Back to School

Credit Quality and Investment Considerations for California K-12 Districts

Executive Summary

While credit quality among California K-12 school districts has moderated from pandemic-era highs, the Payden municipal bond team continues to view the sector favorably for investors focused on capital preservation and stable tax-free income. District balance sheets remain supported by strong reserve levels and ongoing state funding, though enrollment declines, rising labor costs, and post-pandemic normalization are beginning to pressure margins. From an investment perspective, California K-12 bonds continue to offer attractive risk-adjusted value given their essential-service nature, stable demand, and relative spread consistency.

Taken together, we believe the sector remains fundamentally resilient, though credit dispersion is likely to increase over time. We outline our views in two sections, beginning with the current credit climate followed by a discussion of investment considerations.

1. Credit Backdrop

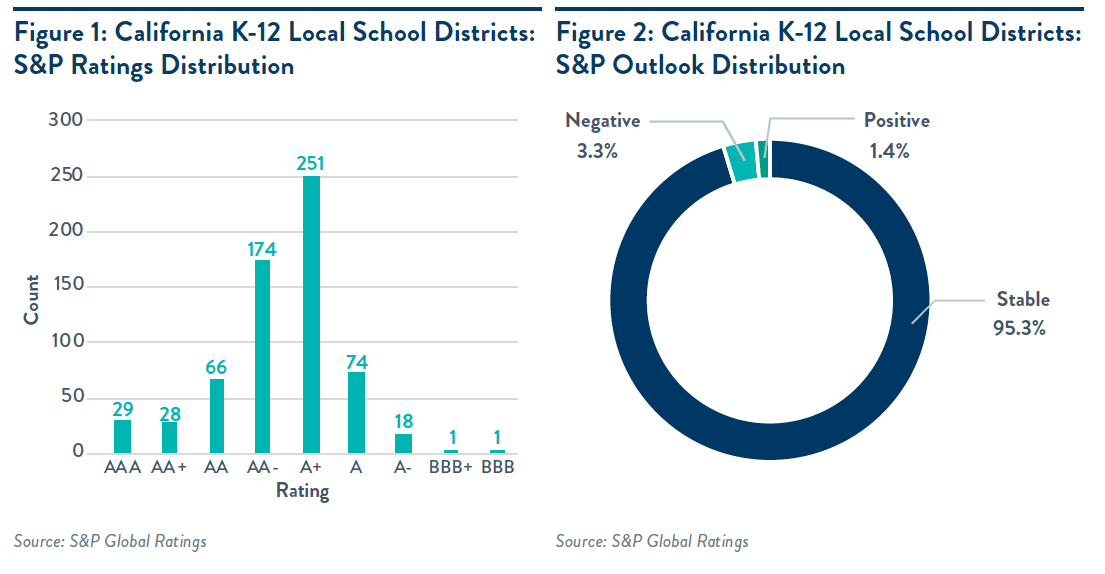

Ratings below A- are rare, with most California districts firmly in the A category or higher due to state oversight and balance sheet strength.

Elevated reserves provide a buffer, but expenditure growth has begun to outpace revenue growth, pressuring margins.

2. State Support

Strong legal protections support bondholders, including unlimited property tax levies for GO bonds and a first-lien claim on property tax revenues, ensuring first-priority debt service treatment.

State and county oversight allows intervention in distressed districts, reducing the risk of payment disruption.

