Will The Golden State Go Bankrupt?

Assessing Stability in the World’s 4th-Largest Economy

Executive Summary

Recent concerns over California’s fiscal health—driven by declining IPO volume, reduced federal funding risk, and rising costs—have prompted questions about the state’s financial stability. After a thorough analysis, we believe the risk of a bond default or severe credit deterioration remains low. Key takeaways below:

1. Bankruptcy vs. Default

States cannot legally file for bankruptcy under the 10th Amendment.

While defaults are technically possible, California is nowhere near default based on current indicators.

2. Revenue Trends & IPO Activity

IPO activity is not a core revenue driver and its recent decline reflects a normalization post-COVID stimulus, not a structural weakness.

Tax collections remain healthy, with current fiscal year trends pointing toward a relatively small $12 billion deficit spread over the next two fiscal years.

3. Credit Ratings Stability

All three major credit agencies S&P, Moody’s, and Fitch—rate California AA-/Aa2/AA, respectively, all with stable outlooks.

Ratings were recently reviewed and reaffirmed, reflecting confidence in the State’s near-term fiscal footing, but we anticipate their reaction to the May Budget Revision shortly.

4. Economic Strength & Reserves

California’s GDP ranks #4 globally, surpassing Japan, with a broad and resilient tax base.

Although reserves have dipped since 2023 due to pandemic fund drawdowns and delayed tax receipts, they remain at comparatively strong levels historically.

5. Manageable Liabilities

Debt service is low (3–4% of govermental expenditures), and pension funding is solid (near the 70–80% comfort threshold).

Constitutional protections prioritize education and debt payments, meaning revenue would need to drop over 50% to threaten debt service.

6. Credit Conditions Remain Steady, with Caveats

Despite uncertainty, California retains strong credit fundamentals with stable ratings, manageable deficits, and conservative budgeting that supports bondholder confidence.

A recent client inquiry raised concerns about the potential for California to face insolvency, driven by declining IPO activity, the risk of reduced federal support, and rising costs for goods and wages. In light of these concerns, we believe a clear and measured perspective is essential.

While recent headlines surrounding tariffs, fiscal tightening, and economic uncertainty have contributed to heightened market anxiety, our base case remains firm: Although California’s credit profile is softening slightly, it continues to demonstrate resilience, supported by a vast and diversified tax base, substantial reserve levels, and long-term liabilities that we consider both moderate and manageable.

Furthermore, monthly tax collection data remains healthy as we enter the final month of the current fiscal year. The following analysis provides a comprehensive overview of the key fiscal indicators and structural protections underpinning the State’s continued credit strength. Let’s explore the data more closely:

1. First, to clarify semantics, the 10th amendment prohibits states from declaring bankruptcy because the Constitution considers them to be “sovereign entities.”

Of course, cities like Detroit have filed for bankruptcy but even for a Commonwealth like Puerto Rico, the Obama administration had to coordinate with Congress to establish a creative work-around so that the Island could restructure its debt. Nevertheless, although states may not file for bankruptcy, they can still default on their debt, as Arkansas last did in 1933. Now that the semantics are out of the way, we will address how close (or far) we believe the State of California is to default, which we believe was central to the spirit of our client’s question.

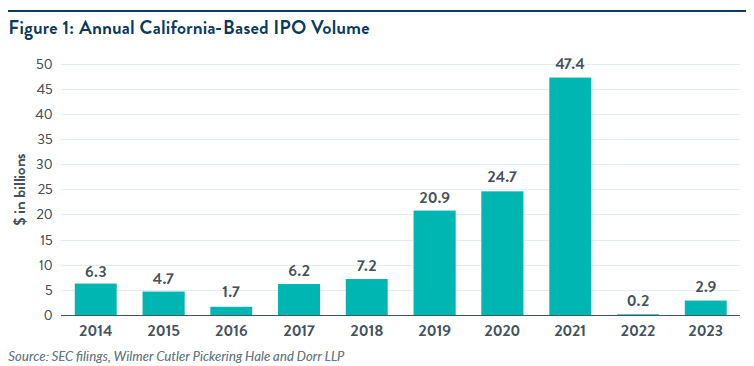

2. Second, we highlight that although IPO volume has declined materially, we are not overly concerned as IPO revenues have not traditionally been a revenue driver for the State.

