SaaS Stumple

Week Ending: February 6, 2026

SaaS Stumble

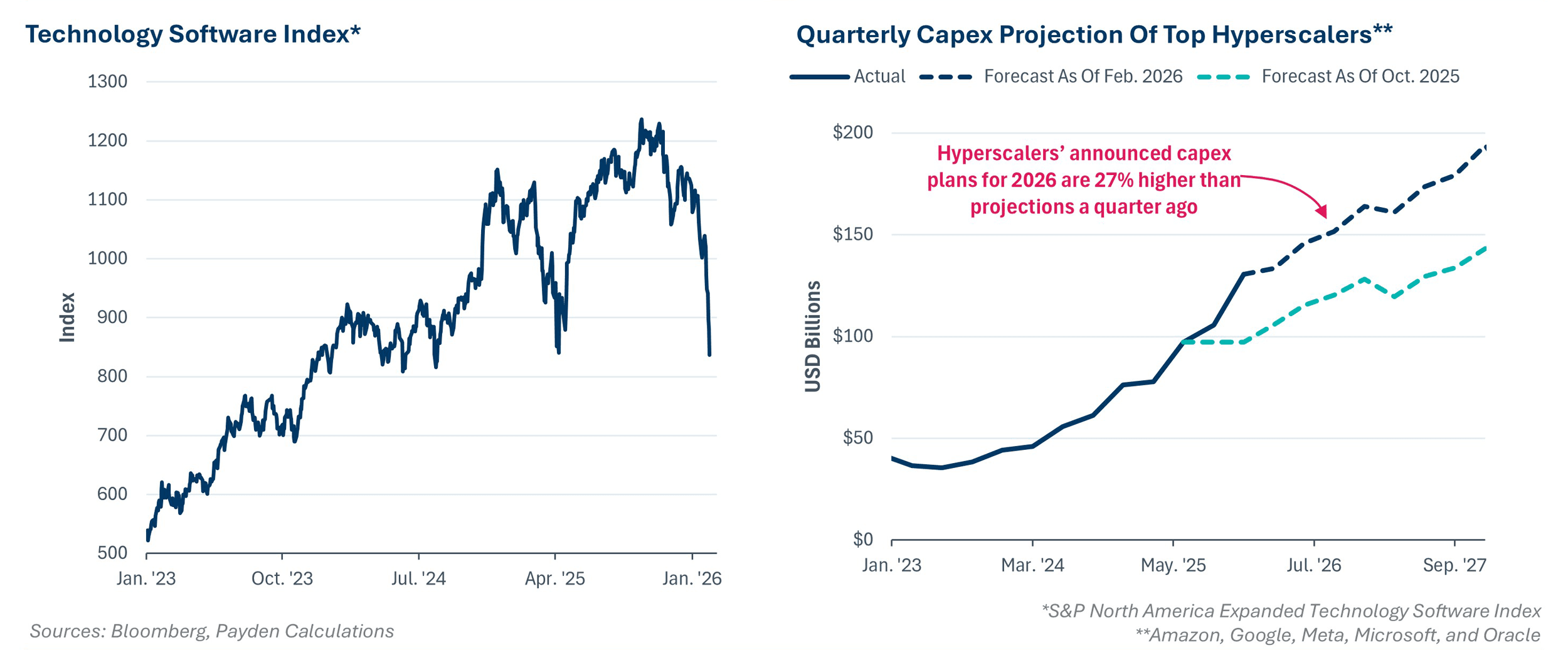

Technology Software Index*

This week, software technology stocks saw a 12% drawdown as of Thursday, even as major hyperscalers announced stellar revenue growth and higher-than-expected capital expenditure projections. Why? We can name a few reasons. First, the debut of Claude’s AI agent bot, which can operate independently in browsers, heightened fears that AI will replace traditional software technologies, particularly as rising hyperscaler spend is expected to improve AI performance. Second, investors are increasingly concerned that AI investment may not generate sufficient revenue to justify the spend. However, we have a more positive spin on both stories. First, rather than replacing traditional software, AI agents may lead to greater software use, not less. Second, we are not yet seeing an oversupply of data centers. Hyperscalers continue to report unmet demand for compute (i.e., insufficient data center and semiconductor capacity), which is critical for both training frontier AI models and running existing chatbots. Put differently, if demand for compute to run chatbots still outstrips supply, imagine the compute required to power an army of agents running 24/7—each using at least four times as much compute as chatbots.