3. Revenue Climate

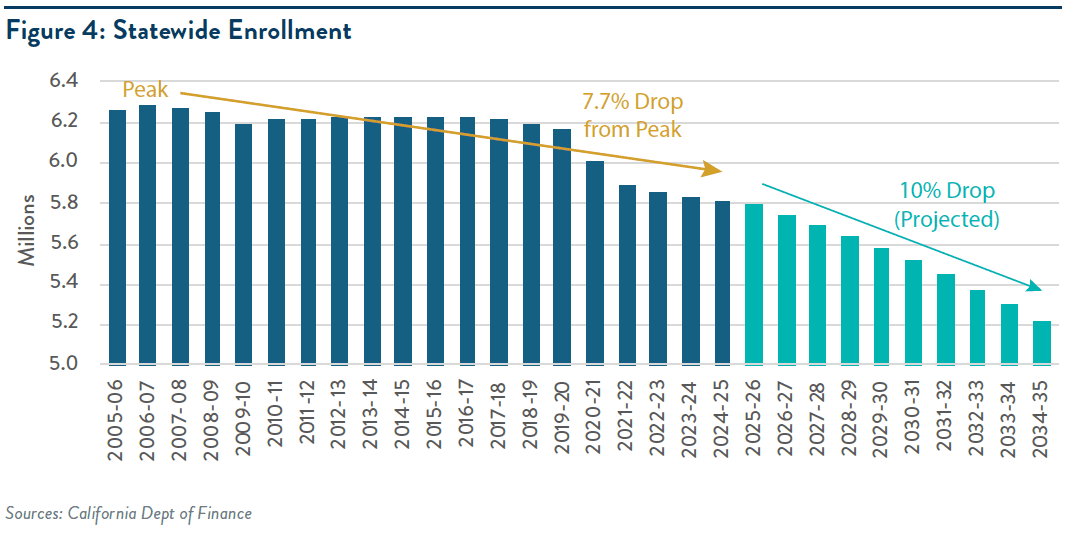

State aid, driven by enrollment, is softening due to demographic decline and school choice pressures, creating long-term revenue headwinds.

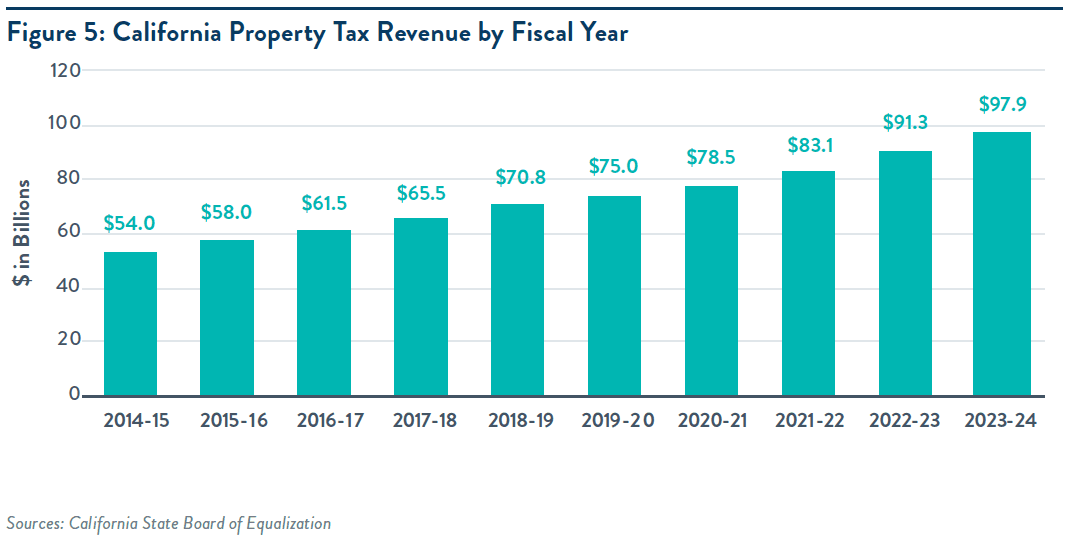

Property tax revenues remain robust and growing, partially offsetting enrollment-driven weakness despite Proposition 13 constraints.

4. Expenditure Growth

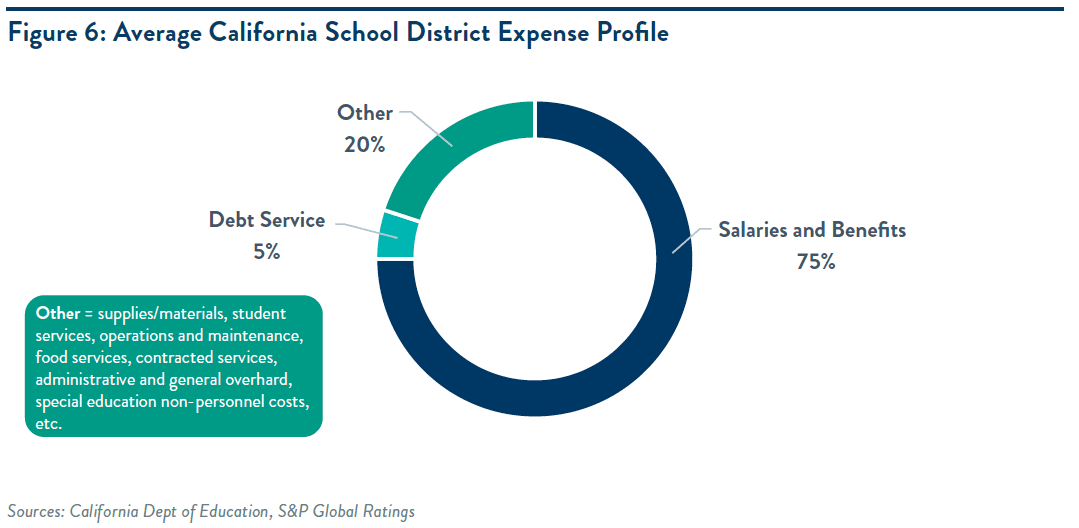

Salaries and benefits make up roughly 75% of spending and are rising due to inflation and collective bargaining agreements.

