China's economy has been slowing. The $18 trillion economy is struggling to meet its growth targets and has been teetering on the brink of deflation for almost two years.

Today, most investors view the real estate sector slump as the cause of China’s slowdown. Yet, while property values are down, something else has been brewing beneath the surface of China’s housing market: local government financing vehicles (地方政府融资平台), or LGFVs for short.

Simply put, LGFVs are financial entities that local governments in China use to borrow money on their behalf. In broader terms, LGFVs are the main financing engines of the Chinese local governments, fueling the country’s real estate sector and economy since the turn of the century.

However, these financial engines are now sputtering.

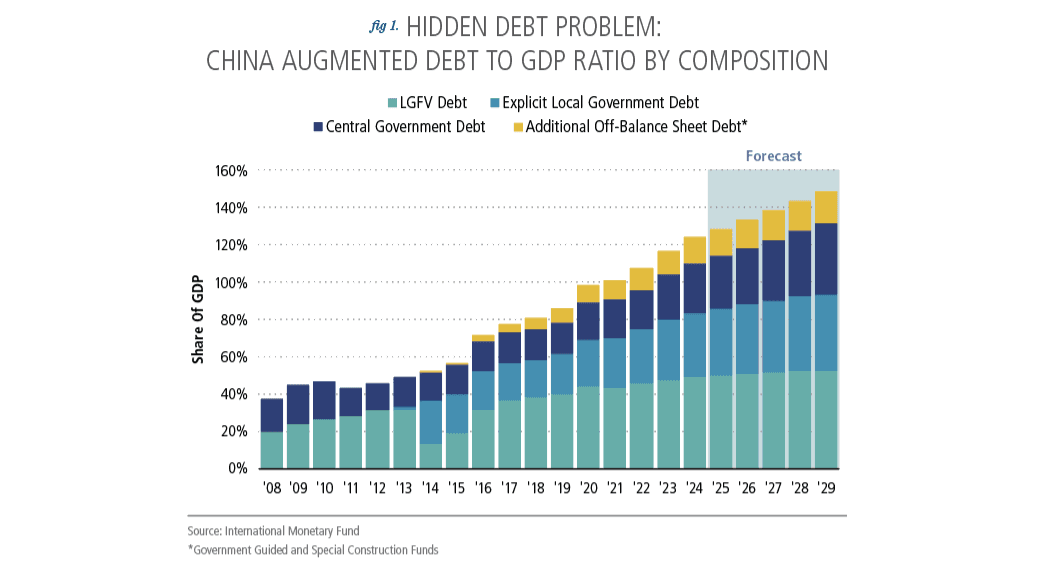

The debt numbers are staggeringly large. According to the International Monetary Fund (IMF), the LGFV debt load has ballooned from $1.2 trillion in 2014 to somewhere between $9 trillion and $14 trillion in 2024, or 50%-80% of GDP (see Figure 1).1

Below, we examine how LGFVs have contributed to the Chinese economy's boom (and bust) and consider possible outcomes for what could be the largest hidden debt crisis in history.

Let’s Rewind

LGFVs were born as a legal arbitrage to circumvent a 1994 Chinese law that banned local government borrowing rights.

However, local leaders encouraged land development to meet the ambitious growth targets set by the central government. By increasing land development, local governments sold more land use rights and stimulated economic growth.

Before real estate developers can build on land and sell finished properties to households, the raw land must be “readied” for development, which involves connecting it with roads, water, and electricity, among other things. Readying the land requires financial investment. To kickstart the land development process, in 1998, Wuhu City in Anhui Province created the first local government financing vehicle, the Wuhu Construction Investment Company (芜湖市建设投资有限公司).2

