Transit Trouble

Week Ending: March 06, 2026

Transit Trouble

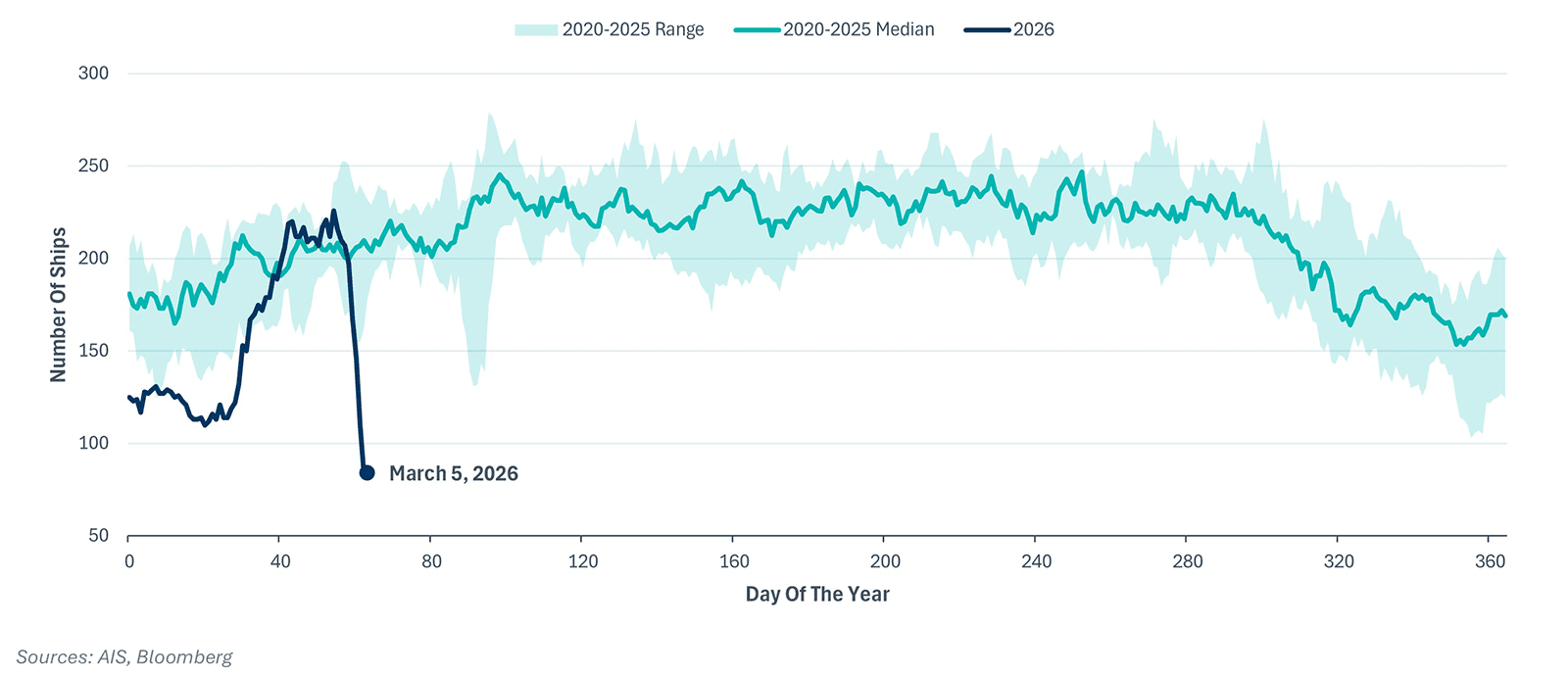

Daily Transits Of Tankers And Gas Carriers Through The Stra

For financial markets, the most pressing issue arising from events in the Middle East is the flow (or disruption) of energy through the narrow Straitof Hormuz. In the week before hostilities erupted, roughly 735 commercial vessels, including 210 tankers and gas carriers, transited the Strait.In the five days since the war began, ship traffic slowed to its lowest since 2020. Over 150 tankers are waiting outside the Strait, a container shiphas already been hit, and two others have turned around. It’s little surprise that the price of Brent oil has spiked 17% as of Thursday’s close, andEuropean benchmark gas futures surged 59% after attacks on Qatari LNG facilities forced a production suspension. The ultimate macro impact willdepend on the duration of the disruption. Days or weeks versus months and quarters? Our main view is that the longer