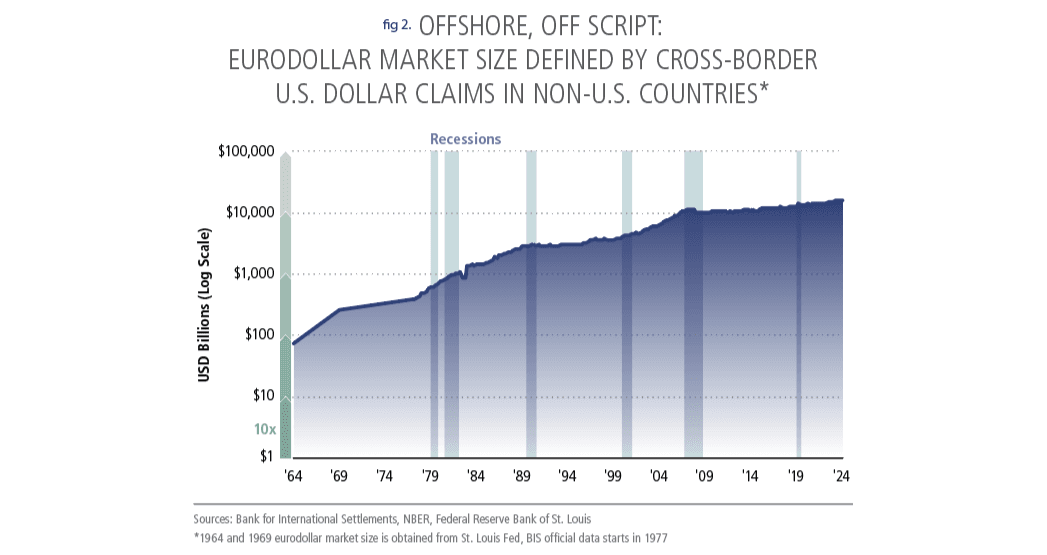

As a result, the eurodollar market size increased fivefold from 1960 to 1970, with about $50 billion in eurodollars sloshing overseas by the end of the decade (see Figure 2).4 Interestingly, adjusted for inflation in today’s dollars, the eurodollar market would have stood at $264 billion in 1969, roughly the size of the stablecoin market today!5

Policymakers and presidents have always been uneasy with the offshore arrangement, fearing that the pool of “offshore” dollars posed the risk of a run on the U.S. dollar and threatened its peg with gold.6 In fact, it was partially the threat of “offshore dollars” that drove President Nixon’s decision to de-link the dollar from gold on August 15, 1971.

While Nixon’s sudden move shocked the world and sent the dollar tumbling, it didn’t end the dollar’s reign. If anything, Nixon‘s closing of the gold window pushed more dollars offshore! By the late 1980s, dollar balances overseas grew to $1.7 trillion. Today, the eurodollar market stands at $16 trillion, which is three times as many dollars held offshore as in U.S. bank deposit accounts (see Figure 2)!7

As a natural consequence, as dollars abroad grew, offshore banks found creative ways to earn returns on these dollars, such as making loans and conducting repos, buying corporate commercial paper, and asset-backed commercial paper, which later became ground zero for the 2008 global financial crisis. The abundance of eurodollars also led to the rise of the “eurobond” market. The first “eurobond” issue was $15 million of USD “bearer bonds” yielding 5.5% for 15 years to finance a roadway in Italy.8 Today, “eurobonds” are a ~$13 trillion market.9

The Stablecoin Landscape

Interestingly, stablecoins mirror many aspects of the eurodollar evolution in the 20th century.

First, financial innovation often occurs due to market needs rather than careful design. Like eurodollars, which were born from the need of foreign countries to hold U.S. dollars, stablecoins were born from the need to move value (or your “money”) across crypto exchanges quickly and cheaply, as major cryptocurrencies like Bitcoin were too volatile or too valuable to sell. Stablecoins were born as a “stable” form of crypto that can be efficiently transferred across various exchanges without converting digital currency back to government-backed currency.