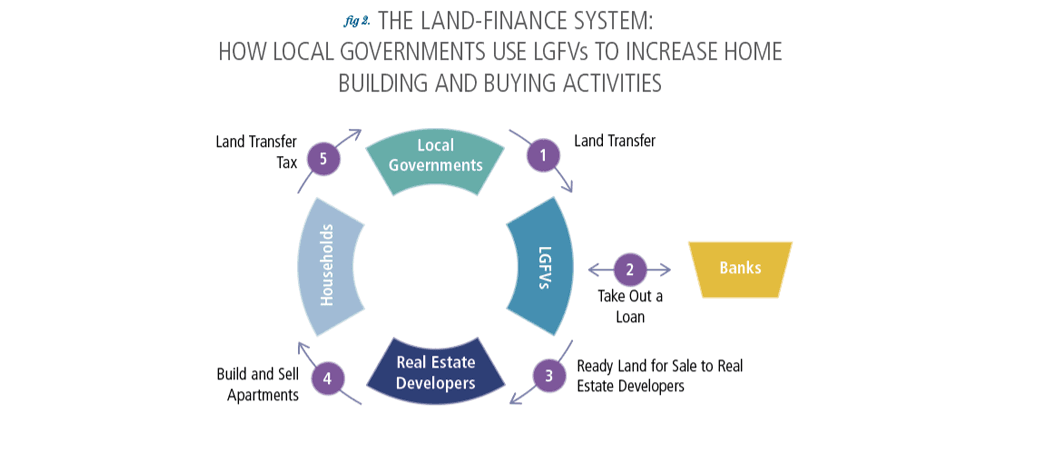

LGFVs quickly blossomed and became a key part of China's “land finance system” (土地财政). The model operates as follows: Local governments transfer land-use rights to LGFVs, who then approach banks to secure a loan for land development, using the rights as collateral (see Figure 2).

Next, the LGFVs use the borrowed capital to prepare the land for sale to real estate developers. Of the land sale proceeds, 30%-60% goes to the local government as a land transfer tax. The LGFVs use the rest to pay off their loan and interest from the bank (as we explore later, preparing the land for development generally costs more than the land can be sold for, leading to snowballing debt).

Effectively, LGFVs generated revenue while keeping local government balance sheets “debt-free.” In an ideal world, with high housing demand and rising property prices (as seen in China in the 2000s and the U.S. from 2003 to 2006), the financing model works, as developers pay substantial amounts for the prepared land. At its peak, land transfer revenue accounted for 30% of LGFVs’ total revenue. Consequently, as the primary financing source for public infrastructure, LGFVs pumped trillions of dollars into the Chinese economy.

A Qualified Success

LGFVs are open secrets to the central government. In fact, Chinese officials claim that LGFVs are “generally used for investment in infrastructure, so…[they] have positive externalities for the local economy.”3

Indeed, LGFVs have successfully built infrastructure and are key pillars of construction in China. LGFV spending in China is used for public investments, including constructing roads, high-speed rail, industrial parks, gas stations, skyscrapers, and other retail and shopping complexes.

As a result, China’s population has been urbanizing rapidly. In 2019, about 63% of the Chinese population lived in urban areas, up from under 30% at the turn of the century.

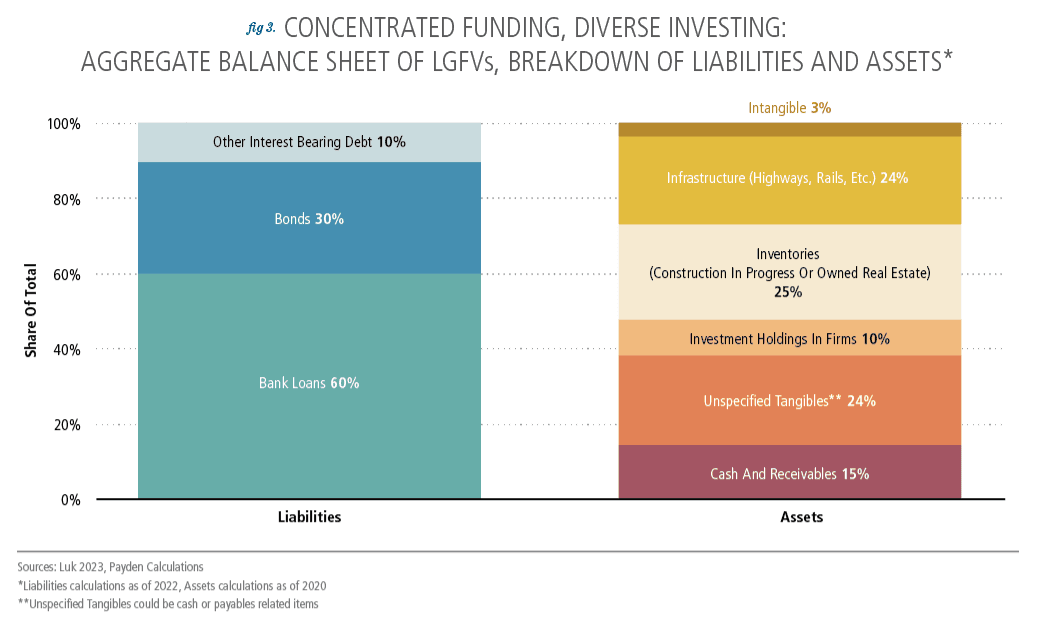

Moreover, since the global financial crisis (GFC), LGFVs have begun investing more actively in industrial sectors, transitioning into market-oriented state-owned enterprises. By 2022, less than half of LGFV spending has been used for capital expenditure in public investments like infrastructure, and a significant portion of LGFVs’ assets (investment holdings in firms, unspecified tangibles, and cash and receivables) are in non-real estate sectors such as manufacturing, technology, and retail, although a lot of those investments are not profitable (see Figure 3).4