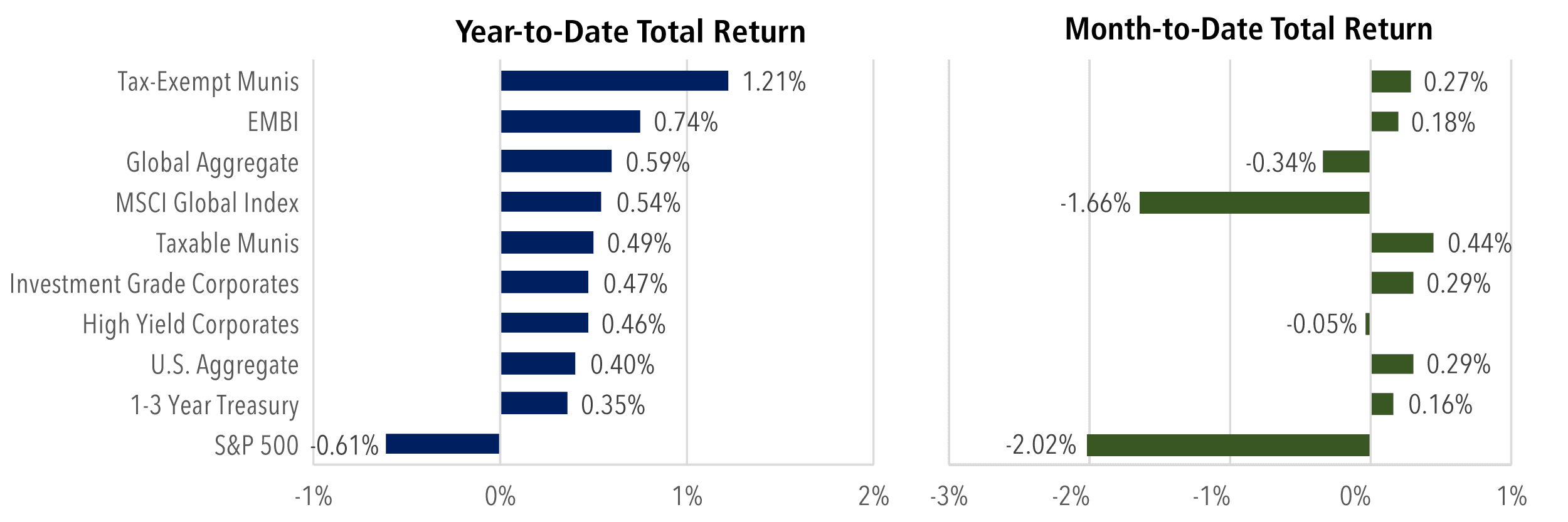

Total Returns by Asset Class

Highlights of the Week:

High Yield: Software issuers exposed to AI disruption have been in the crosshairs of investors. The broadly syndicated loan and private credit markets are more vulnerable to AI disruption because technology issuers make up more than 20% of each market, yet they constitute only 5% of the high-yield bond market. While we haven’t seen signs of contagion, default cycles are often sector-driven, and the next cycle will likely concentrate in the asset classes most exposed to the problem sector.

Corporates: Recent volatility surrounding AI has spilled over into the private credit markets due to concerns about tech-heavy and softwareexposed loan books. While higher-quality short-term bonds have performed better, with spreads wider by a single digit, longer-term softwareexposed names have widened anywhere from 25-50 basis points over the past two weeks.

Municipals: Muni inflows started the year strong, with January weekly inflows reaching $6.3 billion. Meanwhile, performance has remained solid. The Bloomberg Municipal Index posted a 0.9% return, outperforming the U.S. Treasury Index. Additionally, the muni high yield index posted a 1% return, and the taxable muni index also recorded a positive return at 0.05%.

Equities: The U.S. equity market ended the week lower amid increased volatility as investors weighed concerns that the rise of AI could hinder the growth prospects of specialized companies. Sector performance varied: consumer staples, energy, and industrials were the top performers, while consumer discretionary, communications, and technology lagged behind.

Securitized Products: Despite the heavy dose of new issuance at the start of the year (up approximately 70% from January 2025), spreads have narrowed in the residential mortgage-backed security (RMBS) credit market. Investor demand has been supported by strong economic data and the presidential administration's emphasis on boosting the housing market. Investors have shifted into RMBS credit after taking profits in agency mortgages as spreads tightened in response to the administration’s directive for the government-sponsored enterprises (GSEs) to purchase $200 billion of agency mortgage-backed securities (MBS).