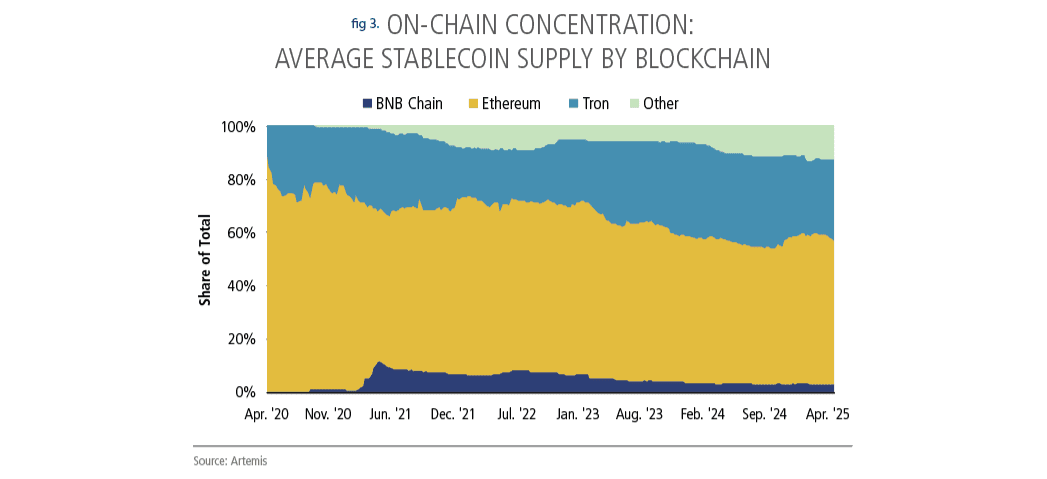

Second, the principal definition of a eurodollar is a dollar deposit held “offshore.” A stablecoin is a dollar held (custodied) on a blockchain. So, while eurodollars are “offshore private dollar deposits,” stablecoins are “on-chain private dollar deposits” (see Figure 3).10

But are stablecoins really “dollars,” you ask?

Well, 95% of stablecoins are “fiat-backed.” Examples include Tether (USDT) and USD Coin (USDC), both of which promise to back deposits one-for-one with high-quality reserves (e.g., cash, T-bills, money market assets, etc.).11 In turn, stablecoin issuers are already major buyers of U.S. debt. Today, stablecoin issuers hold over $120 billion in T-bills, making them the 17th largest holders of U.S. Treasuries.12

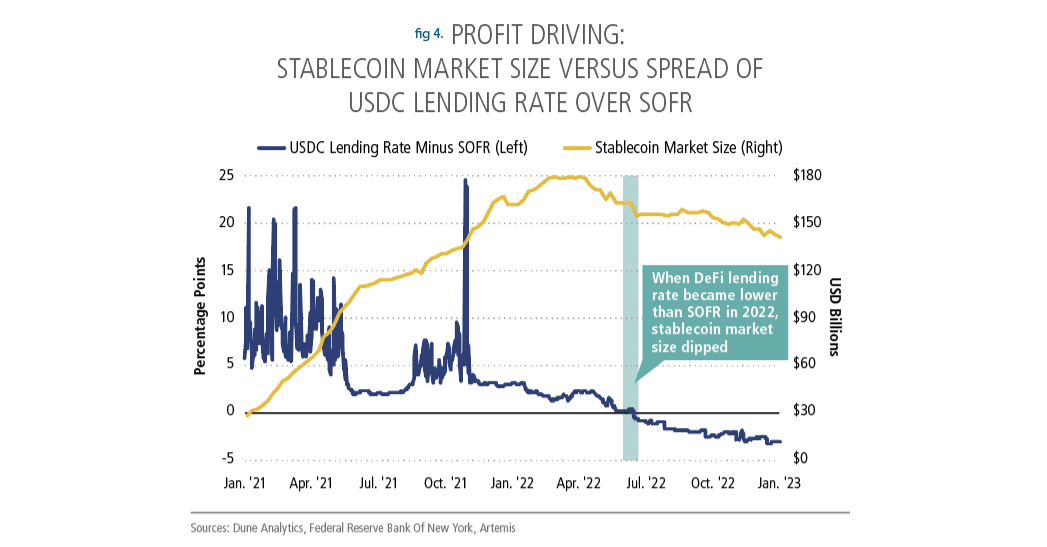

Third, just as with the eurobond market born out of the eurodollars, on-chain and off-chain worlds have collided, as stablecoin investors take advantage of lending rates offered in decentralized finance (DeFi; the blockchain borrowing and lending market), often earning a spread above traditional overnight rates.