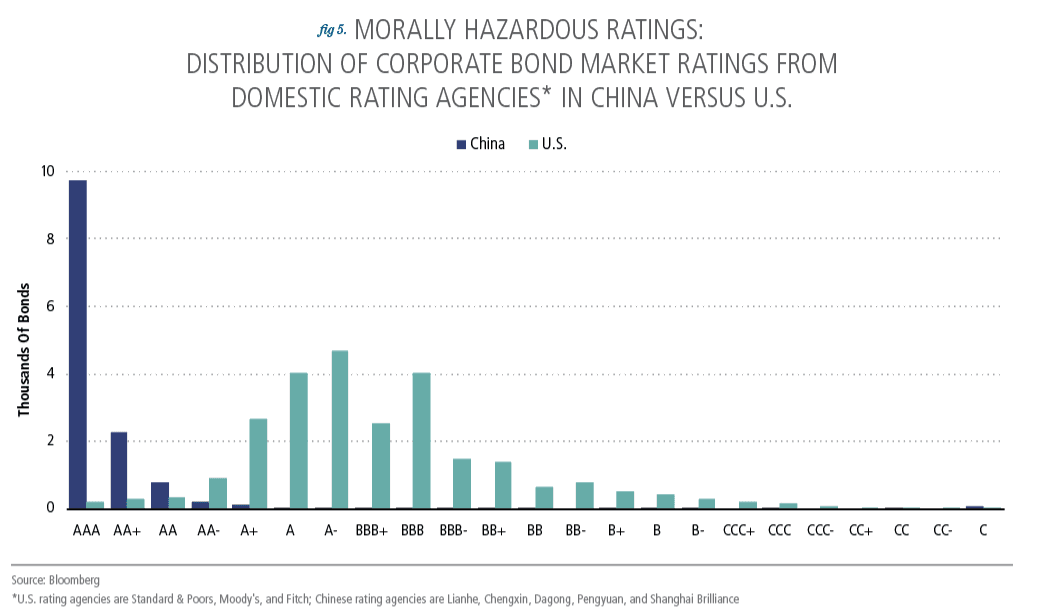

As LGFVs expanded their investment scope, their borrowing also broadened, shifting from taking loans from banks to directly issuing debt in the bond market (see Figure 3 again). The most recent available data (2022) shows that LGFV bond issuance accounted for roughly 40% of outstanding corporate bonds in China (see Did You Know? Moral Hazard).5

Chain Reaction

A common characteristic of a debt-fueled growth model is that it works until something breaks. The same linkages among LGFVs, commercial banks, the real estate sector, and capital markets that initially drove growth may now be working in reverse.

China’s property price growth stagnated in the mid-2010s. New home prices have declined by 10% since their peak in 2021, while existing home prices have declined by 16% in value. At the end of 2024, approximately 90 million housing units were left vacant nationwide. For comparison, there are only 147 million housing units in the entire United States (although the U.S. population is one-quarter the size).6

The decline in land sale prices and property demand has triggered a breakdown in LGFVs' financing cycle.

From 2017 to 2022, LGFVs struggled to finance their debt load. Income from operations and transfers from local governments were only sufficient to generate an average interest coverage ratio (income divided by required interest payments) of 105%. By 2022, the total income of LGFVs, including government transfers, reached $320 billion, while interest costs were approximately $400 billion.

What’s worse, many large real estate developers defaulted in 2020. To support the deteriorating housing market, LGFVs picked up the slack and purchased nearly half of the total land sold in 2022, compared to 17% in 2020.7 Subsequently, LGFVs incurred more debt to address the existing financial burden. Studies show that 80%-90% of LGFV spending is funded by infusions of new financing each year, primarily in the form of debt.8

Extend And Pretend

So, what has the Chinese government done to tackle the growing LGFV issue? In short, not enough.