the energy supply flow isrestricted, the bigger the risk to global economic growth, rather than inflation. In particular, Asia and Europe would be more exposed than theU.S., which receives only about 2% of energy shipments through the Strait.

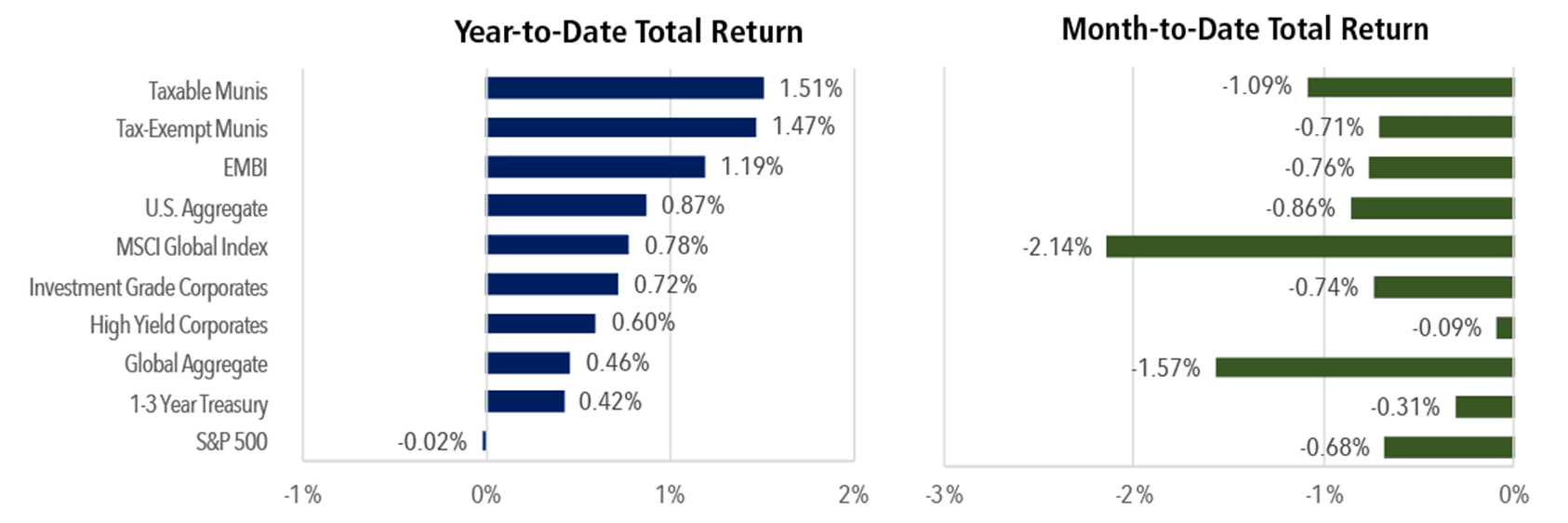

Total Returns by Asset Class

Highlights of the Week:

High Yield: High yield has traditionally safeguarded capital during risk market sell-offs, and this week was no different. The S&P 500 dropped0.64% through Thursday’s close, while the high yield market declined just 0.04%. High yield remains an important part of a diversifiedportfolio.

Corporates: Issuers are looking for signs of improving market sentiment to re-enter the new issue market. Only one deal was priced onMonday and Tuesday, before more than $50 billion came to market across 25 issuers over the next two days. Due to the volatility, dealperformance has been mixed, but spreads on newly issued bonds have tightened on the margin in the secondary market.