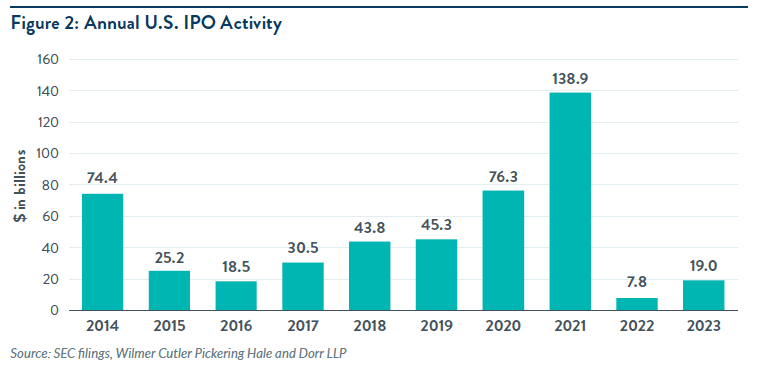

As you can see below (in Figure 1), from fiscals 2014-2018, IPO volume was rather immaterial before experiencing some solid growth over 2019-2021. That said, we view 2019 IPO growth as organic while assigning strong IPO growth in 2020 and 2021 to exceptional liquidity transferred from the federal government to state and local governments, corporations, individuals, etc., that drove an extraordinary surge in business activity. We view the drop in IPO activity in 2022 as a correction to the surge over the preceding few years. Therefore, we view IPO growth over 2019-2021 as more of an exception to the rule. As shown in Figure 2, California’s IPO activity largely coincides with national trends. As such, we don’t view the drop in IPO activity as a major credit concern as most recent IPO activity is merely a reflection of the normalization of historical trends nationwide.

3. No indications currently suggest a risk of bankruptcy or default, a view shared by all three major credit rating agencies, which have affirmed the State’s ratings at AA-/Aa2/AA, each with a stable outlook. These ratings have been reviewed within the past two months and remain current. Importantly, had federal policy uncertainty been deemed a material credit risk, it is likely the agencies would have revised their outlooks to negative or placed the ratings on CreditWatch. Instead, all three have maintained stable outlooks (good news!), signaling continued confidence in the State’s credit strength. Nevertheless we’re watching for potential reactions to the recent May Budget Revision, but expect a low probability of a one notch downgrade in a worst case scenario.

4. Despite comparatively high levels of income inequality, poverty and unemployment, the State economy still provides an exceptional tax base for revenue generation. In fact, Governor Newsom recently announced the State economy surpassed Japan’s economy as the 4th largest in the world with Germany just slightly ahead (but India is right on California’s heels!).

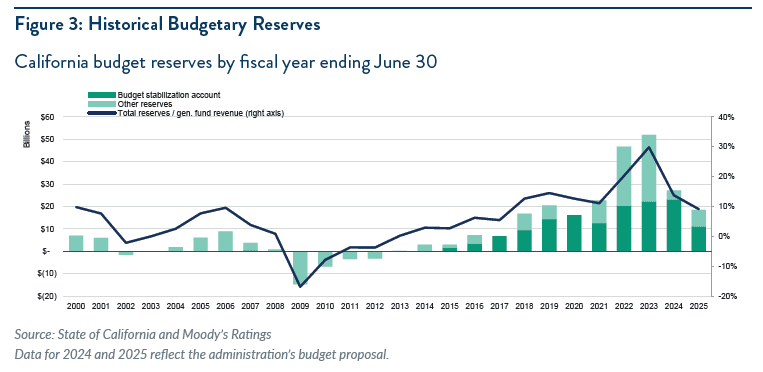

The State’s finances are still relatively strong despite the recent volatility. Figure 3 tracks budget reserves historically, underscoring that in 2024 and 2025 the Golden State still enjoyed some of the highest reserves in its recent history. We note, however, that reserves have fallen since 2023, due mostly to spending down COVID funds and to an imbalance breached in 2023 due a tax filing extension from April to October, during which time State leadership realized too late that tax revenues had fallen more than it was expecting. Since then, although budgetary performance has improved materially, a small structural imbalance has persisted due to what Governor Newsom labels the “Trump Slump”. Up until “Liberation Day”, the budgetary picture was looking rosy for FY 25 and revenue trends were indicating at least balanced operations to close the fiscal year. However, the aftermath of “Liberation Day” heavily disrupted markets and injected a shot of uncertainty into the State’s budgeting framework. In fact, when Governor Newsom was revising next year’s proposed budget, he was doing so at the heights of this volatility, during which time he and his team concluded that uncertainty surrounding tariffs and federal policy would correct revenue projections downward by $16 billion, thereby erasing the small surplus projected for this year. The good news, however, is that although we are still operating under a degree of uncertainty, the investment climate has improved since then, making Newsom’s estimates more conservative in nature as they were made in preparation for a much worse economic scenario. In his recently announced May Budget Revision, Newsom announced his $322 spending bill for the next fiscal year with a $12 billion gap projected for the next two fiscal years, which is expected to reduce total reserves from $18.2 billion to $11.2 billion at FYE 2026. To address the gap, the Governor is proposing reducing universal healthcare benefits for undocumented Californians as well as making cuts to some non-recurring spending initiatives. The California State Legislature will likely debate then pass the budget (with modifications) by June 15 at which time we expect the ratings agencies to begin opining on the future trajectory of the State’s credit rating.