High fixed costs limit budget flexibility, increasing downside risk if revenues decline faster than reserves can absorb.

5. Investment Considerations

Pricing is driven more by technical factors, structure, and timing than by small credit differences across districts.

Pricing remains supported by strong in-state sponsorship, consistent reinvestment flows, and favorable callable structures that underpin market stability.

6. Bottom Line for Investors

Credit fundamentals remain sound but are gradually softening as enrollment and funding dynamics normalize post-pandemic.

Nevertheless, California K-12 bonds remain a core, defensive holding offering stable, tax-advantaged income commanding a quality premium consistent with their resilient fundamentals.

Credit backdrop:

Over the past decade, ratings at or below the A- level have been rare among California K-12 school districts and largely limited to isolated cases of acute fiscal stress, most notably Oakland Unified School District. The sector remains firmly anchored in the A category and above, reflecting strong state oversight and the essential-service nature of school district credits. While expenditure growth has outpaced revenue growth in recent years, we expect most districts to rely on balance sheet strength and active financial management to navigate a gradual moderation in credit quality. Many districts entered this period with historically elevated reserves, providing a buffer against near-term operating pressure.

State Support: California law provides strong statutory protections for school district bondholders, including a dedicated unlimited property tax levy for GO bonds and a robust state and county oversight framework that prioritizes timely debt service payment. As a result, we view state support for local school districts as very strong, even in the absence of a formal state aid intercept program, such as those in New York, Indiana, or Pennsylvania, or a permanent fund guarantee like in Texas.

We view Proposition 98 as reflective of strong state support; while it does not mandate a fixed percentage of General Fund spending, it establishes a constitutional minimum funding guarantee that has historically directed roughly 40% of State General Fund resources to K-14 education. This framework supports baseline funding continuity even as state revenues fluctuate with the economic cycle.

We view the priority of debt service as a state support strength. California law treats school district GO debt service as a first obligation, requiring a dedicated property tax levy sufficient to meet bond payments; failure to levy would constitute a legal violation, providing bondholders with strong payment security. California law provides school district GO bondholders with an effective first-priority claim on a dedicated ad valorem property tax levy, with taxes collected by the county and applied to debt service before remittance to districts; this statutory structure is a key factor underlying Fitch Ratings’ assignment of AAA ratings to many California school district GO bonds and represents a significant bondholder strength.

California’s fiscal oversight framework allows the state and county offices of education to intervene in financially challenged school districts, including assuming control over management and the budget process, as seen in cases such as Oakland USD; this proactive oversight is a credit strength that helps stabilize operations and prevent further credit deterioration. This oversight reduces the likelihood of sudden operational disruption and supports timely debt service payment even in periods of local fiscal stress.

However, while California’s GO bond structure provides strong bondholder protections, Proposition 13 limits annual growth in assessed property values to 2%, generally constraining property tax base growth. As a result, longer-term revenue expansion depends more on turnover, new development, and broader economic activity than on inflation alone.

Additionally, although California’s credit rating has remained stable over the past five years, emerging structural deficits may pressure the state’s fiscal flexibility and could limit future education funding capacity.

Revenue climate: While the revenue environment is softening due to pressures on government funding, property tax generation remains robust and continues to support district finances.

