Productivity Puzzle

Week Ending: February 27, 2026

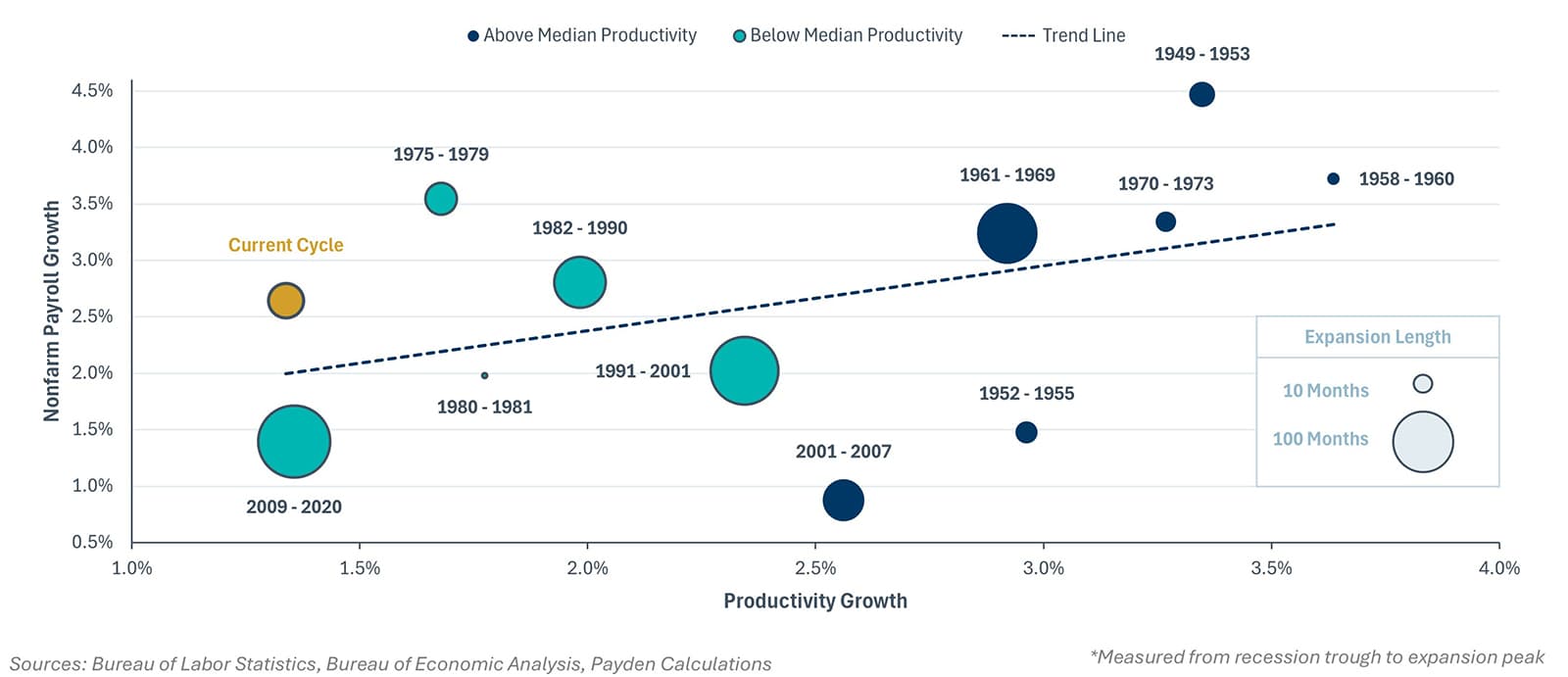

Productivity Puzzle

Average Annualized Growth Rate Of Employment And Productivity In Expansions*

Fear that AI will radically boost productivity and eliminate jobs circulated through markets again this week. Interestingly, though, rapid productivity growth has not (yet) plagued the economy in the current cycle. Historically, more rapid productivity growth has coincided with stronger job growth. For example, the 1950s and 1970s expansions saw both strong productivity gains and job growth. Meanwhile, in expansions with weaker investment and productivity, such as the 2010s, job growth was also relatively weak. Could AI upend the relationship, with never-tired, never-sick, always-working AI agents replacing workers? It's possible, but not our baseline. Perhaps, in the short run, AI can reduce the need for hiring for repetitive tasks. However, in the long run, history suggests that new technologies often create new industries and more jobs that need to be done. After all, 60% of today's jobs didn't exist before the 1940s, yet a much larger share of the prime-age (25-54) population has a job today (80%) than in the 1940s (63%)!