Our base case is Newsom’s revision likely incorporates conservative budget estimates and that the credit rating will likely remain stable in the near term with a moderately low to moderate probability of a negative outlook revision while the ratings agencies monitor how budgetary performance unfolds. Additionally, although we view the likelihood of a one notch downgrade to be low, we can’t rule out that possibility altogether but we do not expect any credit deterioration beyond a one-notch downgrade. We also note that Governor Newsom may be preparing a run for president in 2028 so we are expecting him to pull out all the stops to ensure the State’s finances/reserves are as robust as possible to mollify critics in the less liberal swing states.

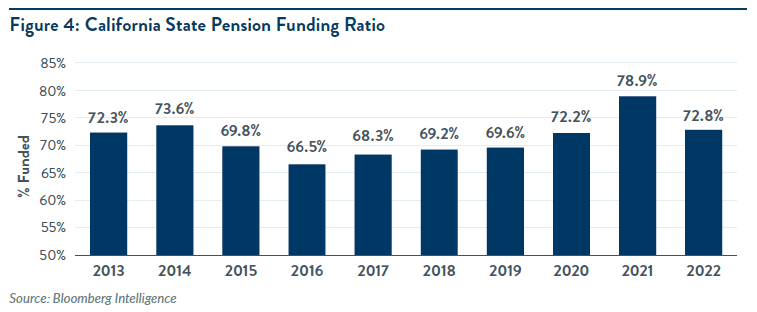

5. Lastly, we view the State’s long term liabilities to be moderate/manageable. The debt burden is moderate on a per capita basis and debt service only comprises 3%-4% of total governmental expenditures, which is low. Additionally, as you can see in Figure 4 from Bloomberg Intelligence, pension funding is very good (and it’s right in the sweet spot you want to be in around 70–80%). *Please note there is a 1-2 year lag in pension reporting so the strong performance recorded in 2024 and volatile performance this year are not reflected in Figure 4.