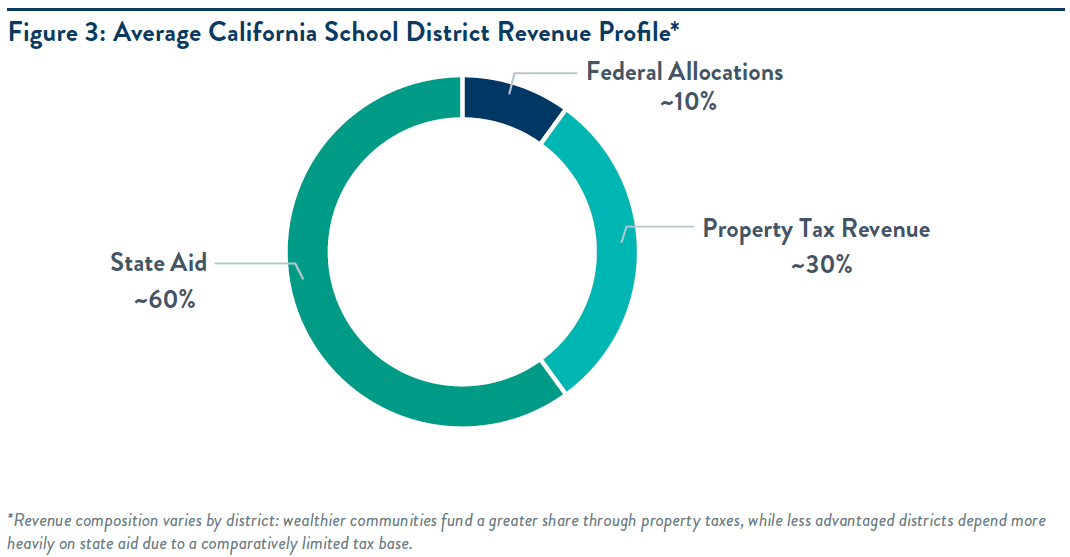

State aid represents the largest portion of California K-12 school district revenues, typically around 60%, and is primarily driven by average daily attendance (enrollment); ongoing enrollment declines tied to the state’s demographic cliff are the key driver of revenue softening and a credit concern we are closely monitoring, as they are likely to influence the sector’s future credit trajectory. These declines are largely attributable to persistently lower birth rates, declining fertility trends, and net out-migration in certain regions, which have reduced the school-age population statewide. In addition, increasing school choice competition from charter schools and private alternatives has further pressured district enrollment and attendance in certain regions, which can exacerbate declines in state aid and heighten long-term funding challenges for traditional public school systems. Districts experiencing sustained enrollment losses may face structurally weaker revenue growth, particularly if cost structures remain sticky. Unlike many other municipal issuers, California K-12 districts have minimal independent revenue-raising authority, as funding levels are largely determined by the state and local tax rates are constitutionally constrained, further limiting fiscal flexibility.

Federal funding is generally not a material credit concern given its small but stable contribution to district revenues. It typically represents less than 10% of total revenues for California K-12 school districts and is largely statutorily restricted, with funds primarily dedicated to Title I programs, special education, and ADA-related compliance. Importantly, Title I funding is established in federal statute and historically has remained durable across administrations, providing a measure of stability even amid policy proposals to reduce education spending or reorganize the Department of Education. By contrast, pandemic-era ESSER allocations were explicitly temporary federal transfers that have now expired; districts that used those one-time funds to support ongoing expenditures may face budgetary pressure as the associated revenues roll off while costs remain embedded in their operating structures.

Property tax generation remains robust across California, with statewide property tax revenues increasing approximately 29% from $70.8 billion in FY 2019 to $91.3 billion in FY 2023, followed by an additional ~7% increase to $97.9 billion in FY 2024. This consistent property tax performance helps offset softness in state aid driven by enrollment declines, although Proposition 13 constrains longer-term growth potential by limiting annual assessed value increases absent property turnover or new development. This dynamic increases the importance of local tax base trends, particularly in high-growth or high turnover regions when evaluating credit stability.

Expenditure growth: Expenditure pressures are increasing across California K-12 school districts as elevated inflation and recently negotiated collective bargaining agreements continue to drive higher operating costs. Salary increases, rising benefit expenses, and mandated cost growth have outpaced revenue gains in recent years, reducing budgetary flexibility and pressuring operating margins. As personnel costs represent the largest share of district expenditures, management’s ability to control spending and utilize reserves will be a key determinant of future credit trajectories. In our view, the main near- to medium-term credit question is whether revenue softening outpaces districts’ ability to slow expenditure growth. Recent labor disruptions, including the strike at San Francisco Unified School District, reflect broader financial strain across California public schools, as enrollment declines and elevated staffing and healthcare costs pressure district budgets and intensify collective bargaining tensions statewide.

Salaries and benefits, which typically comprise roughly 75% of total expenditures, are largely determined through collective bargaining agreements in California and are sometimes negotiated without full consideration of the prevailing revenue environment or longer-term affordability. At the same time, once agreements are in place, these costs are generally fixed and predictable, providing budget directors with clear visibility into the majority of expenditure obligations until the next round of collective bargaining negotiations.