Following a debt-fueled spending spree during the GFC, the central government restricted LGFV borrowings and mandated local governments to swap off-balance-sheet LGFV debt with on-balance-sheet bonds within a three-year period in 2015.

It turns out that the goal was too ambitious. Faced with a property market slowdown and a lack of other means of financing, the State Council issued a new decree in May 2015 (Document 40) urging financial institutions to continue lending to LGFVs to prop up economic growth.9

Since then, China has introduced multiple measures to tighten LGFV borrowing and bail out certain high-risk provinces, but has failed to halt the growth of LGFV debt. Finally, in September 2024, the government introduced a “three-way package” (“三箭齐发”), which includes an $800 billion central government debt swap, a $660 billion local government debt swap, and an extension of its 2028 deadline to repay $300 billion of LGFV debt.10 While the plan slowly swaps $1.7 trillion in hidden LGFV debt to on-balance-sheet debt, it accounts for only 20% of the known LGFV debt, ignoring the remaining 80%.11

Is There No Way Out? History Often Rhymes

Sovereign debt crises are not rare in world history. For example, during the 1830s, U.S. states borrowed aggressively to fund infrastructure construction, leading to a combined state debt of 12% of U.S. nominal GDP by 1841.12 Subsequently, nine out of the then 26 U.S. states defaulted, with four repudiating a substantial portion of their debt.

However, U.S. states restructured after the crisis through tax reforms, including increases in property taxes. Furthermore, the railroad boom in the 1850s allowed states to re-enter the bond market with increased demand and better credit protection systems.

In parallel with the U.S. state debt crisis, China's best-case scenario may be a technology-driven productivity boom, potentially even larger than the railroad boom in the U.S. during the 1850s. However, the ongoing trade war targeting China could thwart the country’s manufacturing and tech sectors, clouding the outlook for such a productivity boom.

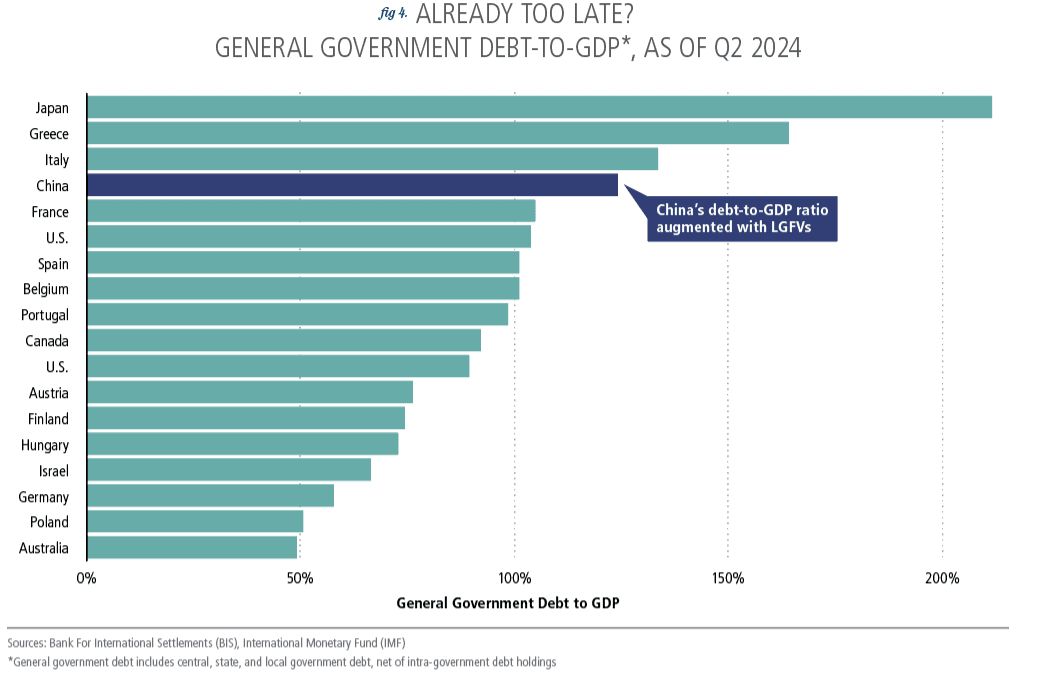

Can there be another way out? Recall that the Chinese central government still operates with a 25% official debt-to-GDP ratio. If the government warmed to more foreign ownership of government debt, China could leverage its ultra-low long-term government bond yield (1.6%) to swap LGFV debts onto its balance sheet. If total LGFV debt were added to the central government’s debt tally, Chinese debt-to-GDP would rise to an estimated 124%, above the debt ratio in the U.S. and many other major global economies, but not completely unmanageable, as it would still be lower than that of Italy (134%) and Japan (212%) (see Figure 4).13

Obviously, given the magnitude and complexity of China’s debt situation, a comprehensive solution, if any, will likely involve a combination of tax reform, reduced fiscal spending, and, most importantly, debt write-offs for banks and bondholders. Given that the state heavily controls China’s banking system, it may be possible for the government to prevent a widespread financial crisis.