For example, throughout the early stage of the post-Covid-19 era, the DeFi-SOFR spread, indicating that yields generated from “on-chain lending” (lending in crypto) were higher than “real world” lending in the money markets, and the growth of the stablecoin market cap took off (see Figure 4).

Comparative Advantage

While similar to eurodollars in their functionalities, stablecoins have many uses and advantages compared to eurodollars, which may enable them to become an even larger “offshore” market than eurodollars. Think of the move from coins to cash to electronic payments. Stablecoins appear to be the next step in the evolution.

First, there’s speed. Stablecoins already offer near-instant settlement 24 hours a day, 7 days a week. Your author recently moved money across the globe instantly on a Sunday afternoon, just as easily as he sent a WhatsApp message to a friend in London.

Second, stablecoins are cheap. The average global remittance fee for all payment channels is 6.35% of the transfer amount. However, the maximum remittance cost for stablecoins is 3%, with the lowest at only 0.5% of the transfer amount.13

Third, stablecoins are transparent. Any payment made on a public blockchain can be tracked by the sender, recipient, and any relevant regulatory body. Consequently, stablecoins are easier to regulate than their predecessor, eurodollars. And, as we head into the age of AI “agents,” machine-to-machine transactions will take off and likely dwarf the quantity of human-to-human transactions. So, the need for a stable currency to process payments quickly and cheaply will be higher than ever.

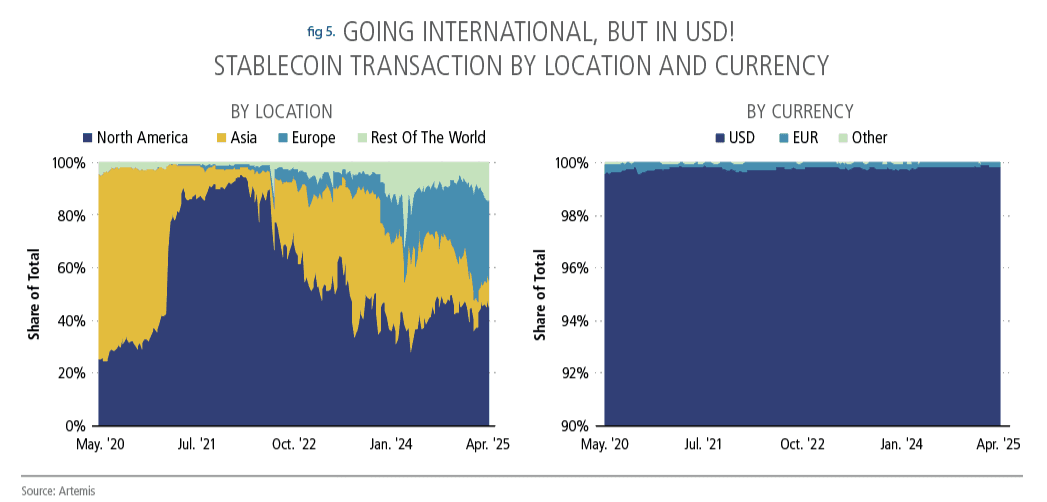

Fourth, unlike eurodollars, which can be held only by those who have access to elite European banks, stablecoins are accessible to anyone who has internet access. In 2021, 90% of stablecoin transactions happened in the U.S. By April 2025, Europe, Asia, and Southeast Asia have become rising locations of stablecoin use. Interestingly, 99.5% of all global stablecoin transactions are conducted with, you guessed it: a USD-denominated stablecoin (see Figure 5)!

The above combination of traits will likely unleash uses we’ve yet to consider. Today, corporate treasury departments are already using stablecoins to move money internationally. SpaceX, for example, is collecting payments for Starlink using stablecoins.14