Fixed costs are generally higher in California than in most other states and can comprise up to 20% of total expenditures, reflecting elevated retirement and other long-term obligations. Because retirement costs are largely captured within salaries and benefits, which account for roughly 75% of spending, and debt service typically represents an additional ~5%, approximately 80% of a typical district’s expenditures are effectively fixed. As a result, amid inflationary pressures and collectively bargained wage increases, budget directors have limited flexibility to meaningfully reduce costs on the expenditure side of the ledger. This limited flexibility can create asymmetric downside risk if enrollment-driven revenues decline faster than reserves can absorb.

Investment Considerations:

For California investors, K-12 school district bonds are often driven more by technical, structural, and relative-value dynamics than by incremental credit differentiation. Tax-driven in-state demand, combined with supply patterns, reinvestment flows, and seasonal technicals, frequently compress spreads and support firm pricing for high-grade school GOs relative to broader benchmarks, making entry levels and timing important. Pricing is also heavily influenced by bond structure and optionality, as coupon and call features meaningfully affect yield profiles and total return outcomes. Investors can add value through curve positioning, callable structure selection, and cross-sector relative-value trades versus other California sectors (cities, counties, community colleges), while K-12 exposure can also provide portfolio diversification by introducing revenue and tax-base drivers that differ from general government or utility credits. In practice, technical conditions and structure often matter more than small differences in underlying ratings.

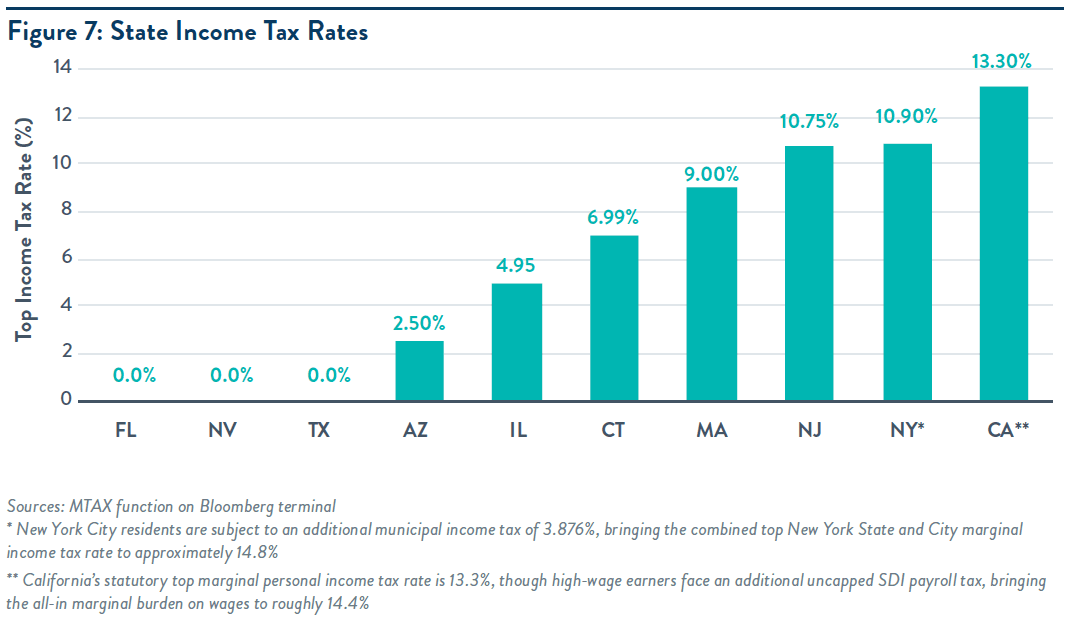

Demand for California K-12 school district bonds is heavily driven by the state’s high income tax environment, as the double tax exemption materially enhances tax-equivalent yields for in-state investors. This persistent tax-driven demand contributes to price stability and sustained valuations, even when nominal yields appear modest.