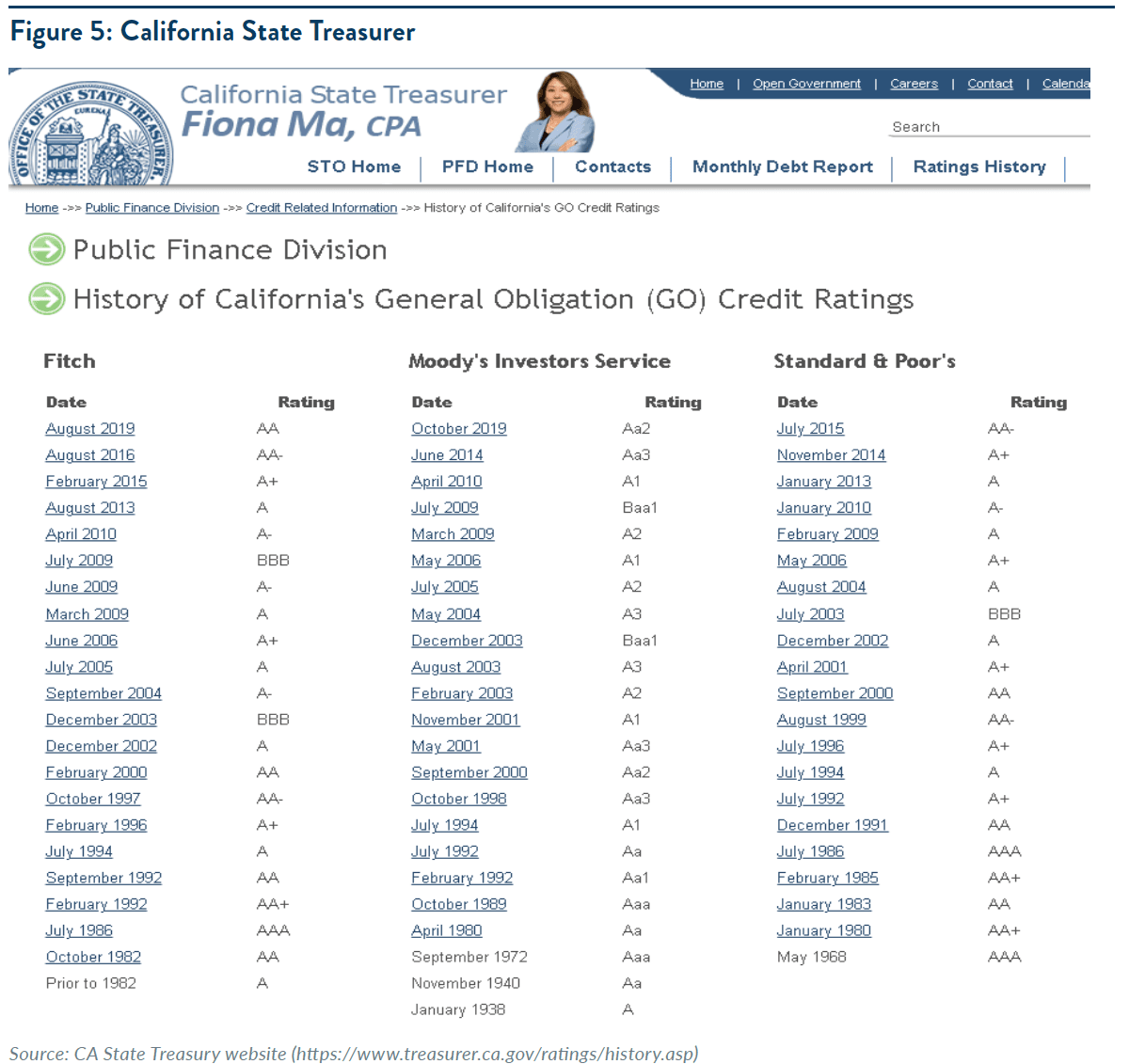

The probability of default is also reduced by the sheer nature of bondholder protections in the State. There is a “pecking order” with regards to which expenditures are guaranteed and prioritized with bondholder payments guaranteed only after all education spending obligations have been met. At the top of the pecking order is education spending and as per Prop 98, at least 40% of all general fund spending must be allocated to education, so should total revenue drop precipitously, education spending would be prioritized over all other items that comprise the remaining 60% of the budget. Next in the pecking order is debt service, which comprises about 5% of general fund spending. That said, education and debt service, which together comprise about 45% of the budget, are guaranteed and prioritized by the State Constitution before all other spending items. That means revenue would have to drop over 50% for us to to consider a default picture, meaning the economic climate would have to be cataclysmic for the State to get to a point where it would not be able to meet its debt obligations. Of course, we could see drops in revenue that could reduce reserves, which could make spreads widen or catalyze a one notch credit downgrade but we would expect ensuing downward rating movement to be limited. As you can see in Figure 5, even during the Great Recession, when the State was materially less prepared for a downturn than it is now (thanks largely to Governor Brown who spearheaded several initiatives to strengthen credit quality, such as Prop 2), the State’s rating never fell below investment grade and didn’t get notched down more than 2-3 levels, remaining fully investment grade. Although there is some current uneasiness and uncertainty, economic data still looks like it’s holding up reasonably well as are tax collections, which came in underbudget for April but are still strong on a historical basis. Also, over the last few weeks, although not guaranteed, it looks like the administration is willing to back down and reverse course if market volatility punishes it for policy turns the market doesn’t like (i.e. threatening to fire Fed Chair Powell, being too hard on China, etc).

6. In conclusion, while a degree of market unpredictability persists, recent signals suggest relative credit stability with slight credit softening indicate at worst a one notch downgrade. All three major credit rating agencies have maintained high investment-grade ratings for the State, each with a stable outlook and California’s expansive economy is expected to continue generating sufficient revenue, with only a modest deficit likely in a worst-case scenario for the current fiscal year. Additionally, long-term liabilities are not anticipated to exert meaningful credit pressure. Given the constitutional prioritization of debt repayment, a revenue decline exceeding 50 percent would be required to pose a credible threat of bond default. Fiscal performance and federal policy developments remain key areas of observation. Governor Newsom’s “May Revision” to the upcoming fiscal year’s budget reflects a softening budget picture in an uncertain climate but his conservative estimates addressing potential revenue shortfalls likely bode well for credit stability.

This material reflects the firm’s current opinion and is subject to change without notice. Sources for the material contained herein are deemed reliable but cannot be guaranteed. This material is for illustrative purposes only and does not constitute investment advice or an offer to sell or buy any security. Past performance is no guarantee of future results. Point of View articles may not be reprinted without permission. We welcome your comments and feedback at editor@payden.com.

This material has been approved by Payden & Rygel Global Limited which is authorised and regulated by the Financial Conduct Authority. This material has been approved by Payden Global SIM S.p.A.. which is authorised and regulated by CONSOB.