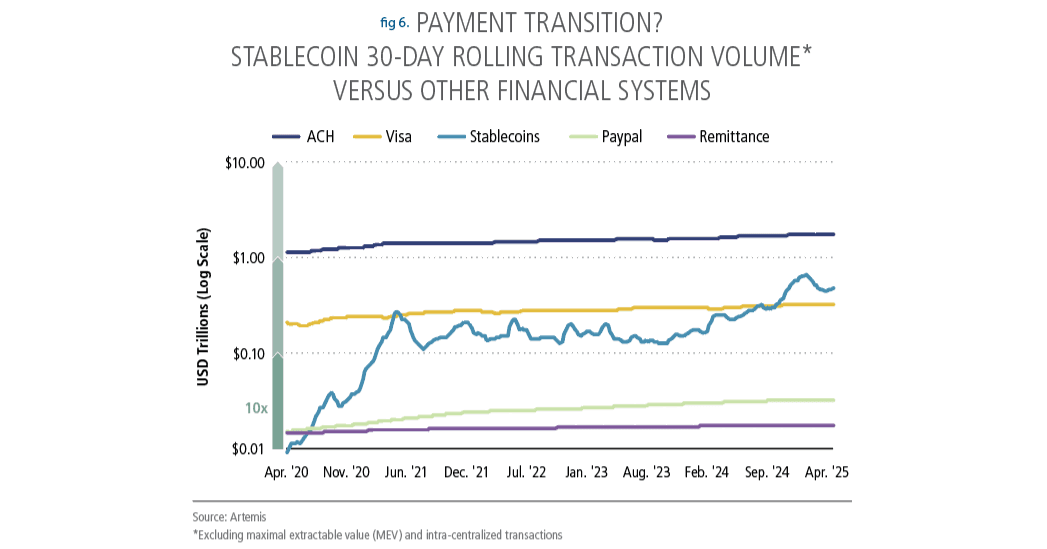

Stablecoins’ average transaction volume increased from $10 billion a month to over $100 billion per month within the last year, and recently surpassed the average transaction volume of payments on Visa’s platform (see Figure 6)!

Into The Unknown

Will stablecoins become a macro issue? Inevitably (see Did You Know? Digital Bank Run ). Just as the eurodollar market became central to the global financial crisis.

Did You Know?

Digital Bank Run

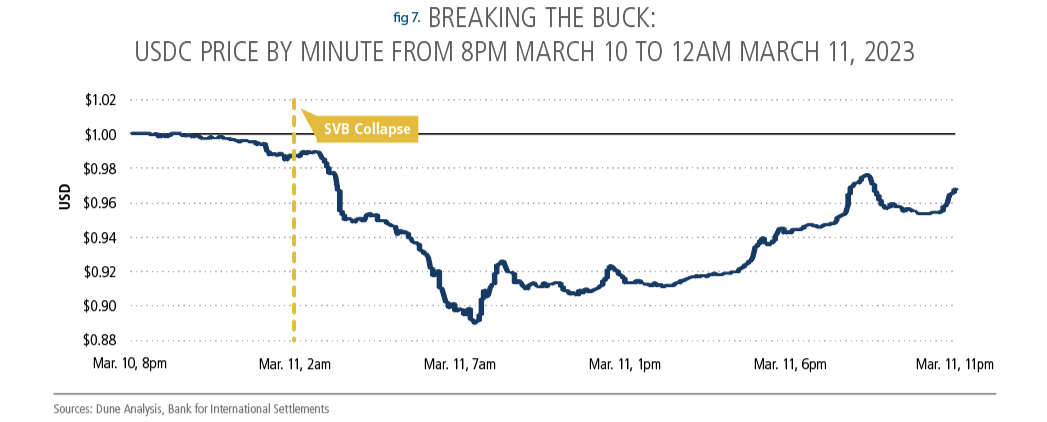

Central bankers may have been surprised that Silicon Valley Bank (SVB) held reserves for Circle, the creator of the US Dollar Coin (USDC). The day after SVB collapsed, the USDC traded down to 90 cents for every dollar, instead of the supposed 1-for-1 peg (see Figure 7). Why? Recall that Circle, the issuer of USDC, promised to back the USDC with the dollar. As the SVB’s collapse threatened dollar and Treasury deposits of Circle, crypto investors worried that Circle wouldn’t have enough dollars for them to redeem, leading to a fire sale of USDC, pushing down its price. However, investor panic eased after a week, and the USDC returned to trading at par ($1).

In the meantime, the rise of stablecoins will continue to popularize the U.S. dollar, the already popular and long-standing global currency leader.