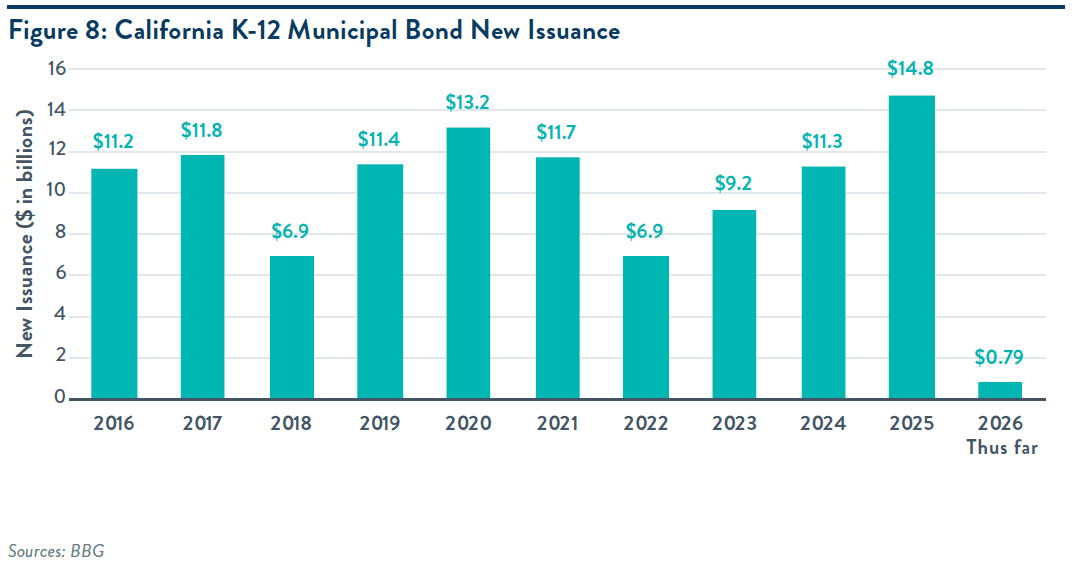

Supply technicals are influential in the California school district market, as elevated redemption and reinvestment flows combined with steady new issuance have supported spread compression; while supply has remained active, strong in-state demand has generally absorbed issuance efficiently, limiting spread widening. Shifts in net supply, refunding activity, and sector-specific issuance trends can nonetheless meaningfully move yields and relative value.

Seasonal technicals, particularly the “January effect,” have been sustained into February this year, as elevated coupon and maturity reinvestment flows and strong in-state demand for California tax-exempt paper have continued to generate outsized buying pressure in the school district sector. This reinvestment-driven seasonality has helped absorb steady issuance, compress spreads, and push yields lower, often resulting in firm pricing and sustained premium valuations for California K-12 bonds relative to broader benchmarks, making entry points and timing especially important in the early-year period.

Bond structure and optionality are key pricing determinants in the California K-12 market, as school district issuance is frequently concentrated in premium-coupon, callable GO structures where yield-to-call dynamics, call protection, and extension risk can meaningfully influence valuations and total return. As a result, bonds with stronger call profiles or more investor-favorable structures often trade at tighter spreads, while optionality can introduce relative-value dispersion even among similarly rated credits.

Bottom Line for Investors

For California investors, K-12 school district bonds sit in a market where credit fundamentals remain sound but are gradually softening from the elevated levels seen during the pandemic period, as enrollment pressures and funding dynamics continue to evolve. While we expect this measured credit weakening to persist over time, state oversight, statutory funding formulas, and strong bondholder protections provide important mitigants that help preserve overall credit stability. Against this backdrop, pricing is driven largely by technical and structural forces, including strong tax-driven in-state demand, favorable seasonal reinvestment dynamics, readily absorbed supply, and callable bond optionality, which have contributed to sustained spread compression and tight differentials for high-grade California school district GOs relative to broader benchmarks.

Although investors can find materially wider spreads in other Californina sectors—such as affordable housing or prepaid energy bonds, we view California K-12 school districts as a core portfolio diversifier, offering stable tax-backed income, defensive characteristics, and reliable cash flows. In this context, school district bonds remain an effective tool for clipping steady, tax-advantaged income, preserving capital, and complementing higher-spread exposures, even as valuations remain well-supported and credit trends modestly downward. For high-quality California portfolios, we continue to view the sector as a durable source of essential-service income supported by strong structural protections.

This material reflects the firm’s current opinion and is subject to change without notice. Sources for the material contained herein are deemed reliable but cannot be guaranteed. This material is for illustrative purposes only and does not constitute investment advice or an offer to sell or buy any security. Past performance is no guarantee of future results. Point of View articles may not be reprinted without permission. We welcome your comments and feedback at editor@payden.com.

This material has been approved by Payden & Rygel Global Limited which is authorised and regulated by the Financial Conduct Authority. This material has been approved by Payden Global SIM S.p.A.. which is authorised and regulated by CONSOB.