No one has a crystal ball. However, if there is truly no way out, at least you are now familiar with a complex financial structure that has been driving an economy at the heart of the global financial system for decades.

Did You Know?

Moral Hazard

While the government may be unwilling to regulate LGFVs properly, we, as bond investors, have to wonder why anyone would lend trillions of dollars to companies with poor financials. Moral hazard, or perceived lack of risk due to high credit ratings, is the clear and resounding answer. Case in point: 73% of domestically rated Chinese corporate bonds (LGFVs’ classification) have a AAA rating. In the U.S., domestically rated corporates make up less than 1% of bonds receiving an AAA rating (see Figure 5).14 Further, Chinese firms are known to have dropped from AAA to default in the blink of an eye. If rating downgrades persist, it could lead to systemic collapse and put $18 trillion of outstanding debt at repricing risk.15 Interestingly, China’s current crisis resembles the subprime mortgage crisis in the U.S., which led to the worst recession in a century. It contains all the hallmarks: bad debt, a real estate bubble, and rampant moral hazard. Will we see a repeat of the worst financial crisis in world history?

Endnotes

Schneider, J. (2024, September 19). The Rise and Fall of LGFVs. Chinatalk.media; ChinaTalk. https://www.chinatalk.media/p/the-rise-and-fall-of-lgfvs

Ibid.

Zhang, Zheng Xin. (2024, July 19). Statement by the Executive Director of the IMF for The People’s Republic of China. People’s Republic of China: 2024 Article IV Consultation; IMF. https://www.imf.org/en/Publications/CR/Issues/2024/08/01/Peoples-Republic-of-China-2024-Article-IV-Consultation-Press-Release-Staff-Report-and-552803

International Monetary Fund. Asia and Pacific Department. (2022). People’s Republic of China: Selected Issues. IMF Staff Country Reports, 2022(022). https://www.elibrary.imf.org/view/journals/002/2022/022/article-A003-en.xml

Ibid.

Feng, R. (2024, October). China’s Housing Glut Collides With Its Shrinking Population. WSJ; The Wall Street Journal. https://www.wsj.com/world/china/china-housing-glut-population-economy-09cffa6a

Feng, A., & Wright, L. (2023, June 1). Tapped Out. Rhodium Group. https://rhg.com/research/tapped-out/

Ibid.

Ibid.

沙鹏程. (2024). 12万亿元地方化债“组合拳”怎么看旄当前中国经济问答__中国政府网. Www.gov.cn. https://www.gov.cn/yaowen/liebiao/202412/content_6991352.htm

Spegele, B., & Feng, R. (2024, July 14). Trillions in Hidden Debt Drove China’s Growth. Now It Threatens Its Future. WSJ; The Wall Street Journal. https://www.wsj.com/world/china/china-economy-debt-borrowing-33f08b5e?mod=article_inline

Grinath, A., Wallis, J. J., & Sylla, R. (1997). Debt, Default, and Revenue Structure: The American State Debt Crisis in the Early 1840s. RePEc: Research Papers in Economics. https://doi.org/10.3386/h0097. The total U.S. state debt was $193 million in 1841, whereas nominal GDP was $1,678 million. See Measuring Worth, U.S. GDP Dataset for nominal GDP data since the 1700s.

Ibid.

Chan, Andrew. 85% AAA-Rated Bonds Signal China Mispricing Risk. Bloomberg Intelligence; Bloomberg.

Ibid.

This material reflects the firm’s current opinion and is subject to change without notice. Sources for the material contained herein are deemed reliable but cannot be guaranteed. This material is for illustrative purposes only and does not constitute investment advice or an offer to sell or buy any security. Past performance is no guarantee of future results. Point of View articles may not be reprinted without permission. We welcome your comments and feedback at editor@payden.com.

This material has been approved by Payden & Rygel Global Limited which is authorised and regulated by the Financial Conduct Authority. This material has been approved by Payden Global SIM S.p.A.. which is authorised and regulated by CONSOB.