As ever, the future is unknown. However, a brief tour of recent monetary history suggests we have seen this movie before. And, despite the efforts of various U.S. Presidents to shrug off the “burden” of the dollar system, eurodollars cemented the dollar's global status and sucked the rest of the world even more deeply into a positive feedback loop: using the dollar, borrowing in dollars, and settling trade in dollars, further entrenched the dollar.

A similar phenomenon is now underway with stablecoins—the vast majority of which are linked to USD—which could give the U.S. dollar system an unprecedented edge and opportunity in the 21st century.

Will policymakers embrace it? More importantly, will it even matter if they don’t?

Endnotes

President Nixon Address to the Nation Outlining a New Economic Policy: "The Challenge of Peace". (August 12, 2021). Richard Nixon Presidential Library. Youtube. https://www.youtube.com/watch?v=0BVj2gT6CgI

Massad T. G. (April 17, 2024). “Stablecoins and national security: Learning the lessons of Eurodollars.” Brookings Institute. https://www.brookings.edu/articles/stablecoins-and-national-security-learning-the-lessons-of eurodollars/#:~:text=satellites%20occasionally%20needed%20U,Eurobank%29%20that%20%E2%80%9CEurodollars%E2%80%9D%20are%20named

Schenk, C. R. (1998). The origins of the eurodollar market in London: 1955–1963. Explorations in Economic History, 35(2), 221–238. https://doi.org/10.1006/exeh.1998.0693

Federal Reserve Bank of New York. Research and Statistics Group. "November 1960, Vol. 42, No. 11," Economic Policy Review (Federal Reserve Bank of New York) (November 1960). https://fraser.stlouisfed.org/title/1170/item/2936

Paulina Restrepo-Echavarría and Praew Grittayaphong, "Bretton Woods and the Growth of the Eurodollar Market ," St. Louis Fed On the Economy, Jan. 20, 2022.

Gary Burn. “The Re-Emergence of Global Finance.” New York: Palgrave MacMillan, 2006. Jeffrey E. Garten. “Three Days at Camp David: How A Secret Meeting In 1971 Transformed The Global Economy.” New York: HarperCollins, 2021.

Money Market Stock Measures, H.6 Release. (April 22, 2025). Demand Deposits. Federal Reserve.

Burn 30.

Statistical release: BIS international banking statistics and global liquidity indicators at end-December 2023. (April 30, 2024). Bank for International Statistics (BIS).

Iñaki Aldasoro, Perry Mehrling, and Daniel H. Neilson, “Onchain is like offshore.”

Stablecoins fall into three categories: fiat-backed custodial stablecoins, collateralized stablecoins, and algorithmic stablecoins. Collateralized stablecoins are backed by other forms of crypto, such as DAI, which holds Bitcoin as collateral. Meanwhile, algorithmic stablecoins include projects like TerraUSD, which collapsed in 2022. See Written testimony of Jake Chervinsky, Chief Policy Officer of the Blockchain Association before the United States House of Representatives Committee on Financial Services Subcommittee on Digital Assets, Financial Technology and Inclusion, in a hearing entitled, “Understanding Stablecoins' Role in Payments and the Need for Legislation, 19 April 2023.”

Digital Money. (April 30, 2025). Treasury Borrowing Advisory Committee (TBAC). Presentation. https://home.treasury.gov/system/files/221/TBACCharge2Q22025.pdf

Duong, D. (2024, August 5). Stablecoins and the new payments landscape. Coinbase Institutional Trading Insights. https://www.coinbase.com/institutional/research-insights/research/market-intelligence/stablecoins-new-payments-landscape

Stripe 2024 annual letter. https://assets.stripeassets.com/fzn2n1nzq965/2pt3y

IHthraqR1KwXgr98U/b6301040587a62d5b6ef7b76c904032d/Stripe-annual-letter-2024.pdf

This material reflects the firm’s current opinion and is subject to change without notice. Sources for the material contained herein are deemed reliable but cannot be guaranteed. This material is for illustrative purposes only and does not constitute investment advice or an offer to sell or buy any security. Past performance is no guarantee of future results. Point of View articles may not be reprinted without permission. We welcome your comments and feedback at editor@payden.com.

This material has been approved by Payden & Rygel Global Limited which is authorised and regulated by the Financial Conduct Authority. This material has been approved by Payden Global SIM S.p.A.. which is authorised and regulated by CONSOB.