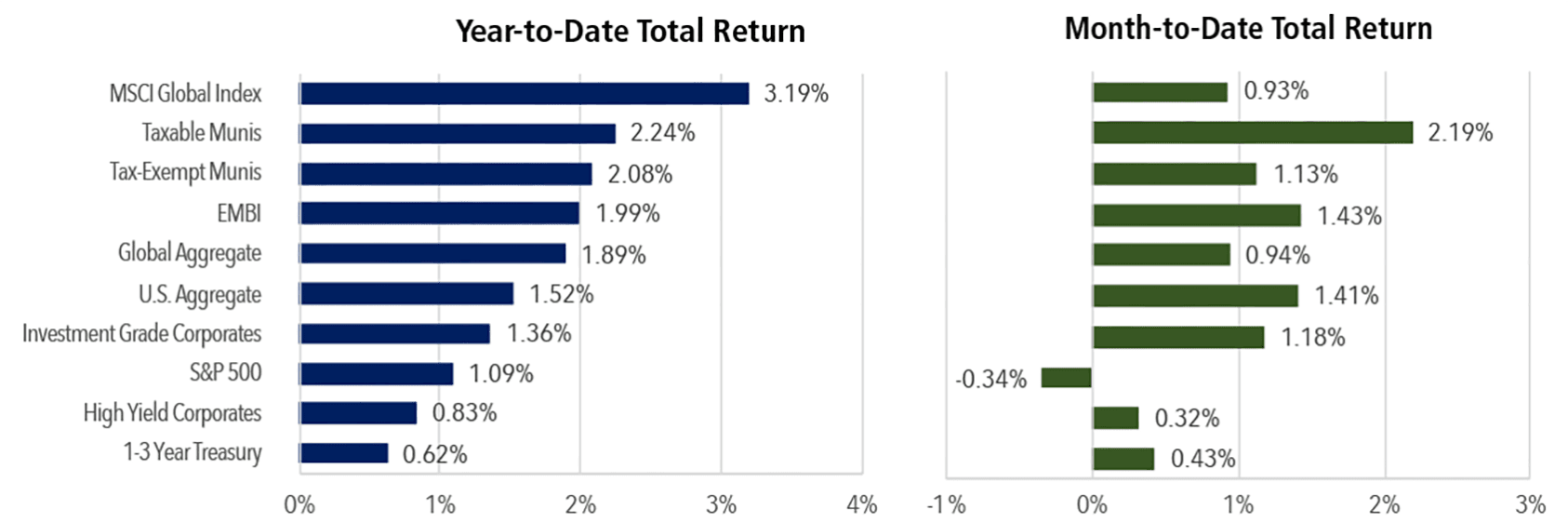

Total Returns by Asset Class

Highlights of the Week:

High Yield: Netflix surprised the market by withdrawing its bid for Warner Bros. Discovery (WBD), and Netflix's stock surged while WBD bonds declined. The market worries that Paramount, the winning bidder, will face greater challenges in managing WBD's large outstanding debt stack. Active managers need to carefully manage their positions in large and special situations, including issues like WBD.

Corporates: Investment grade (IG) corporate primary supply continues to come in strong, with February closing at $193 billion, bringing year-to-date totals to $411 billion, 19% higher than the same period last year. While Treasury rates are falling, IG corporate spreads are five basis points (bps) wider on the week at an option-adjusted spread of 82 bps.

Municipals: Municipal fund inflows are on track at the third-highest annual pace recorded so far this year. For the week ending Wednesday, LSEG Lipper reported another week of positive inflows, totaling about $1 billion, bringing the year-to-date total municipal bond fund inflows to $17.6 billion.

Equities: The U.S. equity market finished the week lower, pressured by uneven earnings results, ongoing uncertainty about AI-driven disruption, and persistent geopolitical tensions. Performance varied across sectors, with financials, technology, and consumer discretionary the weakest, while utilities, consumer staples, and healthcare performed best.

Securitized Products: Structured finance market professionals gathered this week for the annual SFVegas conference, focusing on asset-backed securities (ABS), residential mortgage-backed securities (RMBS), and collateralized loan obligations (CLOs). The RMBS market has maintained solid credit fundamentals and remains a bright spot for many investors. The ABS market has also been resilient, with some weakness in lower-income brackets being offset by higher underwriting standards. However, AI disruption concerns and declining valuations led to wider spreads in the CLO market. Commercial mortgage-backed securities (CMBS) also experienced stress from AI—issuance slowed to about one-third of its typical pace, with only two deals pricing, totaling $1.38 billion.